Florida doesn’t send warning letters. When a Bureau of Compliance investigator arrives at your job site and finds you operating without workers’ compensation coverage, they issue a stop-work order on the spot halting all operations immediately. You cannot work, bill clients, or fulfill contracts until you prove compliance and pay your penalties.

In 2024, Florida issued 2,323 enforcement actions against non-compliant employers, resulting in $14.7 million in assessed penalties, $6.7 million in generated premium, and 8,457 workers added to active coverage (Florida OIR Workers’ Compensation Annual Report, January 2026). Those are the numbers from one year of enforcement in one state.

The penalties for workers’ comp non-compliance consistently exceed the cost of the coverage itself often by a significant multiple. Here we’ll explain exactly what non-compliance costs, what triggers it, and how Florida employers stay on the right side of the law in 2026.

What Triggers a Workers’ Comp Compliance Investigation?

Florida’s Bureau of Compliance conducts unannounced job site inspections across the state construction sites, commercial properties, landscaping crews, and any business where employees are visible. Investigators have the authority to review your business records, speak with employees, request certificates of insurance, and issue stop-work orders without prior notice.

Enforcement is also triggered by:

- Employee injury reports: When an employee files a workers’ comp claim and the carrier cannot confirm active coverage, investigators respond immediately

- Competitor or public tips: Anonymous reports from competitors or members of the public about businesses operating without coverage frequently initiate investigations

- Routine industry sweeps: Florida targets high-risk industries construction, roofing, landscaping, staffing for proactive enforcement sweeps, particularly in Tampa, Miami, and Orlando

- Payroll audits: Annual premium audits by your carrier identify payroll discrepancies that can expose misclassification errors or unreported employees triggering retroactive premium charges and, in some cases, regulatory referrals

Being found out of compliance does not require malicious intent. Employers who genuinely believed they were covered because an exemption expired, a policy lapsed, or a subcontractor was assumed to carry their own coverage face the same penalties as those who deliberately avoided coverage.

The Real Cost of Non-Compliance: Florida Workers’ Comp Penalties in 2026

The penalties for workers’ comp violations scale rapidly. Here is what each violation type actually costs with real-world cost examples based on current Florida enforcement:

| Violation Type | Penalty | Real-World Cost Example |

|---|---|---|

| No workers’ comp coverage (non-construction, 4+ employees) | Stop-work order + $1,000 minimum or 2× unpaid premiums for up to 2 years — whichever is greater | A landscaping company with $250,000 payroll goes uninsured for 8 months. Estimated penalty: $20,000+ in doubled premiums plus business shutdown until compliant. |

| No coverage (construction, 1+ employees) | Same: stop-work order + $1,000 minimum or 2× unpaid premiums. Construction carries higher risk — penalties escalate faster. | A roofing contractor with 3 workers skips coverage for 6 months. Higher industry rate × 2 = potentially $15,000–$30,000+ in penalties. |

| Misclassifying employees as independent contractors | $5,000 per misclassified worker — plus the standard non-coverage penalty on any resulting premium gap | A contractor labels 5 workers as 1099 contractors: $25,000 in misclassification fines alone, before premium penalties. |

| Violating a stop-work order (continuing to work after order issued) | $1,000 per day for each day of continued violation | An employer ignores the stop-work order and operates for 5 days: $5,000 additional penalty — on top of all prior fines. |

| Filing a false exemption certificate or fraudulent policy document | Felony charge — third-degree or higher depending on dollar value. Potential prison sentence. | A business owner files a false certificate of insurance: criminal fraud charge, potential prison time. |

| Lapsed policy — coverage expires and is not renewed | Immediately non-compliant from the first day of lapse. Subject to the same penalties as never having coverage. | A policy lapses for 30 days during renewal: any injury during that window = employer personal liability + penalty exposure. |

Criminal Exposure

In Florida, filing a false certificate of insurance, submitting a fraudulent exemption certificate, or deliberately misclassifying employees to avoid premium constitutes a felony. In one documented South Florida case, a carpentry contractor who hid payroll to reduce workers’ comp costs faced up to 30 years in prison upon conviction. The financial penalties pale against the criminal exposure.

The Three Most Common Compliance Violations and How to Avoid Them

1. Misclassifying Employees as Independent Contractors

This is Florida’s number-one workers’ comp compliance error. Businesses label full-time or regular workers as 1099 contractors to avoid the cost of workers’ comp coverage. Florida uses a right-to-control test: if you control how the work gets done — setting schedules, providing tools, directing methods — that worker is almost certainly an employee, regardless of what the contract says.

The penalty: $5,000 per misclassified worker, plus the standard doubled-premium penalty for any coverage gap that resulted. Five misclassified workers on a single inspection = $25,000 in misclassification fines before any coverage penalty is calculated.

Review your workers’ comp requirements and confirm your classification structure annually especially before adding contract workers or expanding into new work categories.

2. Allowing Coverage to Lapse

A policy that expires without renewal leaves you non-compliant from day one of the lapse. Many employers assume a grace period exists it doesn’t. Any injury during an uninsured period creates direct personal employer liability for all medical costs, lost wages, disability benefits, and potentially death and survivor benefits — in addition to the penalty for the lapse period itself.

Set calendar reminders 60 and 30 days before your renewal date. Confirm your carrier has processed the renewal and that your Certificate of Insurance is current before your old policy expires.

3. Failing to Verify Subcontractor Coverage

Florida holds the hiring contractor responsible when an uninsured subcontractor is injured on their site. If the subcontractor cannot produce valid workers’ comp coverage, you as the general contractor or hiring employer may be treated as the employer for coverage purposes and held liable for all benefits owed to that injured worker.

Before any subcontractor begins work: request their Certificate of Insurance showing active workers’ comp coverage, verify it through the Florida Division of Workers’ Compensation’s proof of coverage database, and keep copies on file. This is not optional it is a direct line of liability protection.

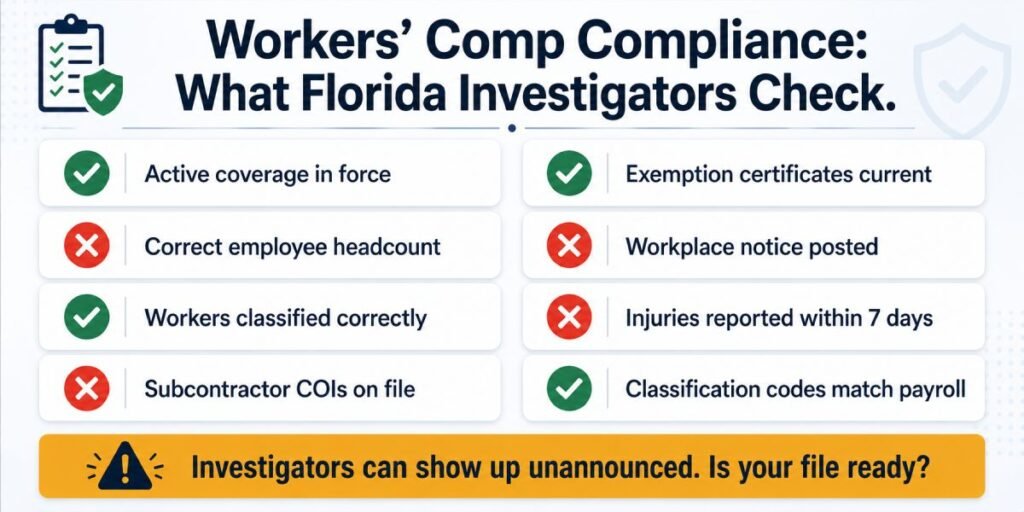

The Workers’ Comp Compliance Checklist Every Florida Employer Needs

Use this checklist to audit your own compliance posture before an investigator does it for you. Each item represents a real enforcement trigger and a real penalty if it’s out of order:

| Compliance Requirement | When to Check | What Can Go Wrong |

|---|---|---|

| Coverage is active and current — no lapse | Before any employee starts work | Confirm active policy with your carrier before your first hire and at every renewal date. Set auto-renewal alerts. |

| All employees counted correctly — FT, PT, seasonal, temporary | At hiring and annually | Part-time and seasonal workers count toward the threshold. An audit that finds uncounted employees triggers immediate non-compliance. |

| Worker classification reviewed — employee vs. contractor | At hiring and when roles change | Use Florida’s right-to-control test. If you direct how work is done — not just the result — that person is likely an employee. |

| Subcontractor coverage verified before work begins | Before any subcontractor starts work on your site | Request a current Certificate of Insurance showing valid workers’ comp. Keep copies on file. You are liable for uninsured subcontractors injured on your site. |

| Corporate officer exemptions filed and current | Every 2 years (exemptions expire) | Exemptions must be renewed — they are not permanent. An expired exemption means you may be uncovered without realizing it. |

| Workplace injury posted and notification procedures in place | Ongoing — post required notice visibly | Florida requires you to post workers’ comp information where employees can see it. Failure to post can be cited during inspections. |

| Injuries reported to carrier within 7 days | After every injury | Late reporting triggers fines and can delay the injured worker’s benefits — creating additional legal exposure for the employer. |

| Payroll and classification codes reviewed at renewal | Annually at policy renewal | Payroll changes and role changes affect your classification codes and premium. Inaccurate codes can result in audit surcharges or fraud allegations. |

The Cost of Coverage vs. the Cost of Non-Compliance

The math on workers’ comp compliance is unambiguous. Consider a Florida landscaping company with $300,000 in annual payroll.

- Annual workers’ comp premium (approx.): $12,000–$18,000 depending on classification code and experience modifier

- Non-compliance penalty (doubled premium, 12-month period): $24,000–$36,000 minimum — before any personal liability for injuries, which is uncapped

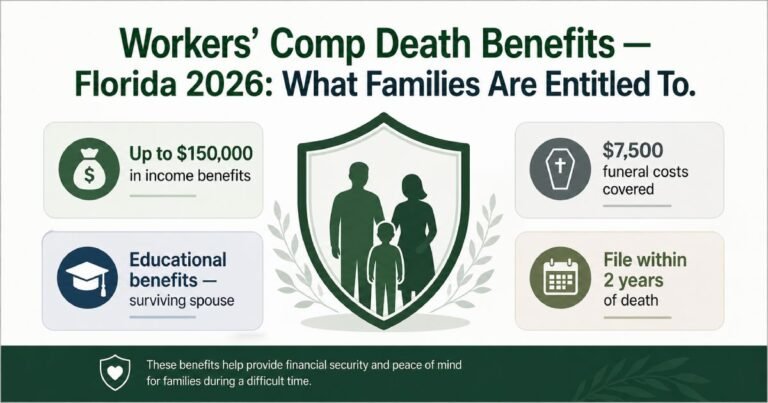

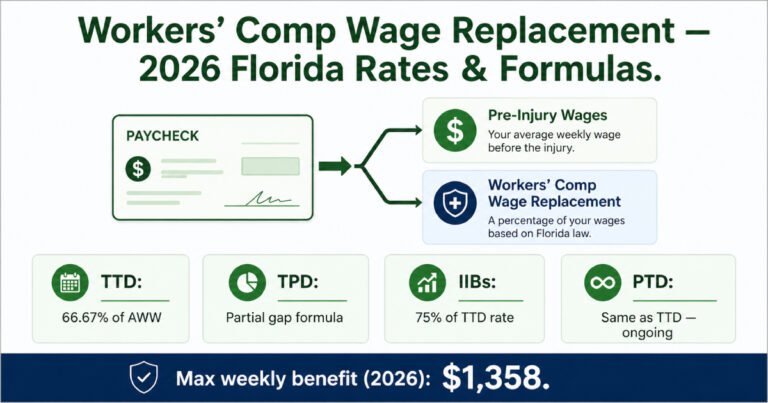

- If one worker is injured while uninsured: Employer pays all medical costs (no cap), lost wages at 66.67% of AWW for the duration of recovery, potential disability or death benefits — all out of pocket, plus litigation exposure

The coverage cost is fixed, predictable, and tax-deductible. The non-compliance exposure is open-ended, personally devastating, and growing every day the gap exists. There is no scenario in which skipping workers’ comp is a sound financial decision — only a costly short-term illusion.

How to Reduce Premium While Staying Compliant

Accurate classification codes, a strong experience modifier from a clean claims history, a documented return-to-work program, and working with an independent advisor who accesses multiple carriers all reduce your premium without creating compliance gaps. The goal is the lowest compliant cost not the lowest-cost non-compliance.

Alternative Compliance Paths: Self-Insurance and the Assigned Risk Pool

Standard workers’ comp coverage through a private carrier is the most common compliance path but it is not the only one. Florida employers who cannot secure coverage in the standard market (typically due to poor claims history) have two additional options:

- Self-insurance: Large employers with sufficient financial reserves can apply to self-insure their workers’ comp obligations. Self-insurance requires approval from the Florida Division of Workers’ Compensation, demonstration of financial solvency, and ongoing reporting obligations. Most small and mid-size businesses do not qualify

- Assigned risk pool (FWCJUA): The Florida Workers’ Compensation Joint Underwriting Association (FWCJUA) provides coverage to employers who cannot obtain it in the voluntary market. Rates are higher than the standard market, but the coverage satisfies all legal requirements and eliminates non-compliance exposure while the employer works to improve their claims profile

Both alternatives carry the same coverage obligations as standard policies. An employer who uses either path and allows their coverage to lapse faces identical penalties to one who had no coverage at all.

FAQs About Workers’ Comp State Compliance

The penalty is the greater of $1,000 or double the amount you would have paid in workers’ comp premiums for up to 24 months of non-compliance. A business with $400,000 in payroll that goes uninsured for 12 months could face $20,000–$40,000+ in penalties — plus an immediate stop-work order, personal liability for any injuries during the uninsured period, and potential felony charges if fraud is involved. The $1,000 minimum applies even if doubled premiums calculate to less

A stop-work order is a Florida state enforcement action that immediately halts all business operations at the site where the violation is found. You cannot work, serve customers, or generate revenue under a stop-work order. To have it lifted, you must: (1) obtain the required workers’ comp coverage with an active, valid policy; (2) pay all assessed penalties in full; and (3) demonstrate compliance to the Division of Workers’ Compensation. Violating a stop-work order by continuing to operate adds $1,000 per day in additional penalties.

Florida assesses a $5,000 fine per misclassified worker in addition to any penalty for the workers’ comp coverage gap that resulted from the misclassification. Five misclassified workers = $25,000 in misclassification penalties before coverage penalties are calculated. Deliberate misclassification to reduce workers’ comp premium is also treated as fraud and can result in criminal felony charges. Florida uses a right-to-control test: if you direct how the work is done, the worker is likely an employee regardless of their contract title.

You do not need to cover subcontractors directly — but you must verify that they carry their own valid workers’ comp coverage before they begin work. If a subcontractor without coverage is injured on your site, Florida may hold you — as the hiring contractor — liable for all workers’ comp benefits owed to that worker, plus penalties. Always request a Certificate of Insurance showing active workers’ comp coverage, verify it through Florida’s proof of coverage database, and keep the documentation on file for every subcontractor who works on your projects.

Four strategies reduce premium without creating compliance gaps:

(1) Accurate classification codes — ensure every employee is classified correctly; over-classification in high-risk codes raises your premium unnecessarily.

(2) Experience modification management — a documented return-to-work program and prompt injury reporting both improve your claims history and lower your experience modifier over time.

(3) Annual payroll audits — confirm payroll figures match your policy before renewal to avoid audit surcharges.

(4) Work with an independent broker — access to multiple carriers ensures you get the most competitive rate for your risk profile.

Get Compliant Today — Before the Inspector Does It for You

Florida workers’ comp enforcement is active, unannounced, and expensive. Every day a business operates without required coverage is a day of penalty exposure and one injured worker away from a financial liability that could permanently damage the business. At Casey insurance Companies our commercial insurance advisors help Florida and nationwide businesses audit their workers’ comp compliance posture, correct classification gaps before audits surface them, and structure workers’ comp coverage that keeps them protected and compliant at every stage. Explore our state compliance and legal security page, review the full workers’ comp insurance program, and contact us for a compliance review today before a stop-work order does it for you.