When a worker dies from a job-related injury or occupational illness, their family faces more than grief. In most cases, they also face the sudden loss of income their household depended on. Florida’s workers’ compensation system the same system that provides medical coverage and lost wage protection to injured workers extends a specific set of benefits to surviving family members when a work-related death occurs.

These benefits are structured, rule-bound, and tied to strict deadlines. They do not flow automatically. Families must file claims, prove eligibility, and meet documentation requirements and they must do so within a window that begins from the date of death. Understanding what these benefits are, who qualifies, and how to access them is essential for any family navigating this process.

Florida Workers’ Comp Death Benefits — Key Numbers

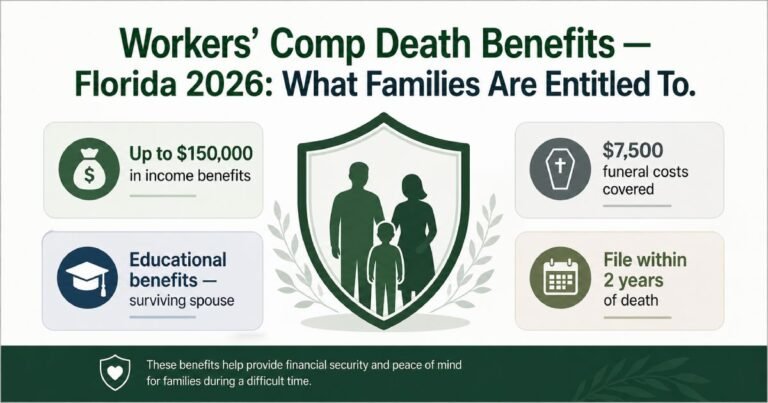

Maximum total indemnity to all dependents: $150,000. Funeral/burial expenses: up to $7,500 — paid within 14 days. Benefit rate: up to 66.67% of the deceased worker’s Average Weekly Wage (AWW). Death must occur within 1 year of the accident (or 5 years if continuous disability). Claim filing deadline: 2 years from the date of death.

When Are Workers’ Comp Death Benefits Triggered?

Florida workers’ comp death benefits apply under Florida Statutes §440.16 when an employee’s death is directly caused by a work-related accident or occupational illness. The system operates on a no-fault basis the family does not need to prove the employer was negligent. The only requirement is that the death arose out of and in the course of employment.

Two timing rules govern eligibility:

- One-year rule: The death must occur within one year of the workplace accident for benefits to apply.

- Five-year exception: If the work-related accident caused continuous disability that the worker never recovered from, and the death occurs within five years of the accident date, survivor benefits still apply even if more than a year has passed since the injury.

Carriers frequently dispute whether a death is work-related particularly when the death occurs weeks or months after an injury, or when a pre-existing condition is involved. Clear documentation connecting the injury to the cause of death is essential. This is especially relevant for occupational illnesses such as mesothelioma, industrial disease, or cumulative physical damage where the connection between work exposure and death may be contested.

The state compliance and legal security requirements that govern Florida workers’ comp including the obligation to carry adequate coverage — are what ensure these benefits are funded when a fatal claim occurs.

The 2-Year Filing Deadline

Families must file a claim for death benefits within 2 years of the date of the employee’s death (Florida Statute §440.19). Missing this deadline can permanently bar the claim. The deadline does not pause while the insurance carrier is ‘reviewing’ the case. If benefits are delayed or disputed, families should seek legal guidance and file formally without waiting for informal resolution.

Who Is Eligible for Workers’ Comp Death Benefits in Florida?

Benefits go to dependents of the deceased worker not simply to next of kin. Florida law establishes a specific hierarchy of eligible dependents, with priority given to those with the closest family relationship and the strongest financial dependency.

Priority Order of Eligible Dependents

- Surviving spouse: Must have been legally married to the deceased at the time of both the accident and the death. A common-law spouse may qualify if the common-law marriage was established in a state that recognizes it.

- Dependent children: Children qualify automatically to age 18. Children who are full-time students qualify to age 22. Children with a mental or physical disability that prevents self-support qualify at any age indefinitely.

- Fully dependent parents: Eligible only if there is no qualifying spouse or child, and only if the parent was fully financially dependent on the deceased worker.

- Fully dependent siblings or grandchildren: Eligible only if no higher-priority dependents qualify, and only with proof of full financial dependency.

Partial dependents family members who received some support from the deceased but were not fully dependent may qualify for a proportional benefit in certain circumstances, but this is less common and more frequently contested by carriers.

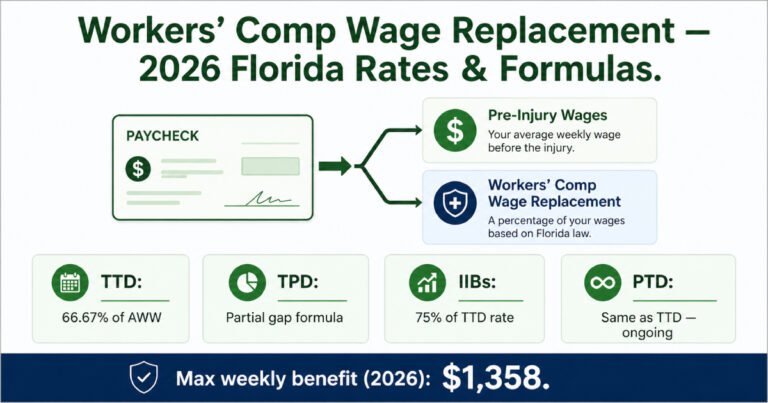

How Much Do Survivor Benefits Pay?

All income benefits are calculated as a percentage of the deceased worker’s Average Weekly Wage (AWW) — the same AWW used to calculate lost wage protection benefits during the worker’s lifetime. AWW is based on the 13 weeks of earnings prior to the accident.

| Eligible Dependent Category | Weekly Benefit Rate | Duration and Key Conditions |

|---|---|---|

| Surviving spouse (no children) | 50% of AWW | Paid for the remainder of the spouse’s life, or until remarriage. At remarriage: lump sum of 26 weeks × 50% AWW (capped at $150,000 total). Entire benefit from date of death. |

| Surviving spouse + dependent children | 66.67% of AWW total | Spouse receives 50%, children collectively receive 16.67% divided equally. A judge may reallocate the full amount to children if deemed in their best interest. |

| Dependent children only (no surviving spouse) | 33.33% of AWW divided equally | All eligible dependent children share 33.33% of AWW equally. Children qualify to age 18; to age 22 if full-time students; any age if permanently disabled. |

| Fully dependent parents (no spouse or children) | 25% of AWW per parent | Must prove full financial dependency on the deceased worker. Each qualifying parent receives 25%. |

| Fully dependent siblings, grandchildren | 15% of AWW each | Only eligible if no spouse, children, or parents qualify. Must prove full financial dependency on the deceased worker. |

| Total benefit cap (all dependents combined) | Maximum: $150,000 | Total indemnity payments to all dependents cannot exceed $150,000 across the entire benefit period. Funeral costs ($7,500) are separate and not counted toward this cap. |

Complete Benefits Package: Everything the Employer’s Policy Must Cover

Florida workers’ comp death benefits extend beyond weekly income payments. The workers’ compensation insurance policy the employer carries is the funding mechanism for all of the following components:

| Benefit Component | Amount | Key Conditions / Notes |

|---|---|---|

| Funeral / burial expenses | Up to $7,500 — paid by employer directly | Employer must pay within 14 days of receiving the funeral bill. Separate from indemnity cap. Covers actual funeral costs only. |

| Compensation to dependents | Up to 66.67% of deceased’s AWW | Paid weekly to eligible dependents (see eligibility table). All payments combined cannot exceed $150,000 total indemnity. |

| Medical expenses prior to death | All authorized medical costs incurred from injury to date of death | Covered fully — same as standard workers’ comp medical benefits during the illness or injury period. |

| Educational benefits (surviving spouse) | Up to 1,800 classroom hours — or equivalent in student fees | Helps a surviving spouse re-enter the workforce. Available for up to 7 years from the date of the employee’s death. |

| Remarriage lump sum | 26 weeks × 50% AWW — subject to $150,000 overall cap | Paid to surviving spouse upon remarriage in lieu of continued weekly benefits. This ends the spouse’s ongoing benefit entitlement. |

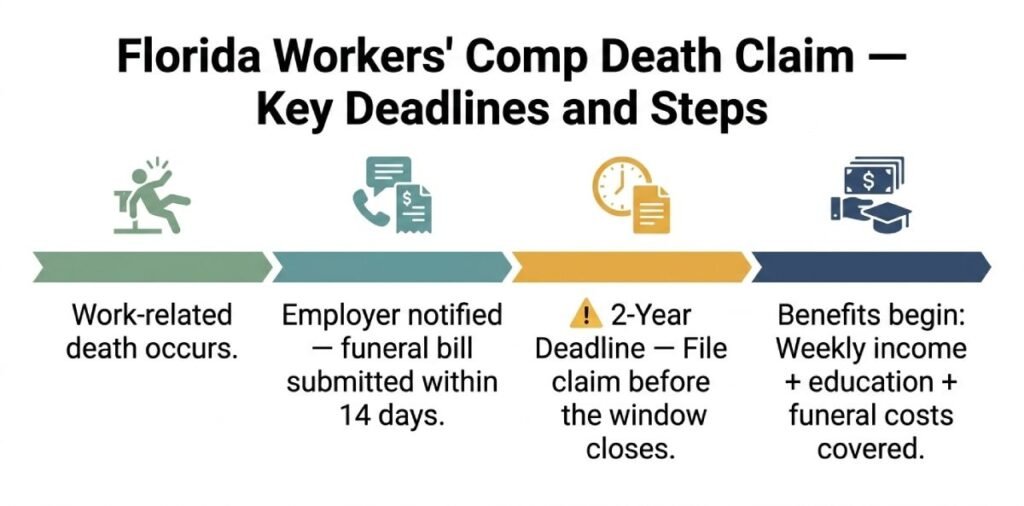

How to File a Workers’ Comp Death Claim in Florida

Filing for death benefits requires organized documentation and timely action. The following steps reflect the standard claims process under Florida’s workers’ compensation system:

- Notify the employer: Inform the deceased employee’s employer of the work-related death as soon as possible. The employer is required to notify their workers’ comp carrier within 7 days

- Submit funeral expenses immediately: The employer must pay funeral costs up to $7,500 within 14 days of receiving the bill. Submit the invoice promptly do not wait for the broader claim to be processed

- Gather documentation: Death certificate, accident or injury report, hospital and medical records from the injury period, proof of relationship to the deceased, financial dependency records (bank statements, tax returns), wage records for AWW calculation, and school enrollment records if claiming for student children

- File the claim formally: Submit a Petition for Benefits with the Florida Division of Workers’ Compensation. This formally initiates the claim and triggers the carrier’s obligation to respond

- Respond to carrier requests promptly: The carrier may request an Independent Medical Examination to dispute causation, or additional documentation to verify dependency. Delays in responding can slow or jeopardize the claim

- If denied or delayed: Claims that are denied or left unresolved can be escalated through the Division of Workers’ Compensation’s dispute resolution process. The 2-year deadline continues to run regardless of carrier activity do not wait for informal resolution

This process runs through the workers’ compensation administrative system not the civil court system and is governed by the same state compliance framework that governs all Florida workers’ comp claims.

What This Means for Employers: Liability and Coverage

For employers, a fatal workplace injury triggers the highest-value workers’ comp claim their policy may ever face. With total indemnity exposure up to $150,000 plus funeral costs, medical expenses, and educational benefits a single fatality can represent a significant financial obligation.

This is precisely why Florida law requires employers to carry adequate workers’ compensation insurance. Without coverage, the employer becomes directly and personally liable for every element of the death benefit package an obligation that could extend for years or decades in the form of ongoing weekly payments to a surviving spouse and dependent children.

Beyond the financial protection, workers’ comp coverage also provides employer liability protection through the employer liability component (Part B) of the policy — which responds in the rare cases where family members pursue additional legal action beyond the workers’ comp system, such as third-party liability claims against a manufacturer of defective equipment.

Employers concerned about fatal injury risk in their operations should review their workers’ comp requirements and work with their advisor to ensure policy limits, classification codes, and coverage terms are appropriate for the nature and scale of their workforce. The combination of medical coverage, wage replacement, and death benefits under a single workers’ comp policy represents the full financial ecosystem of workplace injury protection.

Frequently Asked Questions: Workers’ Comp Death Benefits

Benefits go to dependents — not all family members. Priority order: (1) surviving spouse; (2) dependent children (under 18, or to 22 if full-time students, or any age if permanently disabled); (3) fully dependent parents — only if no spouse or children qualify; (4) fully dependent siblings or grandchildren — only if no higher-priority dependents exist.

Benefits are paid as a percentage of the deceased worker’s Average Weekly Wage (AWW): surviving spouse only = 50% of AWW; spouse and children = 66.67% AWW total (50% spouse + 16.67% children); children only = 33.33% AWW divided equally. Total indemnity benefits for all dependents combined are capped at $150,000. Separately, up to $7,500 in funeral expenses must be paid within 14 days — this does not count toward the $150,000 cap.

A surviving spouse receives benefits for the remainder of their life — or until remarriage. At remarriage, a lump sum of 26 weeks × 50% AWW is paid (subject to the $150,000 cap) and weekly payments end. Dependent children receive benefits until age 18 (or 22 if a full-time student, or indefinitely if permanently disabled). Once the $150,000 total indemnity cap is reached, all ongoing payments stop regardless of the recipient’s circumstances.

Yes — Florida workers’ comp requires the employer’s carrier to pay up to $7,500 in actual funeral and burial expenses. The employer must pay the funeral bill within 14 days of receiving it. This payment is separate from the weekly income benefits paid to dependents and does not count against the $150,000 total indemnity cap.

Ensure Your Workers’ Comp Policy Fully Covers the People Who Depend on It

The benefits described in this guide are only as reliable as the workers’ compensation coverage behind them. An employer without adequate coverage or with gaps in classification or compliance may leave surviving families pursuing benefits from an uninsured employer directly, a legally complex and often unsuccessful process. Our commercial insurance advisors help Florida and nationwide businesses structure workers’ compensation coverage that fully addresses every component of the benefit structure from medical treatment and lost wage protection through death and survivor benefits and state compliance obligations. Review our complete workers’ comp insurance program and contact us for a coverage review today.