Workers’ compensation is not optional. In nearly every state and for most Florida employers it is a legal requirement the moment you bring on employees. It protects your workers when something goes wrong on the job, and it protects your business from direct lawsuit exposure that could otherwise be financially catastrophic.

Despite this, workers’ comp is one of the most misunderstood commercial insurance coverages. Many employers don’t know exactly when it applies, what it pays for, or what happens if they’re not compliant. And in Florida, non-compliance carries serious consequences: stop-work orders, penalties of $1,000 or more, doubled premium assessments, and personal liability for injured workers’ medical costs and wages.

2026 Florida Workers’ Comp at a Glance

Florida issued 2,323 enforcement actions in 2024 and assessed $14.7 million in penalties (FL OIR 2025 Annual Report). Rates are expected to decrease an average of 6.9% in 2026 (NCCI proposal). Florida’s workers’ comp market wrote $3.18 billion in private sector premium in 2024.

What Workers’ Compensation Insurance Covers

Workers’ compensation is a no-fault insurance system. When an employee is injured at work or develops a work-related illness regardless of who caused the incident workers’ comp pays for their recovery and a portion of their lost income. In exchange, employees give up the right to sue their employer for work-related injuries in most circumstances.

The four main benefit categories workers’ comp provides to injured employees:

- Medical coverage: All reasonable and necessary medical treatment for the work-related injury or illness doctor visits, hospitalization, surgery, physical therapy, prescription medications

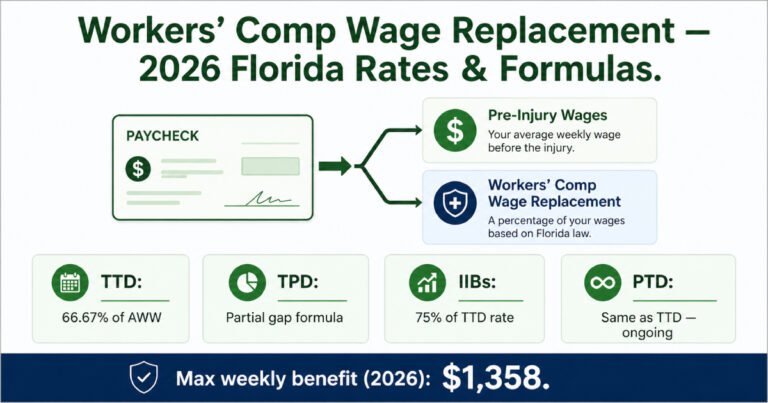

- Lost wage protection: Typically 66.67% of the employee’s average weekly wage during the period they cannot work — subject to state-mandated minimum and maximum benefit amounts

- Disability benefits: Coverage for both temporary and permanent disability the scale of benefit depends on the severity and permanence of the impairment

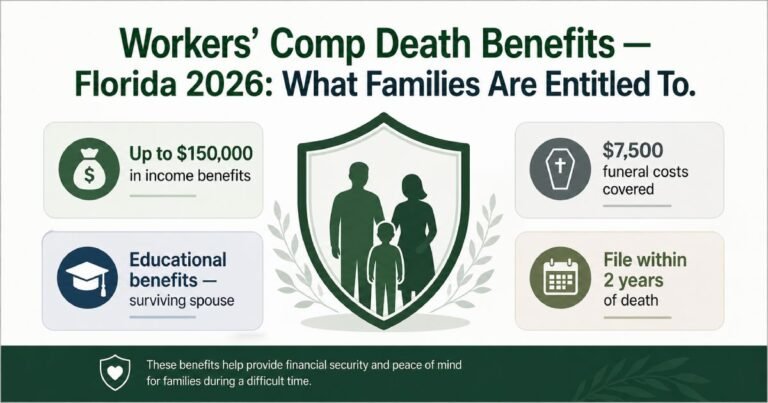

- Death and survivor benefits: Paid to eligible family members if an employee dies from a work-related injury — Florida allows up to $150,000 in compensation benefits paid at 66.67% of the deceased’s weekly wage

Workers’ comp also protects employers through the employers’ liability component (Part B of a standard workers’ comp policy), which covers employer legal costs in the event an employee sues despite the workers’ comp system such as in cases of alleged gross negligence or intentional harm.

What Workers’ Comp Does NOT Cover

Injuries sustained commuting to work (outside employer premises), intentional self-inflicted injuries, injuries occurring while intoxicated, and injuries unrelated to the employee’s job duties. Misclassifying employees as independent contractors to avoid coverage is also a common compliance error that can result in significant penalties.

Florida Workers’ Comp Requirements: Who Needs Coverage and When

Florida’s workers’ compensation requirements are governed by Chapter 440, Florida Statutes, and enforced by the Florida Division of Workers’ Compensation. The rules vary significantly by industry particularly for construction, which has much stricter thresholds than other sectors:

| Business Type | When Coverage Is Required | Non-Compliance Consequences |

|---|---|---|

| Construction businesses | 1 or more employees (including business owners — very limited exemptions) | Immediate stop-work order + minimum $1,000 penalty or 2× unpaid premiums for up to 2 years — whichever is greater |

| Non-construction businesses | 4 or more employees (full-time or part-time combined) | Same: stop-work order + minimum $1,000 or 2× premium penalty; repeated violations = criminal charges |

| Agricultural employers | 6+ regular workers OR 12+ seasonal workers for 30+ days | Same enforcement mechanism — stop-work orders, fines, personal employer liability |

| Corporate officers / LLC members | May elect exemption under Fla. Stat. §440.05 — valid 2 years, must be renewed | Exemption must be filed — not automatic. Construction officers have very limited exemption rights |

| Independent contractors (construction) | Must carry own coverage or be covered by hiring contractor | Employer held liable if uninsured contractor injured on your site without verified coverage |

Your Responsibilities as an Employer

Having workers’ comp coverage is step one. But employers also carry specific ongoing compliance obligations once coverage is in place:

- Maintain continuous, uninterrupted coverage: Even a single day without coverage can trigger a stop-work order and penalties. Set auto-renewal and confirm your policy reflects your current payroll and employee headcount

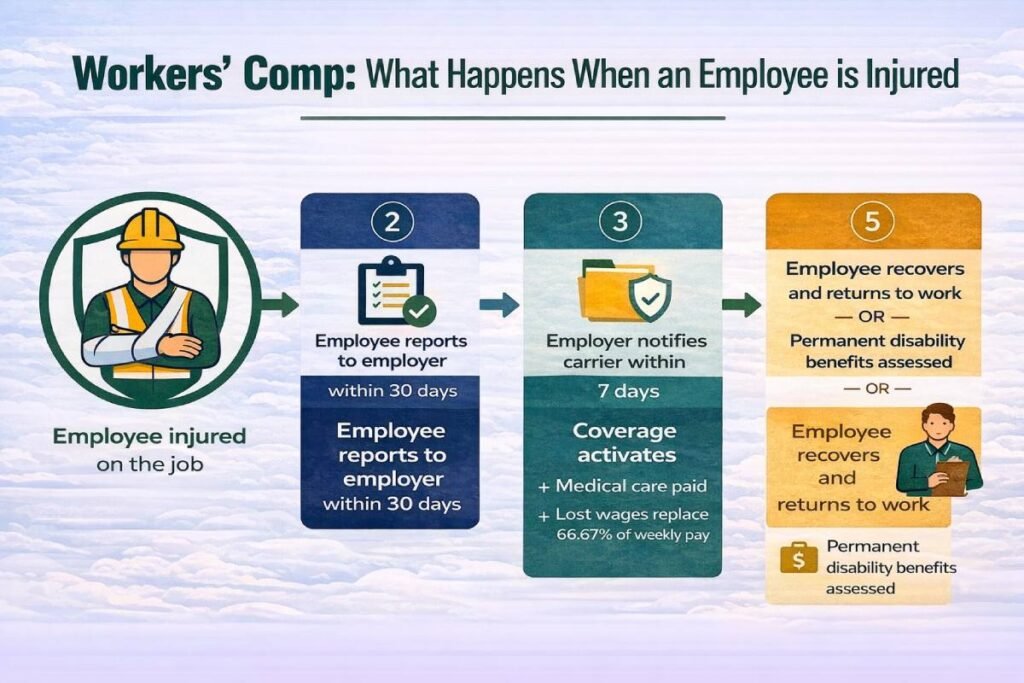

- Report workplace injuries promptly: Florida law requires you to notify your insurer of a work-related injury typically within 7 days of learning about it. Late reporting can complicate or delay claims and increase your exposure

- Post required notices: Florida employers must display workers’ comp information in a location visible to all employees, informing them of their coverage rights and how to report injuries

- Verify independent contractor coverage: If a contractor working on your site doesn’t have workers’ comp, you can be held liable for their injuries. Always request proof of coverage before work begins and keep documentation on file

- Keep records of exemptions: If you or any corporate officer is exempt, maintain your exemption certificates. Exemptions expire every two years — lapsed exemptions mean you’re uninsured and non-compliant without realizing it

- Accurately classify employees: Workers’ comp premiums are calculated by job classification code. Misclassifying workers in lower-risk codes to reduce premium is a form of fraud that generates audit penalties and retroactive premium charges

Florida: State Compliance Coverage

Florida also mandates employers maintain compliance with state regulations and legal security obligations under workers’ comp. See our page on

What Does Workers’ Comp Insurance Cost in Florida in 2026?

Good news for Florida employers: workers’ comp rates are declining in 2026. The National Council on Compensation Insurance (NCCI) has proposed an average 6.9% rate decrease continuing a multi-year trend driven by declining lost-time claim frequency and improving claims outcomes.

Your premium is calculated using three primary inputs:

- Payroll: Premium is assessed per $100 of payroll. Higher payroll = higher premium

- Job classification code: Each type of work carries a specific risk rating — roofing and construction trades pay significantly more per $100 of payroll than office or clerical workers

- Experience modification factor (ex-mod): Your claims history relative to industry average. A clean record earns a credit mod (below 1.0) and a lower premium; frequent claims result in a debit mod (above 1.0) and higher premium

For 2026, Florida’s minimum payroll for included owners/officers is $33,800 for construction and $67,600 for all other industries (up from $65,000 in 2025). These minimums apply when calculating coverage for business owners who choose to include themselves in coverage. The median workers’ comp premium for small businesses is approximately $45–$70/month for lower-risk operations — though this varies widely by industry and payroll size.

Workers’ Comp vs. Employer Liability Insurance — What’s the Difference?

A standard workers’ comp policy includes two distinct coverages:

- Part A — Workers’ Compensation: The statutory coverage described above. Pays benefits to injured employees as required by Florida law. No dollar limit — your carrier pays whatever the statutory benefit requires.

- Part B — Employers’ Liability: Covers your business against lawsuits from employees or their families who claim your negligence caused the injury — in situations outside the standard workers’ comp system (e.g., dual-capacity lawsuits, spouse claims, or intentional tort allegations). Typically limited to $100,000/$500,000/$100,000 at standard policy limits.

Most employers think of these as one thing and in practice they’re purchased together. But understanding the distinction matters: workers’ comp protects employees, employer liability protects you from the edge cases where the system’s normal protections don’t apply.

For more detail on how these protections compare, see our article on employers’ liability vs. workers’ compensation.

Frequently Asked Questions: Workers’ Comp Requirements

It depends on your industry. For construction businesses: coverage is required with 1 or more employees — including business owners in most cases. For non-construction businesses: coverage is required with 4 or more employees (full-time and part-time combined). For agriculture: 6+ regular workers or 12+ seasonal workers working 30+ days in a season. Part-time, seasonal, and temporary workers all count toward the threshold. Texas is the only state that does not mandate workers’ comp for private employers.

Generally no — independent contractors are not employees and are not automatically covered under your workers’ comp policy. However, if you hire an uninsured contractor who is injured while working for you, you may be held liable for their benefits as if they were an employee. Always request a current Certificate of Insurance showing valid workers’ comp coverage before a contractor begins work, and keep that documentation on file.

Get Compliant, Stay Compliant — and Protect Both Your Business and Your Team

Workers’ comp is not just a legal checkbox it is the protection that keeps a workplace injury from becoming a business-ending financial event. In 2026, with Florida rates declining and enforcement remaining active, there has never been a better time to review your coverage, verify your compliance status, and ensure your policy reflects your current payroll and workforce.

Our commercial insurance advisors help Florida businesses structure workers’ compensation coverage that is correctly classified, competitively priced, and fully compliant with Florida law. Explore our medical injury coverage, lost wage protection, death and survivor benefits, and state compliance and legal security and contact us today for a workers’ comp coverage review.