When a workplace injury happens, one of the first things employees want to know is: who pays for my medical care?

The answer under workers’ compensation is clear: the employer’s insurance carrier pays 100% of all medically necessary, authorized treatment related to the work injury with no co-pays, no deductibles, and no out-of-pocket cost to the injured employee. This is not a benefit that varies by employer generosity. In Florida, it is the law.

Let’s explore exactly what medical treatment workers’ comp covers, how the authorization system works, what employees are entitled to from the moment of injury through recovery, and what happens when insurers push back on treatment.

Florida 2026 Medical Context

Florida raised physician reimbursement rates from 110% to 175% of Medicare (SB 362, effective 2024) — improving access to care but adding pressure on carriers to scrutinize claims more closely. Employee medical rights remain unchanged. Florida workers’ comp rates decreased 6.9% for 2026 the 9th consecutive year of reductions.

The Fundamental Rule: Zero Out-of-Pocket Medical Costs for Injured Workers

Florida’s workers’ compensation system (Chapter 440, Florida Statutes) requires the employer’s insurance carrier to pay for all medically necessary treatment for a work-related injury or occupational illness. The injured employee does not pay:

- Emergency room or urgent care co-pays

- Doctor visit co-pays

- Deductibles of any kind

- Pharmacy co-pays for prescribed medications

- Physical therapy session fees

- Surgery costs, hospital room charges, or anesthesia

This zero-cost structure is one of the primary reasons the workers’ compensation system exists: an employee who is injured on the job should not face a choice between getting medical care and paying their bills. Workers’ comp eliminates that choice entirely provided the injury is work-related and the claim is properly filed and accepted.

The ‘Authorized Physician’ Requirement

In Florida, workers’ comp medical benefits apply to treatment from an authorized physician typically selected from the insurance carrier’s network or authorized by the carrier. If you seek treatment from a physician who is not authorized, the carrier can refuse to pay those bills. After the initial emergency period, confirm your treating doctor is authorized before continuing care.

What Workers’ Comp Medical Coverage Includes — Full Reference

Here is the complete list of medical services covered under Florida workers’ comp, from the first day of injury through full recovery or permanent impairment determination:

| Medical Service | Coverage Under Florida Workers’ Comp | Cost to Employee |

|---|---|---|

| Emergency care | 100% — no co-pay, no deductible. ER visits, ambulance, stabilization care all covered immediately after a work injury. Employee pays nothing. | $0 (zero out-of-pocket) |

| Doctor visits (authorized physician) | 100% — all treatment from your employer/carrier-authorized physician is covered, including follow-ups and specialist referrals within the system. | $0 (zero out-of-pocket) |

| Diagnostic imaging | 100% — X-rays, MRIs, CT scans, ultrasounds ordered by the authorized treating physician. | $0 (zero out-of-pocket) |

| Surgery | 100% — all medically necessary surgical procedures including anesthesia, operating room costs, and post-surgical care. | $0 (zero out-of-pocket) |

| Physical & occupational therapy | 100% — all medically authorized physical therapy, occupational therapy, and rehabilitation services. | $0 (zero out-of-pocket) |

| Prescription medications | 100% — all medications prescribed by the authorized physician for the workplace injury. No pharmacy co-pay. | $0 (zero out-of-pocket) |

| Durable medical equipment | 100% — crutches, braces, wheelchairs, orthotics, and other DME prescribed for recovery. | $0 (zero out-of-pocket) |

| Mileage reimbursement | Reimbursed — travel to and from authorized medical appointments is reimbursed at the state mileage rate. | $0 (zero out-of-pocket) |

| Psychiatric / mental health (where injury-related) | Covered when directly caused by or resulting from the physical workplace injury — must be authorized by the carrier. | $0 (zero out-of-pocket) |

| Independent Medical Examination (IME) | If the carrier requests an IME, they pay for it. The employee has no cost obligation for carrier-ordered exams. | $0 (zero out-of-pocket) |

How the Authorized Physician System Works

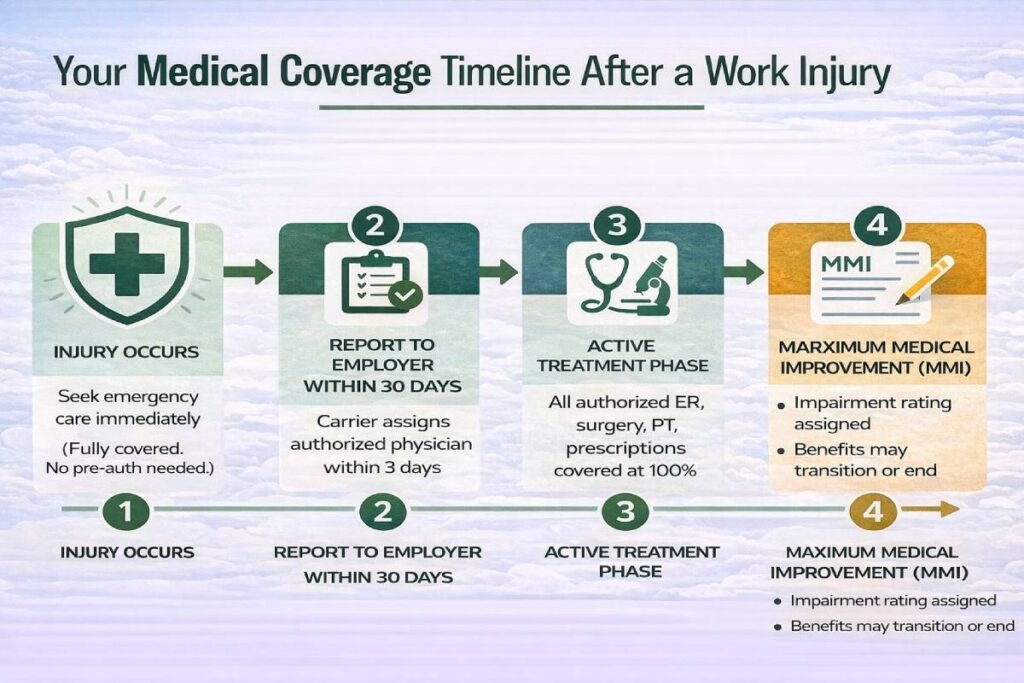

After a work injury, the carrier typically designates an authorized treating physician usually within 3 days of receiving the claim. This physician manages all aspects of care: ordering diagnostics, making referrals, managing treatment, and ultimately determining when the employee has reached maximum medical improvement (MMI).

Here’s how the process unfolds:

- Emergency care: Immediately after an injury, seek emergency treatment at any facility. Emergency care is always covered — no prior authorization needed. The carrier takes over authorization for ongoing care after stabilization.

- Authorized physician assignment: The carrier selects an authorized treating physician. The employee has a one-time right to change physicians within the authorized network if they are dissatisfied with their initial doctor — this must be requested formally.

- Specialist referrals: If the authorized physician determines a specialist is needed (orthopedic surgeon, neurologist, etc.), they initiate a referral. The carrier must authorize specialist treatment, and may request an Independent Medical Examination (IME) to review the need.

- Treatment authorization: Major treatments — surgery, extended physical therapy, expensive procedures — typically require pre-authorization from the carrier. The carrier has 10 days to respond to authorization requests; failure to respond within the statutory timeframe is treated as authorization.

- Maximum Medical Improvement (MMI): When the authorized physician determines the employee has recovered as much as medically expected, they assign MMI status. At MMI, active medical treatment typically ends — though chronic condition management may continue if the injury produced permanent impairment.

Maximum Medical Improvement and What Happens After

MMI does not necessarily mean the employee is fully recovered. It means the medical condition has stabilized to the point where further treatment is unlikely to improve it. At MMI:

- The authorized physician assigns an impairment rating (a percentage) reflecting any permanent loss of function

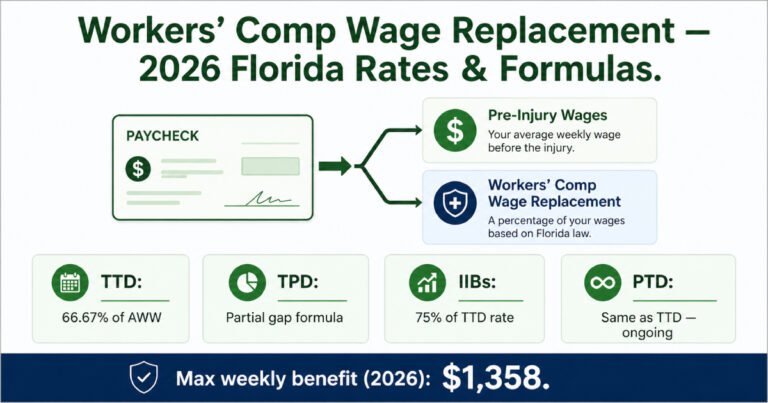

- Employees with a rating above 0% may qualify for Impairment Income Benefits (IIBs) — paid at 75% of the Temporary Total Disability (TTD) rate for a set number of weeks tied to the impairment percentage

- For significant permanent impairments, disability benefits may continue in the form of Permanent Total Disability (PTD) if the employee cannot return to any form of work

- Medical treatment for the specific workplace injury can continue post-MMI if medically necessary — but requires carrier authorization for each episode of care

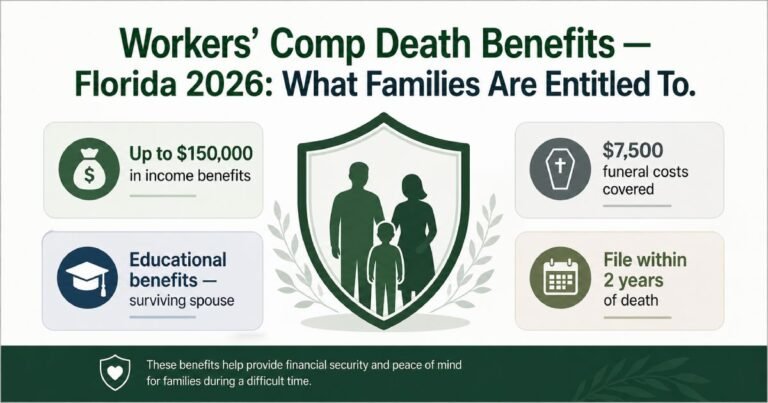

For details on the wage replacement benefits that run alongside medical coverage, see our guides on lost wage protection under workers’ comp and death and survivor benefits.

Medical Coverage Limits and Exclusions

Workers’ comp medical coverage is broad but not unlimited. Key boundaries:

- Unauthorized treatment: Treatment from physicians not authorized by the carrier is not covered. Always confirm authorization status before ongoing care — especially specialist visits

- Pre-existing conditions: Workers’ comp covers the aggravation of a pre-existing condition if the workplace injury worsened it, but not the pre-existing condition itself

- Injuries from intoxication or willful misconduct: Claims are denied if the injury resulted from the employee’s intoxication, intentional self-harm, or deliberate violation of safety rules

- Non-work-related conditions: Only the specific injury or illness arising from employment is covered — not general healthcare or conditions unrelated to the work incident

- Injuries during commute: Standard workers’ comp does not cover injuries that occur during the normal commute to or from work — only injuries during work duties or on employer-controlled premises

Employer Responsibilities for Medical Coverage

From the employer side, workers’ compensation insurance is the mechanism that funds all of these medical benefits. Without valid coverage, the employer is directly and personally liable for every dollar of a work-injured employee’s medical costs, wage replacement, and disability benefits an exposure that can easily reach six or seven figures in a serious injury case.

Beyond purchasing coverage, Florida employers must:

- Report injuries promptly: Notify the carrier within 7 days of learning of a work-related injury. Late reporting can complicate authorization timelines and delay employee care

- Direct employees to authorized providers: After initial emergency care, guide injured employees to the carrier’s authorized physician network to ensure all treatment is covered

- Not interfere with the claims process: Florida law prohibits employers from retaliating against employees who file workers’ comp claims or from discouraging legitimate claims

- Maintain correct classification codes: Accurate payroll and job classification ensures the policy covers all workers in the right risk categories — misclassification can create coverage gaps

For the more details about employer obligations, see our blog on workers’ comp legal requirements and employer responsibilities.

Frequently Asked Questions: Workers’ Comp Medical Coverage

Yes — for authorized medical treatment related to the workplace injury, Florida workers’ comp covers 100% of medical costs with no co-pays, no deductibles, and no out-of-pocket expense to the employee. This includes emergency care, surgery, physical therapy, diagnostics, prescriptions, and durable medical equipment. The key condition: treatment must be from an authorized physician and related to the accepted workplace injury.

In Florida, the insurance carrier — not the employer — designates the authorized treating physician. Employees have a one-time right to change physicians within the carrier’s network if dissatisfied with the initial assignment. This request must be made in writing. Outside of that one-time change, employees are generally treated by the carrier’s authorized physician, though they may request additional opinions in certain circumstances or petition the system for a change if care is inadequate.

Yes — medically necessary surgery related to your workplace injury is fully covered under workers’ comp with no cost to you. However, most surgeries require pre-authorization from the insurance carrier before they will pay.

MMI is the point at which your authorized physician determines your condition has stabilized and further treatment is unlikely to produce improvement. It does not mean you are fully healed — it means the medical trajectory has plateaued. At MMI, active treatment typically ends, though ongoing care may continue for chronic conditions arising from the injury if authorized. If you have permanent impairment, you may qualify for Impairment Income Benefits. Medical coverage does not end abruptly at MMI — any medically necessary care for your workplace injury after MMI still requires carrier authorization but can be provided.

Ensure Your Workers’ Comp Coverage Delivers the Medical Benefits Employees Deserve

Workers’ compensation medical coverage is the cornerstone of workplace injury protection for employees, it eliminates the financial barrier to care; for employers, it provides the structured system that replaces open-ended personal liability. The right workers’ comp policy, properly structured and correctly classified, ensures every claim is handled efficiently and every injured worker receives the treatment they’re legally entitled to.

Our commercial insurance advisors help Florida and nationwide businesses structure workers’ compensation coverage that is competitively priced, correctly classified, and fully compliant. Explore our complete workers’ comp coverages including medical injury coverage, lost wage protection, death and survivor benefits, and state compliance and legal security or contact us for a workers’ comp review today.