A workplace injury takes more than a physical toll. When an employee cannot work or can only work limited hours the financial pressure on their household begins immediately. Workers’ compensation lost wage protection is the benefit that bridges that gap, replacing a portion of income while the employee recovers.

Unlike workers’ comp medical coverage which pays 100% of authorized treatment with no out-of-pocket cost wage replacement benefits are calculated based on a formula, not paid at full salary. Understanding exactly how each benefit type is calculated, what the 2026 caps are, and when each type applies is essential knowledge for any employer carrying workers’ compensation insurance.

This guide breaks down all four wage replacement benefit types in Florida’s workers’ comp system, shows the exact calculation formulas with examples, and explains how the benefit timeline flows from initial injury through maximum medical improvement (MMI).

1. Calculating Your Average Weekly Wage (AWW)

Every workers’ comp wage benefit in Florida starts with the same number: the Average Weekly Wage (AWW). This is the foundation of all benefit calculations. Getting it right and making sure the carrier calculates it correctly is one of the most consequential steps in the claims process.

Florida calculates AWW based on the employee’s earnings over the 13 weeks immediately before the date of injury. The total earnings across those 13 weeks are divided by 13 to arrive at the weekly average. What counts as earnings:

- Gross wages before tax, not take-home pay

- Regular overtime and shift differentials

- Tips and gratuities (where applicable)

- Market value of board, lodging, or fuel provided by the employer

- Bonuses or commissions earned during the 13-week period

Common AWW errors that reduce employee benefits: using net pay instead of gross wages, excluding overtime, or using fewer than 13 weeks. Employers and their carriers are required to use the full 13-week period and include all wage components. If an employee has worked for less than 13 weeks, the carrier calculates AWW based on the available data or uses comparable employees’ wages.

For seasonal or part-time employees, AWW calculation may require adjustment consult the specific provisions under Chapter 440 of the Florida Statutes or discuss with your workers’ comp advisor.

The Four Types of Wage Replacement Benefits — 2026

Florida workers’ comp provides four distinct wage replacement benefit types, each applying at a different phase of recovery. The type of benefit an injured employee qualifies for depends on their work capacity as determined by the authorized treating physician:

| Benefit Type | When It Applies | How It’s Calculated | Duration |

|---|---|---|---|

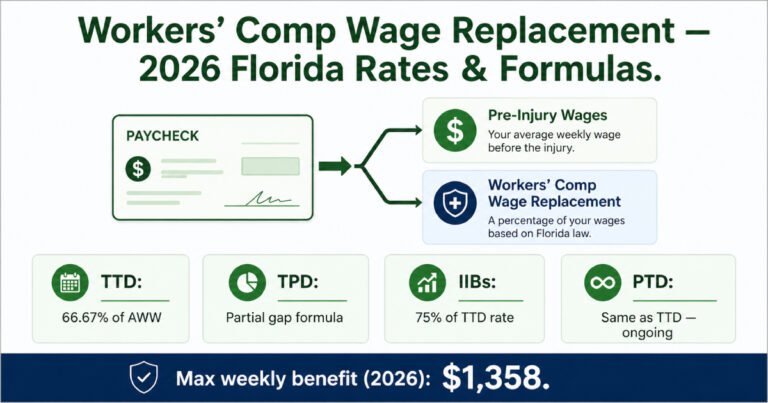

| Temporary Total Disability (TTD) | Cannot work at all | 66.67% of AWW — up to $1,358/week max (2026). 80% of AWW for up to 6 months for certain severe injuries. | Up to 104 weeks, or until MMI — whichever comes first |

| Temporary Partial Disability (TPD) | Working with restrictions at reduced wages (less than 80% of pre-injury AWW) | (AWW × 80%) − current earnings × 80%. Example: AWW $1,000 → 80% = $800 − $600 current = $200 × 80% = $160/week | Up to 260 total weeks combined with TTD |

| Impairment Income Benefits (IIBs) | After MMI — permanent impairment rating assigned | 75% of TTD rate. $600 TTD rate → $450/week IIBs. Duration tied to impairment percentage (2–6 weeks per % point) | Varies: 2 wks/pt for 1–10%, 3 wks/pt for 11–15%, 4 wks/pt for 16–20%, 6 wks/pt for 21%+ |

| Permanent Total Disability (PTD) | Permanently unable to perform any work | Same as TTD: 66.67% of AWW up to $1,358/week cap | Ongoing — may continue indefinitely or until statutory limits |

Temporary Total Disability (TTD): When You Cannot Work at All

TTD is the most common wage replacement benefit and applies when the authorized physician determines the injured employee is unable to perform any work during recovery. The formula is straightforward:

TTD benefit = AWW × 66.67%, subject to $1,358/week maximum (2026)

For severe injuries typically those resulting in hospitalization, major surgery, or significant functional loss Florida law allows TTD to be paid at 80% of AWW for the first six months, subject to the same weekly cap.

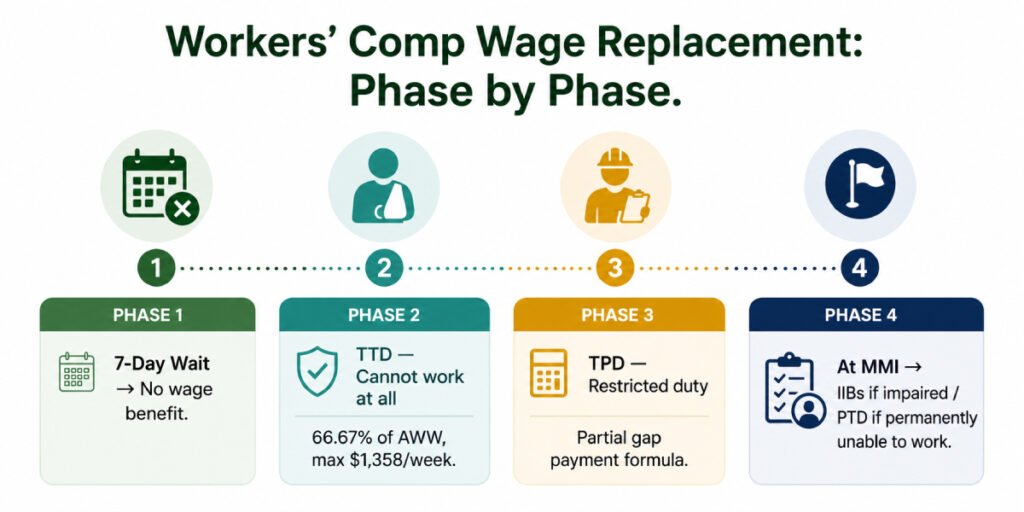

The 7-Day Waiting Period

TTD and all wage benefits have a 7-day waiting period: no compensation is paid for the first seven days of disability. However, if the disability lasts more than 21 days, the carrier must pay the first seven days retroactively. For injuries with a short recovery period, the waiting period means some employees receive no wage benefit at all. For longer recoveries, the first week’s benefit eventually arrives.

| Scenario | Pre-Injury AWW | TTD Weekly Benefit | Note |

|---|---|---|---|

| Employee earning $800/week | $800 | $533/week (66.67% of $800) | Well below $1,358 cap — full 66.67% applies |

| Employee earning $1,500/week | $1,500 | $1,000/week (66.67% of $1,500) | Below cap — full rate applies |

| Employee earning $2,200/week | $2,200 | Capped at $1,358/week | 66.67% of $2,200 = $1,467 — exceeds cap, so receives $1,358 |

| Employee earning $3,500/week | $3,500 | Capped at $1,358/week | Maximum benefit regardless of wages above the cap |

Temporary Partial Disability (TPD): When You Return to Work at Reduced Capacity

When the authorized physician releases an employee to return to work with restrictions shorter hours, lighter duties, or a different role and the employee earns less than 80% of their pre-injury AWW, they qualify for TPD. This benefit bridges the gap between their reduced earnings and what they would have earned before the injury.

TPD formula: (AWW × 80%) − current earnings × 80% = TPD weekly benefit

Example: Employee’s AWW before injury = $1,000. Returns to restricted duty earning $600/week.

- Step 1: AWW × 80% = $1,000 × 0.80 = $800

- Step 2: $800 − current earnings ($600) = $200

- Step 3: $200 × 80% = $160/week in TPD benefits (plus $600 from restricted duty = $760 total weekly income)

TPD ends when the employee earns 80% or more of their pre-injury AWW, reaches MMI, or hits the 260-week combined TTD+TPD cap. Employers can significantly reduce TPD exposure by offering a suitable restricted-duty position an employee working in a modified role and earning 80%+ of their pre-injury wages does not qualify for TPD payments.

Impairment Income Benefits (IIBs): Compensation for Lasting Physical Damage

When an employee reaches Maximum Medical Improvement (MMI) — the point where the authorized physician determines the condition has stabilized — TTD and TPD benefits end. If the employee has a permanent impairment rating above zero, they transition to Impairment Income Benefits (IIBs).

IIB weekly amount = 75% of TTD rate

Example: An employee with a TTD rate of $800/week receives IIBs of $600/week. The duration of IIBs is determined by the impairment percentage using a tiered schedule — this is why impairment ratings are often disputed between the employee and the carrier.

- 1–10% impairment: 2 weeks of IIBs per percentage point

- 11–15%: 3 weeks per point for that range

- 16–20%: 4 weeks per point for that range

- 21% and above: 6 weeks per point for that range

Example: 15% impairment rating → 10 points at 2 weeks (20 weeks) + 5 points at 3 weeks (15 weeks) = 35 total weeks of IIBs.

If an employee returns to work earning at or above their pre-injury wages while receiving IIBs, the benefit is reduced by 50%. IIBs are paid bi-weekly regardless of work status until the calculated weeks are exhausted.

Permanent Total Disability (PTD): When the Injury Ends the Ability to Work

PTD applies when an employee’s work-related injury leaves them permanently unable to perform any work. PTD benefits are paid at the same rate as TTD — 66.67% of AWW up to $1,358/week — but are ongoing rather than temporary. They may continue indefinitely, subject to statutory limits that vary based on injury type and date.

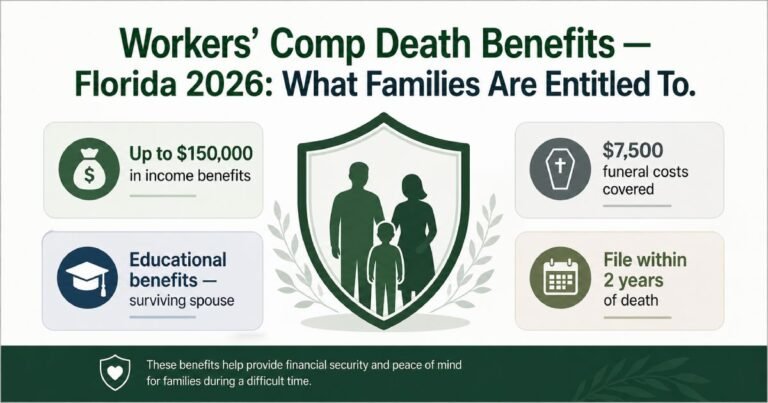

PTD claims are among the most significant workers’ comp liabilities an employer can face, and are among the reasons that adequate workers’ comp coverage matters far beyond basic compliance. A single PTD claim can generate decades of wage benefit payments. For context, see our guide on death and survivor benefits which apply when a work-related injury results in death rather than permanent disability.

What Wage Benefits Mean for Employers and How Coverage Protects You

Every dollar of TTD, TPD, IIB, and PTD paid to an injured employee flows through the employer’s workers’ compensation policy. Without coverage, the employer pays these amounts directly — and the financial exposure is open-ended. A construction worker injured with a PTD outcome could generate $1,000+ per week in wage benefits for decades, plus all medical costs, plus potential death or survivor benefits if complications arise.

Employers can reduce wage benefit exposure through three practices:

- Return-to-work programs: Offering modified or restricted duty positions eliminates TPD payments and keeps experienced workers active during recovery. This is one of the highest-return investments in workers’ comp cost management

- Accurate AWW documentation: Payroll records and timekeeping accuracy directly affect AWW calculations. Inaccurate records benefit neither the employer nor the employee and can create disputes that delay claims resolution

- Claims management and early intervention: Engaging with the authorized medical provider early, facilitating prompt treatment, and communicating light-duty availability to the carrier all accelerate recovery timelines and reduce total benefit duration

Frequently Asked Questions: Workers’ Comp Lost Wage Benefits

No — Florida workers’ comp does not replace 100% of wages. TTD pays 66.67% (two-thirds) of your pre-injury Average Weekly Wage, up to the 2026 state maximum of $1,358/week. For employees earning above the cap threshold, the effective replacement rate is even lower. The 66.67% structure reflects the historical trade-off: employees receive benefits without needing to prove fault, but at reduced wages. Medical benefits, however, are paid at 100% with no out-of-pocket cost.

Florida has a 7-day waiting period before wage replacement benefits begin — no payment is made for the first seven days of disability. However, if the disability lasts more than 21 days, the carrier must pay that first week retroactively. For injuries where the employee returns to work within 21 days, the first week’s wages are not recovered. Benefits are typically paid bi-weekly once the waiting period is satisfied and the claim is accepted.

At MMI, TTD and TPD benefits end. If the authorized physician assigns a permanent impairment rating above zero, the employee transitions to Impairment Income Benefits (IIBs) — paid at 75% of the TTD rate for a defined number of weeks tied to the impairment percentage. If the employee is permanently unable to work, they may qualify for Permanent Total Disability (PTD) benefits at the full TTD rate on an ongoing basis. Post-MMI medical treatment for the workplace injury may continue with carrier authorization.

Ensure Your Workers’ Comp Policy Covers Every Phase of a Wage Claim

Workers’ comp wage replacement benefits can run for months or years. From the initial medical treatment through TTD, TPD, and IIBs, through permanent disability or death benefits, the total liability exposure of a single serious work injury can be substantial. The right workers’ compensation policy correctly classified, properly priced, and fully compliant with Florida law is what converts that open-ended liability into a managed, insured cost.Our advisors help Florida businesses structure workers’ comp programs that are competitively priced and built for how their workforce actually operates. Review our lost wage protection page, the complete workers’ compensation coverage program, and contact us for a workers’ comp review today.