If you own a business whether it’s a landscaping crew, a retail boutique, a construction firm, or a consulting practice one question you can’t afford to leave unanswered is: what does commercial insurance actually cover? The short answer is: a lot. The more important answer is that the right business insurance coverage can be the difference between a setback and a complete financial collapse.

Commercial insurance is an umbrella term for a family of policies specifically designed to protect businesses from the financial consequences of accidents, lawsuits, property damage, employee injuries, and other risks that come with running a company. Unlike personal lines insurance, these policies are built around the unique liabilities and exposures that businesses face every single day.

This guide breaks down what commercial insurance is, what the main types of commercial insurance cover, and how small business owners can think strategically about protecting their operations.

What Is Commercial Insurance?

Commercial insurance also called business insurance is a category of insurance products purchased by businesses rather than individuals. These policies are underwritten with the understanding that business operations carry specific risks: employees can get hurt, customers can sue, vehicles can be involved in accidents, and physical property can be damaged or destroyed.

While personal insurance policies (like your home or auto insurance) cover you as an individual, commercial policies are designed to protect the legal and financial structure of your business entity whether that’s a sole proprietorship, LLC, partnership, or corporation.

In the United States, some forms of commercial insurance are legally required (like workers’ compensation in most states), while others are strongly recommended based on your industry and risk profile. Together, they form a risk management foundation that keeps businesses operational even after costly incidents.

For a complete overview of the commercial coverage options available to Florida and nationwide businesses, visit our commercial insurance hub.

The Main Types of Commercial Insurance Coverage

No two businesses have the same risk exposure, but most small businesses will encounter a core set of insurance needs. Here’s a breakdown of the primary types of commercial insurance and what they cover.

Commercial Insurance Coverage at a Glance

| Coverage Type | What It Protects | Who Needs It |

|---|---|---|

| General Liability | Third-party bodily injury, property damage, advertising injury | Almost every business |

| Commercial Auto | Business vehicle accidents, damage, theft | Businesses with company vehicles or drivers |

| Business Owners Policy (BOP) | GL + property + business income in one package | Small to mid-size businesses |

| Workers’ Compensation | Employee work-related injuries, lost wages, medical costs | Businesses with employees (required in most states) |

| Commercial Property | Buildings, equipment, inventory against fire, theft, disaster | Businesses with physical assets |

| Professional Liability (E&O) | Errors, omissions, negligence in professional services | Consultants, contractors, service providers |

1. General Liability Insurance

General liability (GL) is the most foundational form of business insurance and is often the first policy a new business purchases. It protects against claims that your business caused bodily injury or property damage to a third party, and it also covers certain advertising and personal injury claims.

For example, if a customer slips and falls in your store, or if your employee accidentally damages a client’s property while on a job site, your general liability policy steps in to cover legal defense costs, settlements, and medical expenses.

Our general liability insurance page outlines the full scope of GL coverage, including:

- Bodily injury liability — covering injuries to non-employees on your premises or caused by your operations

- Personal and advertising injury — protecting against libel, slander, or copyright infringement claims

- Products and completed operations — covering liability arising from products you sell or work you’ve completed

- Property damage liability — paying for damage your business causes to someone else’s property

2. Commercial Auto Insurance

If your business owns or operates vehicles from delivery vans to service trucks to company cars commercial auto insurance is not optional. Personal auto policies explicitly exclude coverage for vehicles used for business purposes, which means a gap in coverage could leave you personally liable for a serious accident.

Commercial auto policies typically include:

- Commercial auto liability coverage — for bodily injury and property damage you cause to others

- Collision coverage for commercial vehicles — for damage to your vehicles in at-fault accidents

- Comprehensive coverage for business fleets — for non-collision losses like theft, fire, or weather damage

- Hired and non-owned auto insurance — for vehicles your business rents or that employees use for work in their personal cars

See our existing comparison of commercial vs. personal auto insurance to understand why separate policies matter.

3. Business Owners Policy (BOP)

A Business Owners Policy (BOP) is a bundled insurance solution that combines the most essential coverages for small and mid-size businesses into a single, cost-effective package. It typically includes general liability, commercial property insurance, and business income coverage all under one policy.

Key components of a BOP include:

- Property coverage — protecting your building, equipment, inventory, and business personal property

- General liability under BOP — standard third-party bodily injury and property damage protection

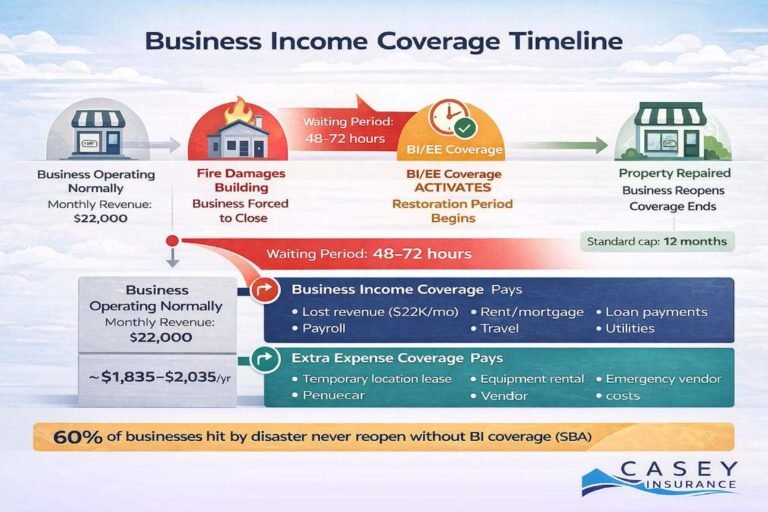

- Business income and extra expense coverage — replacing lost revenue if a covered event forces you to temporarily close

- Optional endorsements — add-ons like data breach, equipment breakdown, or professional liability coverage

BOPs are not available to all businesses insurers evaluate factors like industry type, revenue, and location. However, for eligible businesses, a BOP is often the most efficient entry point into comprehensive commercial coverage.

4. Workers’ Compensation Insurance

Workers’ compensation is required by law in most U.S. states for businesses with employees. It covers the costs associated with work-related injuries and illnesses, ensuring that injured employees receive medical care and wage replacement without the employer facing a devastating lawsuit.

Our workers’ compensation insurance coverage includes:

- Medical and injury coverage — paying for treatment of work-related injuries or occupational illnesses

- Lost wage protection — replacing a portion of income while an employee cannot work

- Death and survivor benefits — providing financial support to families of employees who die from work-related causes

- State compliance and legal security — keeping your business aligned with OSHA standards and state workers’ comp regulations

It’s worth noting the difference between workers’ comp and employers’ liability a distinction many business owners miss. Our blog on employers’ liability insurance vs. workers’ compensation covers this in detail.

What Factors Determine Your Business Insurance Coverage Needs?

Not every small business needs every type of commercial insurance. Your specific coverage needs will depend on several key factors:

- Industry and operations: A construction contractor faces very different risks than a graphic design studio. High-risk industries typically require broader coverage.

- Number of employees: The more employees you have, the greater your workers’ comp exposure and the more important employment practices liability coverage becomes.

- Physical location and assets: Businesses with buildings, equipment, or significant inventory need property protection. Florida businesses should also consider weather-related risks.

- Vehicles and driving exposure: Any business-related driving even employees using personal vehicles creates auto liability exposure.

- Contractual requirements: Many clients, landlords, and government contracts require proof of general liability coverage before you can begin work.

- State regulations: Workers’ compensation laws, auto insurance minimums, and other requirements vary significantly by state. Nationwide businesses must navigate multi-state compliance carefully.

Common Commercial Insurance Mistakes Small Businesses Make

Even business owners who carry insurance sometimes find themselves dangerously underprotected. Here are the most common mistakes to avoid:

- Assuming personal policies cover business activity: They don’t. Personal auto, homeowners, or umbrella policies typically exclude business-related losses.

- Skipping workers’ comp because ‘no one will get hurt’: Workplace injuries are unpredictable. One serious injury without coverage can result in devastating personal liability.

- Choosing the lowest premium without reading policy limits: A policy with a $300,000 liability limit may leave you exposed in a serious lawsuit. Coverage adequacy matters more than premium savings.

- Failing to update coverage as the business grows: A policy that made sense when you had 3 employees may be entirely inadequate when you have 25.

- Not understanding what’s excluded: Most standard commercial policies exclude floods, professional errors, and intentional acts. Optional endorsements or separate policies fill these gaps.

For a broader look at coverage gaps and policy errors, see our blog on common home and auto insurance mistakes to avoid many of the same principles apply to commercial coverage decisions.

How the Commercial Insurance Landscape Is Evolving

The commercial insurance industry is undergoing rapid change. Insurers are increasingly using data analytics, telematics, and artificial intelligence to price policies more accurately and process claims faster. For small business owners, this means more personalized coverage options but also a greater need to understand your actual risk profile. Our blog on how AI is changing insurance underwriting and claims explores how these shifts affect policyholders.

Beyond technology, regulatory changes at the state level continue to reshape compliance requirements particularly around workers’ compensation and commercial auto minimums. Working with an independent commercial insurance advisor ensures you stay current without having to track every legislative update yourself.

How to Find the Right Commercial Insurance for Your Small Business

The best approach to commercial insurance is a structured one. Start by identifying your highest-priority risks typically those that could put your business out of operation or expose you to personal financial liability. Then build outward from there.

A practical starting framework for most small businesses:

- Start with general liability it’s the baseline for most industries and often contractually required.

- Add workers’ compensation if you have any employees it’s legally required in most states and protects both parties.

- Evaluate a Business Owners Policy if you have physical business property and need income protection it’s often the most cost-efficient bundled solution.

- Layer commercial auto if any vehicles are used for business purposes personal auto won’t cover you.

- Consult a licensed advisor about specialized coverage professional liability, cyber insurance, commercial umbrella, and other policies based on your specific exposure.

Working with an independent insurance agency gives you access to multiple carriers and unbiased guidance ensuring you’re not overinsured in areas you don’t need and underprotected where it counts.

Frequently Asked Questions About Commercial Insurance

It depends on the type of coverage and your state. Workers’ compensation is legally required in most U.S. states for businesses with employees, and commercial auto insurance is required if your business owns vehicles. General liability is not universally mandated by law, but many clients, landlords, and licensing boards require it as a condition of doing business.

A Business Owners Policy (BOP) is a pre-packaged combination of general liability, commercial property, and business income coverage typically at a lower combined premium than buying each separately. A standalone commercial insurance policy refers to individual coverages purchased separately. BOPs are ideal for small to mid-size businesses; larger or higher-risk operations may need individually structured policies.

This varies by policy. Standard commercial property coverage generally does not extend to employees’ home offices or equipment. However, some BOP endorsements can be added to cover remote work scenarios. Workers’ compensation typically still applies to employees injured while working from home during the course of employment, even remotely. Always review your policy terms or consult your advisor.

Premiums vary widely based on industry, revenue, number of employees, location, claims history, and coverage types. A basic general liability policy for a low-risk small business might start around $500–$1,500 per year, while a comprehensive package including workers’ comp, commercial auto, and a BOP can range from several thousand to tens of thousands annually for larger or higher-risk operations. The only accurate way to know is to get a customized quote.

Yes and it’s often the smartest financial move. A Business Owners Policy is the most common bundled option, combining GL, property, and income protection. Beyond that, many insurers offer multi-policy discounts when you add commercial auto or workers’ comp through the same carrier. Bundling simplifies your coverage management and can meaningfully reduce overall premium costs.

Ready to Protect Your Business?

Commercial insurance is not a one-size-fits-all product and it shouldn’t be treated as a checkbox. The right coverage strategy is built around your specific business, your industry’s risk landscape, and your long-term growth plans. Whether you’re just getting started or reassessing your current coverage, our team is here to help you build a protection strategy that actually works.

Explore our full range of commercial insurance solutions, or reach out directly to speak with a licensed business insurance advisor today.