Your home is likely your largest investment and most valuable asset. Yet many homeowners don’t truly understand what their homeowners insurance covers or critically, what it excludes until they need to file a claim.

Discovering your policy doesn’t cover flood damage after water fills your basement, or learning that your stolen jewelry exceeded coverage limits, creates devastating financial consequences that proper understanding would have prevented. Homeowners insurance isn’t one-size-fits-all protection it’s a complex policy with specific coverages, limits, and exclusions you need to understand.

This comprehensive guide breaks down exactly what standard homeowners insurance covers, common exclusions that catch people off guard, and how to ensure you have adequate protection for your specific situation.

The Five Core Components of Homeowners Insurance

Standard homeowners policies (HO-3 is most common) include five distinct coverage sections protecting different aspects of your property and liability.

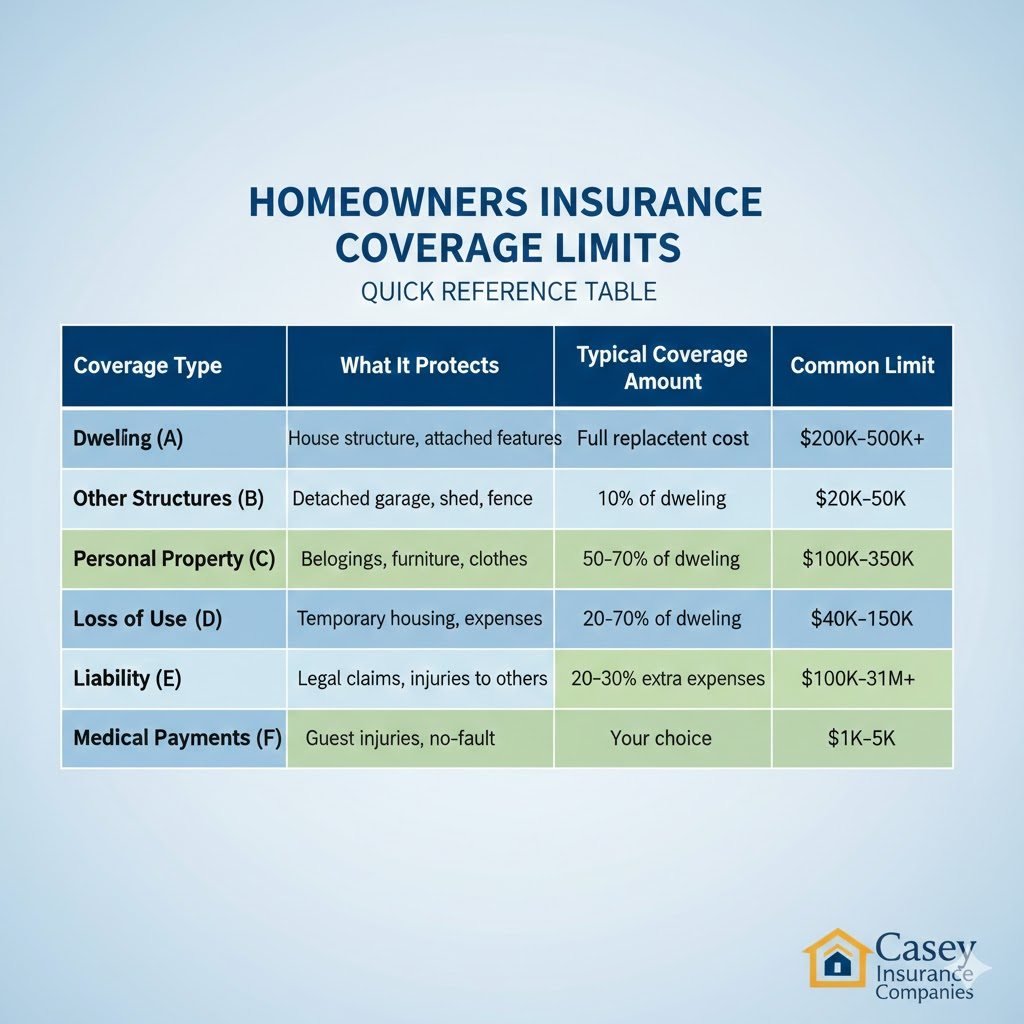

1. Dwelling Coverage (Coverage A)

Dwelling coverage protects your home’s physical structure the most important component of your policy.

What’s Covered:

- Main house structure (walls, roof, foundation)

- Attached structures (attached garages, decks, porches)

- Built-in appliances (furnace, water heater, central AC)

- Plumbing, electrical, and heating systems

- Permanently installed fixtures and features

Covered Perils:

- Fire and smoke damage

- Lightning strikes

- Windstorm and hail damage

- Vandalism and malicious mischief

- Theft of structural components

- Weight of ice, snow, or sleet

- Falling objects

- Water damage from burst pipes

- Explosion

Dwelling coverage pays to repair or rebuild your home after covered events. It’s typically the largest coverage amount on your policy should equal your home’s full replacement cost, not market value or tax assessment.

2. Other Structures Coverage (Coverage B)

This covers structures on your property not attached to your main house.

What’s Covered:

- Detached garages and sheds

- Fences and retaining walls

- Driveways and walkways

- Swimming pools and pool equipment

- Gazebos and pergolas

- Guest houses or mother-in-law suites

Coverage typically equals 10% of your dwelling coverage (adjustable if needed). If your dwelling coverage is $300,000, other structures coverage is $30,000 unless you increase it.

3. Personal Property Coverage (Coverage C)

Personal property coverage protects your belongings inside and outside your home.

What’s Covered:

- Furniture and appliances

- Clothing and shoes

- Electronics (TVs, computers, tablets)

- Kitchenware and dishes

- Books, artwork, and decorations

- Sports equipment

- Tools and lawn equipment

- Items temporarily away from home (luggage during travel, dorm room belongings)

Standard coverage equals 50-70% of dwelling coverage. A $300,000 dwelling typically includes $150,000-$210,000 personal property coverage.

Important Limitations:

- Jewelry, watches, furs: Often limited to $1,000-$2,500 total

- Cash and coins: Typically $200-$500 limit

- Firearms: Usually $2,000-$5,000 limit

- Silverware and gold: Limited coverage

- Electronics: Some policies sublimit electronics to $5,000-$10,000

- Business property: Limited or excluded entirely

High-value items require “scheduling” separately for full protection adding them with specific values and broader coverage.

4. Loss of Use Coverage (Coverage D)

Also called Additional Living Expenses (ALE), this pays costs when your home becomes uninhabitable due to covered damage.

What’s Covered:

- Hotel or temporary rental housing

- Restaurant meals (when you normally cook at home)

- Storage for belongings during repairs

- Increased commuting costs

- Pet boarding if necessary

Coverage typically equals 20-30% of dwelling coverage and applies for the time reasonably needed to repair or rebuild usually 12-24 months for major damage.

Example: Fire damages your home requiring 6 months of repairs. Your policy pays hotel costs ($4,000/month × 6 = $24,000) plus extra meal expenses ($1,500/month × 6 = $9,000), totaling $33,000 in loss of use coverage.

5. Personal Liability Coverage (Coverage E)

Liability coverage protects you from lawsuits when you’re responsible for injuries or property damage to others.

What’s Covered:

- Guest injuries on your property (slip-and-falls, dog bites, pool accidents)

- Injuries you or family members cause to others (accidentally hitting someone with a golf ball, your child damaging neighbor’s property)

- Legal defense costs if you’re sued

- Court judgments against you up to policy limits

Standard policies include $100,000-$300,000 liability coverage. Many experts recommend $500,000 minimum, with $1 million for substantial assets.

What Liability Doesn’t Cover:

- Intentional acts

- Business-related injuries

- Auto accidents (covered by auto insurance)

- Professional services liability

6. Medical Payments to Others (Coverage F)

This covers small medical expenses for guests injured on your property, regardless of fault.

What’s Covered:

- Medical bills up to policy limits (typically $1,000-$5,000)

- Emergency treatment

- Follow-up care within specified timeframes

This coverage prevents small injuries from becoming liability claims. If a guest trips and needs stitches, medical payments covers their treatment without determining fault or involving lawyers.

What Homeowners Insurance Typically Doesn’t Cover?

Understanding exclusions prevents devastating claim surprises.

Flood Damage

Not Covered: Flooding from external water sources rising rivers, storm surge, heavy rain runoff, or groundwater seepage.

Why: Flood risk requires specialized insurance through the National Flood Insurance Program (NFIP) or private flood insurers.

Exception: Water damage from internal sources (burst pipes, appliance leaks, roof leaks during storms) is typically covered.

Our Flood and Water Coverage specialists help homeowners understand and obtain necessary flood protection.

Earthquake Damage

Not Covered: Ground shaking, tremors, and related damage from earthquakes.

Why: Earthquake risk requires separate coverage via endorsements or standalone policies.

Where It Matters: Critical in California, Pacific Northwest, New Madrid Seismic Zone, and other earthquake-prone regions.

Routine Maintenance and Wear and Tear

Not Covered:

- Roof wear and aging requiring replacement

- HVAC systems failing from age

- Plumbing deterioration

- Paint, flooring, and cosmetic aging

- Pest damage (termites, rodents, insects)

Why: Insurance covers sudden, accidental damage not predictable maintenance and aging. Regular upkeep is your responsibility.

Intentional Damage

Not Covered: Deliberately causing damage to make insurance claims (fraud).

Business Activities

Not Covered: Liability or property damage from home-based businesses.

Why: Home offices and small businesses require commercial coverage or business endorsements.

Certain Water Damage

Limited Coverage:

- Slow leaks or seepage over time

- Sewer backup (often requires endorsement)

- Sump pump failure (may require endorsement)

- Water damage from lack of maintenance

Valuable Items Beyond Sublimits

Limited Coverage: As mentioned, jewelry, cash, firearms, and other valuables have sublimits. High-value items require scheduling.

Municipal Actions

Not Covered: Eminent domain, building code violations, or government-mandated repairs/demolitions.

Types of Homeowners Insurance Policies

Different policy types provide varying coverage levels.

HO-3 Policy (Special Form)

Most Common: 85% of homeowners have HO-3 policies.

Coverage: “All-risk” for dwelling (covers everything except specifically excluded perils), “named perils” for personal property (only covers listed events).

Best For: Most single-family homeowners.

HO-5 Policy (Comprehensive Form)

Premium Coverage: “All-risk” for both dwelling and personal property.

Benefits: Broader personal property protection with fewer exclusions.

Best For: High-value homes or owners with expensive belongings.

HO-6 Policy (Condo Insurance)

For Condos: Covers personal property and interior improvements.

Master Policy: Condo associations carry insurance for building exteriors and common areas.

Best For: Condominium unit owners.

HO-4 Policy (Renters Insurance)

For Renters: Covers personal property and liability, not the dwelling structure.

Best For: Apartment or house renters.

How Much Homeowners Insurance Coverage You Need

Proper coverage amounts prevent underinsurance disasters.

Dwelling Coverage Amount

Should Equal: Full replacement cost to rebuild your home at current construction prices not market value or mortgage amount.

How to Determine:

- Professional replacement cost estimates from builders

- Insurance company estimators

- Online replacement cost calculators (less accurate)

Common Mistake: Insuring for market value. If your home’s market value is $400,000 but rebuilding costs $500,000, you’re underinsured by $100,000.

Personal Property Coverage

Standard: 50-70% of dwelling coverage is typically adequate.

Evaluate Your Needs:

- Inventory your belongings

- Calculate total replacement costs

- Increase coverage if you own expensive furniture, electronics, or collections

Liability Coverage

Recommended Minimums:

- Basic: $300,000

- Standard: $500,000-$1 million

- High Assets: $1 million plus umbrella policy

Match liability coverage to your total net worth plaintiffs can pursue all your assets in lawsuits exceeding insurance limits.

Replacement Cost vs Actual Cash Value

This distinction dramatically affects claim payouts.

Replacement Cost Coverage

Pays: Full cost to replace damaged items with new equivalents at current prices.

Example: 5-year-old roof damaged by hail. Replacement cost coverage pays for a brand-new roof (~$15,000). You pay only your deductible.

Benefit: True replacement without depreciation.

Cost: 10-20% higher premiums than actual cash value.

Actual Cash Value Coverage

Pays: Replacement cost minus depreciation based on age and condition.

Example: Same 5-year-old roof. Actual cash value coverage pays depreciated value (~$9,000). You pay deductible plus $6,000 depreciation.

Benefit: Lower premiums.

Drawback: Insufficient for actual replacement you pay the gap.

Recommendation: Always choose replacement cost coverage for dwelling and personal property. The premium difference is minimal compared to claim benefits.

Homeowners Association (HOA) Insurance

If you live in an HOA community, understand coverage coordination.

What HOA Master Policies Cover

Common Areas: Clubhouses, pools, playgrounds, landscaping

Building Exteriors: In some cases, includes your unit’s exterior walls and roof

Shared Liability: Accidents in common areas

What Your Personal Policy Must Cover?

Interior: Everything inside your unit from walls inward

Personal Property: All your belongings

Personal Liability: Liability for incidents in your unit or caused by you

Loss Assessment Coverage: Fees if the HOA assesses homeowners for uncovered damages or liability judgments

Coverage Gaps to Watch For

Deductibles: HOA policies often have high deductibles ($10,000-$50,000). Loss assessment coverage helps pay these.

Coverage Limits: Ensure your personal policy doesn’t duplicate HOA coverage but fills gaps.

Improvements: Your upgrades to the unit (upgraded flooring, custom cabinets) may not be covered by the HOA policy.

Making Claims: What You Need to Know

Understanding the claims process prevents mistakes.

Document Damage Thoroughly

- Photograph and video all damage before any cleanup

- Make temporary repairs preventing further damage (save receipts)

- Keep damaged items until adjusters inspect them

- Maintain detailed records of all expenses

Report Claims Promptly

Most policies require “prompt” notification report within 24-72 hours when possible. Delays can jeopardize coverage.

Understand Your Deductible

You pay the deductible before insurance covers the rest. Typical deductibles: $500-$5,000 for standard claims, 1-10% of dwelling coverage for hurricanes/windstorms.

Don’t Accept Lowball Settlements

If initial settlement offers seem inadequate:

- Get independent estimates

- Document all damages thoroughly

- Request reconsideration with supporting evidence

- Consider public adjusters for large claims (they take 5-15% but may increase settlements significantly)

Reducing Your Homeowners Insurance Costs

Quality coverage doesn’t require overpaying.

Increase Your Deductible

Moving from $500 to $1,000-$2,500 deductibles saves 10-25% annually. Only choose deductibles you can afford during claims.

Bundle Policies

Combining homeowners with auto insurance saves 15-25% on both policies.

Improve Home Security

Security systems, smoke detectors, deadbolts, and fire alarms earn 5-20% discounts.

Maintain Good Credit

Better credit scores reduce premiums 20-50% in most states.

Shop and Compare Regularly

Review coverage and compare quotes every 2-3 years rates vary significantly between insurers.

Stay Claims-Free

Avoid filing small claims you can afford yourself. Claims-free discounts increase over time.

Your Path to Proper Protection

Homeowners insurance protects your largest asset and your financial security. Understanding what’s covered, recognizing exclusions, and ensuring adequate limits prevents devastating surprises when you need coverage most.

Don’t treat your homeowners policy as paperwork filed away and forgotten. Review it annually, update coverage when home improvements increase value, schedule high-value items properly, and close gaps with necessary endorsements.

Our Home Insurance specialists help homeowners understand their coverage, identify gaps, and build comprehensive protection matching their specific needs and property values.

Frequently Asked Questions

Standard policies often restrict or exclude coverage for homes vacant (completely empty) for 30-60+ consecutive days. Short vacations are fine, but extended absences require notifying your insurer. Some offer vacant home endorsements; others won’t cover vacant properties. Unoccupied homes (furnished but no one living there) may have limited coverage. Always notify insurers of extended absences.

Yes, if the tree causes structural damage. Your policy covers tree removal costs (typically $500-$1,500 per tree) only if it damaged covered structures. Trees falling without hitting structures aren’t covered for removal. If your neighbor’s tree falls on your house, your insurance still covers damage (then may pursue your neighbor’s insurance for reimbursement if the tree was diseased/neglected).

Generally no foundation issues from settling, soil movement, or normal aging aren’t covered. However, if sudden covered events (earthquakes with earthquake coverage, water main breaks, explosions) cause foundation damage, it may be covered. Regular foundation issues require maintenance and are your responsibility, not insurable events.