Choosing the right business insurance policy is one of the most consequential financial decisions a small business owner makes and yet it’s one of the most commonly rushed. Too many businesses buy the cheapest policy available, assume it covers everything, and only discover the gaps after a claim is denied.

In 2026, the stakes are higher than ever. Litigation costs continue to climb, workers’ compensation regulations are tightening in many states, and new exposures like cyber liability are reshaping what a complete small business insurance guide needs to address. The good news: choosing the best business insurance policy for your company doesn’t require a law degree it requires a structured approach and the right advisor.

This guide walks you through exactly that: how to assess your risk exposure, understand your legal requirements, select the right coverage types, and avoid the policy mistakes that leave businesses financially exposed when they can least afford it.

1: Understand Your Business Risk Profile Before You Buy Anything

The most common mistake small business owners make when shopping for insurance is starting with the price. The right starting point isn’t the premium it’s a clear-eyed assessment of what could actually go wrong in your specific business.

Ask yourself:

- Do customers, vendors, or the public interact with my business premises or my employees?

- Do I or my employees drive vehicles for work purposes even occasionally?

- Do I have employees who could be injured on the job?

- Do I have physical assets equipment, inventory, a leased or owned building that would be costly to replace?

- Could my business survive a 30-, 60-, or 90-day forced closure due to a fire, flood, or major incident?

- Do I provide professional advice, services, or products that a client could later claim caused them financial harm?

Your answers to these questions map directly to the types of coverage you need. A business that answers “yes” to most of these has substantial exposure across multiple coverage categories. A solo consultant working remotely may need far less but still needs something.

Understanding your risk profile is the foundation of a sound small business insurance guide. Every coverage decision flows from it.

2: Know Your Business Insurance Requirements by Law

Before selecting optional coverage, you need to understand which coverages are legally required. Business insurance requirements vary by state, industry, and even by contract but here are the non-negotiables most small businesses face:

Workers’ Compensation

In the vast majority of U.S. states, if you have employees, workers’ compensation insurance is legally required not optional. Florida, for example, requires workers’ comp for construction businesses with even one employee, and for non-construction businesses with four or more employees. Operating without it exposes you to stop-work orders, fines, and personal liability for injury costs.

The consequences of non-compliance are severe. OSHA regulations establish employer obligations for workplace safety, and workers’ comp sits alongside those obligations as a baseline legal protection. See our detailed breakdown of state compliance and legal security under workers’ comp to understand what your state requires.

Commercial Auto Insurance

If your business owns vehicles, state law requires commercial auto insurance personal auto policies won’t apply, and driving a business vehicle on a personal policy creates a coverage void that most business owners don’t discover until after an accident.

Contractual and Licensing Requirements

Beyond state law, general liability insurance is often required by landlords, general contractors, government agencies, and clients before you can sign a contract or obtain a business license. Many licensing boards in industries like construction, healthcare, and professional services mandate minimum GL limits as a condition of licensure. Always review your contracts before assuming you can self-insure.

3: Match Coverage to Your Specific Business Type and Operations

Once you know your risk profile and your legal minimums, the next step is building a coverage stack that actually fits how your business operates. Use the decision guide below as a starting framework:

Business Insurance Coverage Decision Guide

| Your Business Situation | Coverage to Consider | Why It Matters |

|---|---|---|

| I have employees | Workers’ Compensation | Required in most states — legally non-negotiable |

| I own or lease business vehicles | Commercial Auto Insurance | Personal auto won’t cover business use — ever |

| Customers visit my location or I visit theirs | General Liability (GL) | Slip-and-fall, property damage, third-party claims |

| I have physical property, equipment, or inventory | BOP or Commercial Property | Protects assets from fire, theft, weather, vandalism |

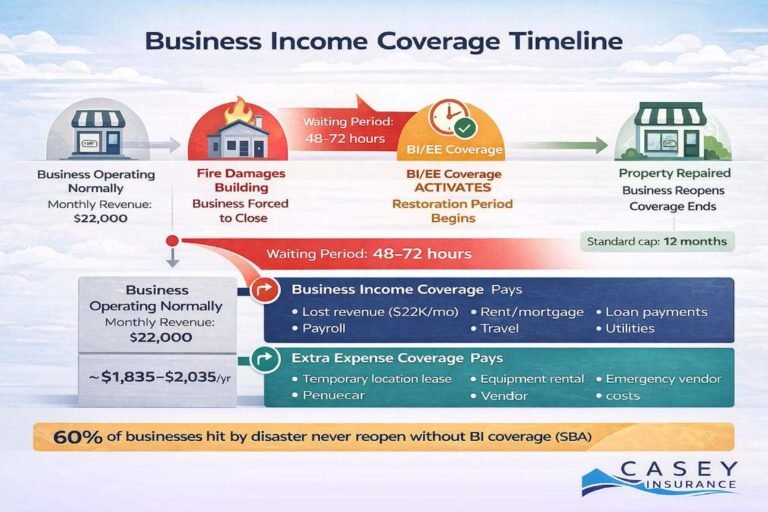

| My business could face a revenue interruption | Business Income Coverage (BOP) | Replaces lost income if you’re forced to temporarily close |

| I provide professional advice or services | Professional Liability (E&O) | Covers claims of negligence, errors, or omissions |

| I collect or store customer data | Cyber Liability | Growing requirement — standard GL does not cover data breaches |

| I have significant overall liability exposure | Commercial Umbrella | Extends limits above your primary policies |

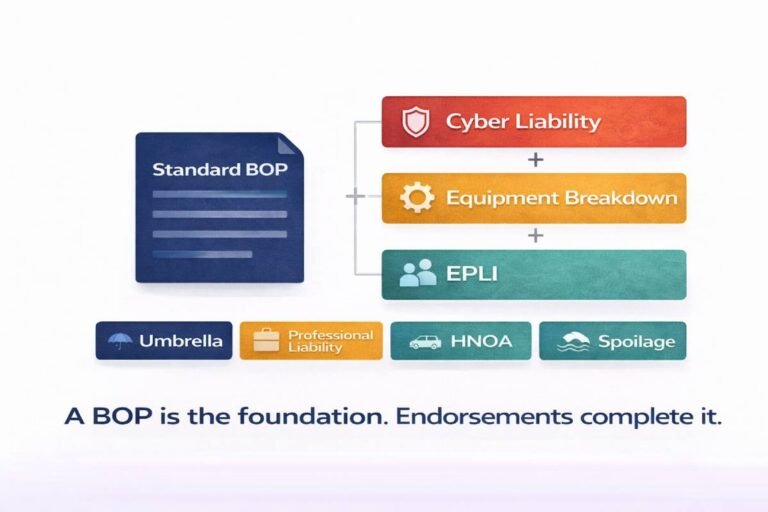

For most small businesses, the most efficient entry point is a Business Owners Policy (BOP) which bundles general liability, commercial property, and business income coverage into a single package at a lower combined cost than buying each separately. If your business qualifies for a BOP, it’s almost always the right foundation to build from.

4: Choose the Right Policy Limits – Not Just the Lowest Premium

One of the most dangerous habits in small business insurance shopping is selecting coverage limits based purely on what keeps the premium low. A policy that’s inadequate when you need it is effectively no policy at all. Here’s a practical guide to typical coverage limits and what to consider:

Commercial Insurance Policy Limits — 2026

| Coverage | Typical Limit Range | Who Needs It | Advisor Tip |

|---|---|---|---|

| General Liability | $1M per occurrence / $2M aggregate | Most small businesses | Low-risk: may suffice; High-risk: consider umbrella |

| Commercial Auto Liability | $500K–$1M combined single limit | All business vehicle operators | Florida minimum is low — carry more |

| Workers’ Compensation | State-mandated (no-fault) | All employers with staff | Required minimums vary by state |

| BOP Property | Replacement cost of assets | Physical business locations | Underinsuring assets is a common mistake |

The Occurrence Limit vs. Aggregate Limit Distinction

Occurrence limit is the maximum your policy pays for any single claim. The aggregate limit is the maximum it pays across all claims in a policy year. A $1M / $2M GL policy the most common standard for small businesses means up to $1M per incident and $2M total annually. If your industry or contract requires higher limits, a commercial umbrella policy is the most cost-effective way to extend them without restructuring your primary coverage.

5: Decide Between a BOP and Standalone Policies

This is one of the most common questions of all small business insurance owner: should you purchase a Business Owners Policy or build a custom stack of standalone coverages?

Choose a BOP if:

- Your business is small to mid-size (typically under $5M in revenue)

- You have a physical business location with property to protect

- You want to simplify policy management with one carrier and one renewal date

- You need bundled business income protection alongside GL and property

- Your industry qualifies BOPs are not available to all business types (construction, for example, is often excluded)

Choose standalone policies if:

- Your business is in a higher-risk industry that doesn’t qualify for a BOP

- You need highly customized coverage limits that exceed standard BOP options

- You already have a specialized carrier for one coverage type and want to keep it

- Your operation is complex enough to require separate policy management by risk category

Explore the full breakdown of BOP coverage components, including property coverage, general liability under BOP, business income and extra expense coverage, and optional endorsements to see how a BOP can be tailored to your operations.

6: Work With an Independent Commercial Insurance Advisor

The policy comparison process is significantly more complex than it appears on a comparison website. Insurers use different policy language, exclusions, and endorsement structures that make apples-to-apples comparisons nearly impossible without professional guidance. An independent commercial insurance advisor works with multiple carriers not just one and can identify coverage gaps, negotiate better terms, and ensure your policy actually does what you think it does.

When evaluating an insurance advisor or agency, ask:

- Do you specialize in commercial insurance, or is it a secondary line?

- Which carriers do you represent, and can you shop the market on my behalf?

- Can you walk me through the exclusions on any policy you recommend?

- How do you handle claims support will you advocate for me if a claim is disputed?

- How often will you review my coverage as my business grows?

The distinction between captive agents (who represent one carrier) and independent brokers is significant and worth understanding before you buy. Our blog on independent marine insurance brokers vs. direct insurers covers this dynamic in depth, and the same principles apply to commercial insurance.

What’s Changed in the Commercial Insurance Landscape in 2026

The business insurance market in 2026 looks meaningfully different from even three years ago. Several trends are directly affecting small business coverage decisions:

Cyber Liability Is No Longer Optional for Most Businesses

Standard general liability and BOP policies do not cover data breaches, ransomware attacks, or regulatory penalties from privacy violations. As cyber incidents targeting small businesses continue to rise, cyber liability coverage has shifted from a specialty add-on to a near-essential endorsement. This can often be added via BOP optional endorsements.

Workers’ Comp Is Expanding to Cover Remote and Gig Workers

State legislatures are actively revising workers’ compensation statutes to address remote work injuries and gig economy classifications. If any of your employees work from home even part-time you should confirm with your advisor that your workers’ comp policy addresses those scenarios explicitly.

Hired and Non-Owned Auto Exposure Is Growing

More businesses are relying on employees using personal vehicles for deliveries, client visits, and errands without realizing this creates a liability exposure their commercial auto policy may not cover. Hired and non-owned auto insurance (HNOA) has become an increasingly important endorsement for service businesses, staffing firms, and any company with field-based employees.

AI-Driven Underwriting Is Changing How Policies Are Priced

Insurers are increasingly using real-time data, telematics, and AI-based risk scoring to price commercial policies. This benefits businesses with strong safety records and clean claims histories but it also means your past claims data has more influence on your current premium than ever before. Our blog on how AI is changing insurance underwriting and claims explains how this affects policyholders in practical terms.

7 Business Insurance Mistakes to Avoid When Choosing a Policy

- Buying the cheapest policy without reading the exclusions. Exclusions can be more important than the coverage itself.

- Assuming your personal auto or home insurance covers business activity. It doesn’t not for vehicles, property, or liability.

- Not updating your coverage as your business grows. A policy that fit a 5-person team may leave a 20-person team dangerously exposed.

- Skipping business income coverage. A single forced closure from a fire, flood, or covered loss can generate months of lost revenue. Without it, recovery becomes a personal financial crisis.

- Treating workers’ comp as optional if you have employees. It’s not. One serious workplace injury without coverage can result in devastating personal liability and regulatory penalties.

- Ignoring the difference between occurrence and claims-made policies. The timing of when a claim is filed vs. when the incident occurred matters significantly for professional liability and some GL policies.

- Not asking about bundling discounts. Combining GL, commercial auto, and workers’ comp with the same carrier often yields meaningful premium reductions.

For a broader look at policy errors, see our coverage of commercial auto insurance coverage mistakes businesses make several of the same principles apply across all commercial lines.

Frequently Asked Questions: Choosing the Best Business Insurance Policy

Start with your risk profile who you interact with, whether you have employees, whether you drive for business, and what physical assets you own. From there, layer in your legal requirements (workers’ comp, commercial auto). A licensed independent insurance advisor can then match those factors to the right coverage types and policy limits.

For many small businesses, a BOP is an excellent foundation but it’s rarely sufficient on its own. BOPs do not include workers’ compensation or commercial auto coverage, both of which most businesses need separately. Depending on your industry, you may also need professional liability or cyber endorsements. Think of a BOP as the core, not the complete picture.

Florida law requires workers’ compensation for construction companies with one or more employees and non-construction businesses with four or more. Commercial auto is required for any business-owned vehicles. General liability is not state-mandated, but is typically required by contracts, leases, and licensing boards. Minimums differ by industry, so consult a licensed Florida insurance advisor for your specific situation.

Generally, yes commercial insurance premiums paid for policies that protect your business operations are considered ordinary and necessary business expenses and are typically tax-deductible. This includes general liability, commercial auto, workers’ comp, and BOP premiums. Always confirm with your accountant or tax advisor for your specific situation.

At minimum, review your coverage annually at renewal. Beyond that, trigger a coverage review whenever your business experiences a significant change: hiring employees, purchasing vehicles or equipment, moving to a new location, adding a new service line, or taking on a major new client contract. Your coverage needs in year three of business will likely look very different from year one.

Build a Policy That Actually Protects Your Business

The best business insurance policy isn’t the one with the lowest premium it’s the one that actually responds when something goes wrong. In 2026, with evolving regulations, new exposures, and rising litigation costs, small business owners cannot afford to treat insurance as an afterthought.

Whether you’re building your first commercial coverage stack or reassessing what you have, our team of experienced commercial insurance advisors is ready to help.