A customer slips and falls in your retail store. A kitchen fire forces your restaurant to close for five weeks. A break-in destroys $40,000 worth of inventory. A storm damages your office building and everything inside it.

For most small businesses, any one of these scenarios uninsured would be financially devastating. Together, they represent the core risks that a Business Owners Policy (BOP) is specifically designed to protect against. A BOP is not a single coverage it is a bundled insurance policy that combines three essential protections into one contract, at one premium, with one renewal date.

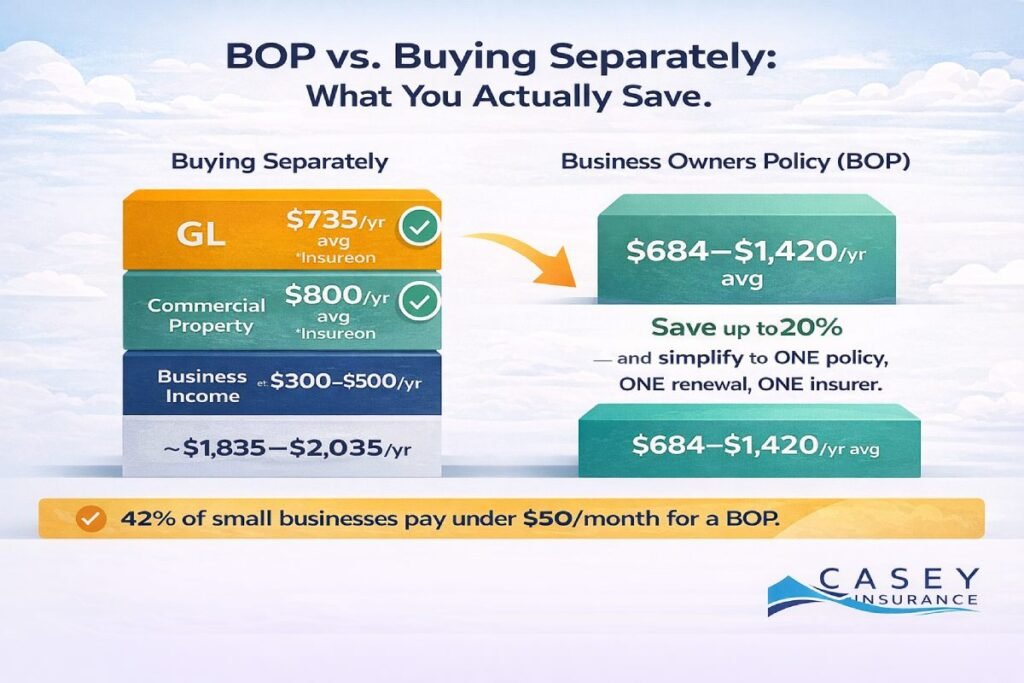

In 2026, a BOP remains the most efficient and cost-effective starting point for small and mid-size businesses that have a physical presence, business property, and customer-facing operations. According to Insureon, 42% of small businesses pay less than $50 per month for a BOP and most pay less than they would buying the same coverages separately.

Here we’ll explain exactly what a BOP covers, who it’s designed for, what it costs by industry, when it’s not the right fit, and how to find the best BOP insurance for your specific business in 2026.

BOP by the Numbers — 2026

National average BOP cost: $57–$147/month depending on source and industry profile.

Florida average: $76/month. 42% of small businesses pay under $50/month. 87% of small business BOP customers choose a $1M/$2M liability limit. Businesses save up to 20% by bundling GL + Property in a BOP vs. buying separately.

What Is a Business Owners Policy (BOP)?

A Business Owners Policy (BOP) is a commercial insurance package that bundles general liability insurance, commercial property insurance, and business income (interruption) coverage into a single policy. It was developed by insurers as a standardized, cost-efficient solution for small and mid-size businesses whose risk profiles are well-understood and relatively predictable.

The bundling structure offers two key advantages: lower total premium (up to 20% less than buying the same coverages separately, and simplified policy management — one insurer, one invoice, one renewal date, one claims contact for events that often trigger both liability and property coverage simultaneously.

Here is what each of the three core coverage components inside a BOP actually does:

What’s Inside a Business Owners Policy — The Three Core Coverages

| Coverage Component | What It Covers | Real-World Example |

|---|---|---|

| General Liability (GL) | Pays for third-party bodily injury, property damage, and personal & advertising injury claims. Covers legal defense + settlements. Standard limit: $1M per occurrence / $2M aggregate (87% of small businesses choose this — Insureon 2026) | A customer slips in your retail store; a client’s property is damaged during a service visit; a social post generates an advertising injury claim |

| Commercial Property | Pays to repair or replace your owned or leased building, business equipment, inventory, furniture, and fixtures after a covered event: fire, theft, vandalism, storm damage, and more | Office fire destroys computers and furniture; retail theft wipes out inventory; a storm damages your storefront sign and display windows |

| Business Income / Extra Expense (BI/EE) | Pays for lost revenue and continuing operating expenses (rent, payroll, utilities) while your business is closed for repairs after a covered property loss. Extra Expense covers the cost of operating from a temporary location | A kitchen fire forces your restaurant to close for six weeks; flood damage shuts your salon; a burst pipe closes your office — BI/EE replaces the income and pays your bills while repairs happen |

What a BOP Does Not Cover Important Gaps to Know

A BOP is comprehensive for standard small business risk but it is not all-encompassing. Understanding its exclusions is as important as understanding its inclusions. Key coverages not included in a standard BOP:

- Workers’ compensation: Required by law in most states once you have employees. Must be purchased separately a BOP does not cover your employees’ work-related injuries or illnesses.

- Commercial auto insurance: A BOP does not cover business vehicles. If your business owns, leases, or regularly uses vehicles for operations, a separate commercial auto policy is required.

- Professional liability (E&O): If your business provides advice, professional services, or consulting, errors and omissions coverage is not part of a standard BOP. It must be added as an endorsement or purchased separately.

- Cyber liability: Data breach, ransomware, and cyber extortion are not covered under standard BOP property or liability components. Cyber liability must be added as a BOP endorsement or standalone policy — and in 2026, with cyber incidents rising across small business sectors, it is increasingly essential.

- Flood and earthquake: Standard BOP property coverage excludes flood and earthquake damage. In Florida, where storm surge and flooding are primary commercial property risks, a separate flood insurance policy (NFIP or private market) is essential for most businesses with a physical location.

- EPLI (Employment Practices Liability): Wrongful termination, discrimination, and harassment claims are not covered under a BOP’s general liability component. EPLI must be added separately.

Smart BOP Strategy

Start with the core BOP bundle, then extend it with endorsements that match your specific risk profile. Cyber liability, equipment breakdown, and EPLI are the three most commonly added BOP endorsements for small businesses in 2026. Each typically adds $20–$80/month to your BOP premium far less than standalone policy pricing. Explore the full range of available add-ons on our BOP optional endorsements page.

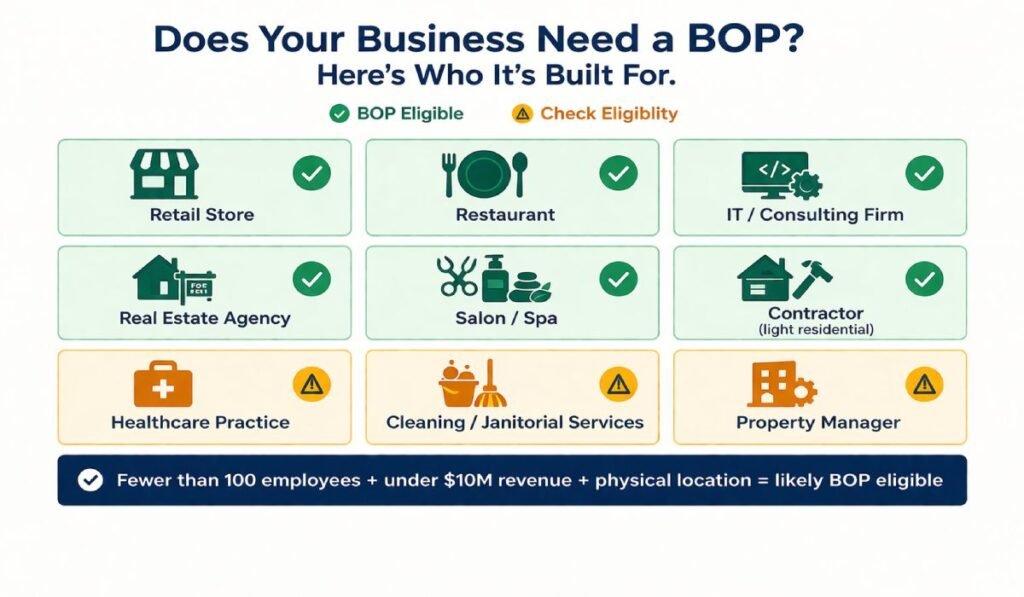

Who Needs a Business Owners Policy?

A BOP is specifically designed for small to mid-size businesses that meet certain eligibility criteria. Most carriers target businesses with:

- Fewer than 100 employees (some carriers extend to 500)

- Annual revenue under $5 million to $10 million (carrier-specific thresholds)

- A defined physical business location — office, retail, warehouse, restaurant, or studio

- Standard commercial risk profiles — not construction, auto dealers, bars, or other excluded classes

The types of businesses that benefit most from a BOP include:

- Retail stores: Customer-facing operations with physical inventory and high foot-traffic slip-and-fall exposure exactly the risk profile BOPs are designed for

- Restaurants and food service: Kitchen fire and business interruption risk make BI/EE coverage essential; GL covers food-borne illness and customer injury claims

- Professional services (accountants, consultants, IT firms): Office-based operations with valuable equipment; low liability risk but significant property and income exposure if operations are disrupted

- Medical and wellness practices: Office property, equipment, and patient-facing liability a strong BOP fit with E&O purchased separately

- Real estate agencies and brokers: Office property, advertising injury risk (personal & advertising injury coverage in GL), and client-facing liability

- Contractors (some): Light residential contractors may qualify for BOP; heavy construction or specialty trades typically require standalone GL + property due to risk complexity

- Salons, spas, and beauty services: Customer-facing operations, valuable equipment, and product liability exposure — well-suited to BOP’s bundled structure

Businesses That Typically Cannot Get a BOP

Some business types exceed BOP eligibility thresholds and require standalone commercial policies or specialty coverage programs. Common BOP-ineligible categories include: auto repair and dealers, bars and nightclubs, financial institutions, adult entertainment, healthcare facilities with high-acuity risk, and most businesses with more than 100 employees or $10M+ in revenue. An independent advisor can quickly confirm eligibility and recommend the appropriate alternative structure.

How Much Does a Business Owners Policy Cost in 2026?

BOP pricing varies widely by industry, location, business size, property value, and claims history. Here is the definitive cost reference for 2026, drawn from Insureon, MoneyGeek, and Progressive Commercial data:

National averages: The median BOP cost for Insureon’s small business customers is $57/month ($684/year). Progressive Commercial’s new customer average is $118/month ($1,420/year), with median at $67/month — the higher average reflects high-risk industries in their mix. MoneyGeek’s analysis across 79 industries and all 50 states places the average at $147/month ($1,767/year) for a two-person business with $300K revenue. Florida’s state average is $76/month.

Distribution: 42% of small businesses pay under $50/month. 30% pay $50–$100/month. The majority of small businesses find BOP pricing well within their budget — particularly low-risk professional services and consulting operations.

BOP Insurance Cost by Industry — 2026 Reference (Insureon, MoneyGeek, Progressive Data)

| Industry | Avg Monthly | Avg Annual | Primary Risk Driver |

|---|---|---|---|

| IT / Software / Consulting | $25–$60/mo | $300–$720/yr | Remote work, low foot traffic, minimal physical property risk |

| Marketing / Advertising Agencies | ~$56/mo | $670/yr avg | Moderate — creative IP exposure, client work, office property |

| Retail Stores | $85–$110/mo | $1,020–$1,320/yr | Customer foot traffic, inventory theft, slip-and-fall risk |

| Restaurants / Food & Beverage | $100–$148/mo | $1,200–$1,770/yr avg | High kitchen fire + BI risk, food liability, high-traffic exposure |

| Building Design / Architecture | ~$54/mo | $648/yr avg | Professional work, moderate property; E&O needed separately |

| General Contractors | ~$98/mo | $1,173/yr avg | Physical job site risk, property damage, product/completed ops |

| Real Estate | $70–$90/mo | $840–$1,080/yr | Property management, tenant exposure, advertising injury risk |

| Pressure Washing / High-Risk Trades | $500–$1,346/mo | Up to $16,158/yr | Highest-risk category — property damage + injury frequency |

How to Lower Your BOP Premium

- Bundle additional coverages: Adding workers’ comp, commercial auto, or professional liability to the same carrier can yield 10–15% multi-policy discounts

- Raise your deductible: A higher property deductible reduces your premium ensure your cash reserves can support the higher out-of-pocket at claim time

- Pay annually: Paying your full annual premium upfront typically saves 5–10% over monthly installment pricing

- Implement documented safety programs: Slip-and-fall prevention protocols, fire suppression systems, alarm monitoring, and security cameras all signal lower risk to underwriters

- Work with an independent advisor: Independent brokers access multiple BOP carriers The Hartford, Chubb, Ergo Next (formerly Next Insurance), Hiscox, Progressive, Travelers, and others — to match your business profile to the carrier with the most competitive pricing for your industry and location

BOP vs. General Liability Alone: When Is a BOP the Right Choice?

Many first-time business insurance buyers start by asking whether they need general liability or a BOP treating them as alternatives. They are not. A BOP includes GL as one of its three components. The real question is whether you need GL alone or GL bundled with property and business income coverage

The answer depends on whether your business has business property at risk. A solo freelance consultant working from a home office with no equipment, no physical location, and no inventory may only need standalone GL — there is nothing to insure under property coverage. But the moment your business has an office, a retail space, a restaurant, owned equipment, inventory, signage, or leasehold improvements a BOP is almost always the more cost-effective and comprehensive choice.

BOP vs. Standalone GL + Property — When Each Makes Sense

| Factor | BOP (Bundled Policy) | Standalone GL + Property |

|---|---|---|

| Coverage structure | One bundled policy — GL + Property + BI/EE in a single contract with one renewal date | Multiple separate policies — each with its own insurer, renewal, premium, and limits |

| Cost | Up to 20% less than buying GL + Property separately (Insureon/Embroker 2026 data) | Full retail pricing on each standalone policy; no bundling discount |

| Best for | Small-to-mid businesses with a physical location, customer-facing operations, business property, and standard risk profile | High-risk businesses, specialized industries, or large businesses whose risk profile exceeds BOP eligibility thresholds |

| Revenue eligibility | Most BOPs are designed for businesses under $5M–$10M annual revenue; carrier-specific | No revenue cap — standalone policies available at any business size |

| Flexibility | Core bundle is fixed; customizable via endorsements (cyber, equipment breakdown, EPLI, etc.) | Fully customizable — each policy can be tailored independently |

| Industries NOT eligible for BOP | Contractors (some), auto dealers, bars, adult entertainment, financial institutions, healthcare (some) | All industries can access standalone GL and property policies |

| Claims handling | One insurer for GL and property claims — reduced complexity, faster coordination | Claims routed to separate insurers — possible coordination issues when a single event triggers multiple policies |

Customizing Your BOP: Common Endorsements for Small Businesses

A standard BOP is the foundation most small businesses expand it with endorsements that address risks specific to their industry or operations. The most commonly added BOP endorsements in 2026:

- Cyber liability / data breach: Covers data breach notification costs, ransomware demands, business interruption from cyber events, and regulatory fines. Essential for any business that stores customer data or relies on digital systems — and the single most important gap in a standard BOP for the majority of small businesses in 2026

- Equipment breakdown: Covers sudden and accidental breakdown of boilers, HVAC systems, electrical systems, refrigeration units, and production equipment. Standard BOP property coverage excludes mechanical failure — this endorsement fills that gap

- Employment practices liability (EPLI): Covers wrongful termination, discrimination, harassment, and wage claims brought by employees. As small businesses hire, EPLI protection becomes increasingly important

- Commercial umbrella: Extends your BOP’s GL limits by $1M, $2M, or more above the primary policy limit. Cost-effective way to access higher total liability protection without repricing the base policy

- Hired and non-owned auto: Covers liability when employees use personal vehicles for business purposes. See our HNOA coverage guide for details

- Spoilage / food contamination: For restaurants and food-service businesses — covers spoilage of perishable goods after a covered property event such as a refrigeration breakdown or power outage

Explore the full range of customization options on our BOP optional endorsements page.

Which Insurers Offer the Best Business Owners Policy in 2026?

The BOP market is competitive and well-developed the following carriers are consistently recognized for small business BOP products in 2026. Independent advisors who access multiple carriers can match your business profile to the insurer pricing your industry most favorably:

- The Hartford: Long-established BOP specialist with deep industry vertical expertise; strong claims reputation; customizable with data breach and off-premises utility endorsements

- Chubb: Preferred for businesses seeking higher limits; online BOP available for businesses under $2M revenue; strong endorsement menu

- Ergo Next (formerly Next Insurance): Fully digital BOP platform; competitive for low-to-moderate risk businesses; instant digital COI issuance; acquired by Ergo (global insurer) in 2025

- Hiscox: Strong for professional services and knowledge-based businesses; available in 43 states + D.C.; competitive pricing for consultants, agencies, and tech firms

- Progressive Commercial: Broad industry appetite; strong for contractors and trades; median new customer premium $67/month in 2024 (the most recent reported figure)

- Travelers, Nationwide, CNA: Mid-market BOP carriers with strong industry-specific programs and broader property coverage options for businesses with more complex risk profiles

Working with an independent commercial insurance advisor — rather than purchasing directly from a single carrier gives you access to all of these markets simultaneously, enabling genuine price and coverage comparison for your specific business profile. Casey Insurance Companies accesses all major BOP carriers and dozens of specialty markets to find the most competitive coverage for your business.

Frequently Asked Questions: Business Owners Policy (BOP)

A BOP covers three core risks in one bundled policy: general liability (third-party bodily injury, property damage, and advertising injury claims), commercial property (your building, equipment, inventory, and business personal property), and business income / extra expense (lost revenue and ongoing expenses while your business is closed after a covered property loss).

A BOP is designed for small to mid-size businesses, generally those with fewer than 100 employees, annual revenue under $5M–$10M (carrier-specific), a defined physical location, and a standard commercial risk profile. Ineligible business types typically include auto dealers, bars and nightclubs, financial institutions, adult entertainment businesses, and some heavy construction or healthcare operations.

National averages range from $57/month (Insureon) to $147/month (MoneyGeek) depending on the industry mix and business profile studied. Progressive Commercial reports a new customer median of $67/month and average of $118/month. Florida businesses average $76/month (Insureon). 42% of small businesses pay under $50/month. Cost is driven primarily by industry risk profile, property value, location, number of employees, claims history, and coverage limits. Low-risk industries (IT, consulting, design) typically pay $25–$60/month; high-risk trades can reach $500–$1,346/month.

Yes — the business income and extra expense (BI/EE) component of a BOP covers lost revenue and continuing operating expenses when your business must close due to a covered property loss (fire, theft, vandalism, wind damage, etc.). Important Florida exception: standard BOP property coverage — and therefore standard BI/EE coverage typically excludes flood damage. In Florida, where storm surge and flooding are primary commercial property risks, a separate flood insurance policy is essential. Without it, a hurricane-related flood that forces your business to close for weeks would not trigger BI/EE coverage.

One Policy. Three Coverages. The Most Efficient Way to Protect Your Business.

A Business Owners Policy is the cornerstone of a sound small business insurance program. It is not the only coverage most businesses need but it is almost always where a complete commercial insurance program starts. In 2026, with commercial property claims rising and business interruption events increasingly common, the question for most small business owners is not whether to have a BOP, but how to build the right one for their specific operations. Our commercial insurance advisors help Florida and nationwide small businesses design BOP programs that start with the right core bundle and extend with the endorsements your industry actually requires at the most competitive pricing across all major carriers. Explore our Business Owners Policy coverage and contact us for a multi-carrier BOP quote today.