A contractor drives his work truck to a job site. An employee makes a delivery run in the company van. A consultant uses her personal car to visit a client across town. In each of these scenarios, if an accident occurs and the vehicle is covered only by a personal auto insurance policy, there is a very strong chance the insurer will deny the claim entirely

This is the central, non-negotiable difference between commercial auto insurance and personal auto insurance and it’s one that costs thousands of business owners tens of thousands of dollars every year. Personal auto policies contain an explicit business use exclusion. The moment your vehicle is being used for business purposes beyond a standard daily commute your personal policy may void coverage for that trip.

In 2026, as more businesses deploy vehicles, rely on employee drivers, and use delivery and field service models, understanding exactly when commercial auto is required, what it costs, and how it compares to personal coverage is not a theoretical insurance question it’s a legal and financial protection imperative.

The $0 Claim Risk:

Personal auto insurance policies almost universally exclude coverage for vehicles used for business purposes. A denied claim after a business-use accident leaves you personally liable for vehicle damage, the other party’s injuries, property damage, and legal fees all out of pocket.

Commercial Auto vs. Personal Auto Insurance: Complete Comparison

Before going deeper into each scenario, here is the definitive side-by-side breakdown of how these two policy types compare across every dimension that matters to a business owner:

Commercial Auto vs. Personal Auto Insurance — 2026 Master Comparison

| Feature | Commercial Auto Insurance | Personal Auto Insurance |

|---|---|---|

| Policy type | Commercial Auto Insurance | Personal Auto Insurance |

| Who it covers | Business entity, any authorized employee driver, named drivers | Named insured and household family members only |

| Vehicle use covered | Business deliveries, client visits, job site travel, commercial hauling | Personal commuting, errands, personal travel NOT business use |

| Liability limits | $500K–$1M+ CSL standard; up to $5M available | $25K–$300K typical; rarely exceeds $500K |

| Who can drive | Any authorized employee operating with business permission | Policyholder and listed household drivers only |

| Business use exclusion | None, built specifically for business operations | Explicit exclusion: business use voids coverage for most claims |

| Hired & non-owned auto | Available as endorsement or standalone | Not available, personal policy cannot extend to hired vehicles |

| Claims handling | Commercial claims team with business expertise | Personal claims department. may not understand business losses |

| Average monthly cost (US) | $147–$293/mo depending on vehicle type and industry | $208/mo full coverage |

| Avg monthly cost (Florida) | $250–$1,370/mo | $311/mo full coverage |

| Annual premium range | $1,762/yr avg to $4,252 full coverage | $2,496/yr national avg; $3,884/yr in Florida |

| Required for business vehicles? | Yes. legally required in all states for business-owned vehicles | Not valid for business-owned vehicles in most states |

Why Personal Auto Insurance Fails for Business Use

Personal auto insurance policies are underwritten based on personal risk how you drive for personal purposes, where you live, your personal driving record, and how many miles you put on your vehicle for non-commercial use. Insurers price those policies with the explicit assumption that the vehicle is not being used to generate income, carry business cargo, or be operated by employees.

The moment a vehicle crosses into business use territory, the risk profile changes fundamentally more miles driven, more driver variability, higher liability exposure, greater cargo value at risk, and more complex claims scenarios. Insurers carve this out through the business use exclusion, which is standard language in virtually every personal auto policy in the U.S.

What Counts as ‘Business Use’?

Most personal auto insurers draw a clear line: commuting to your regular place of work is personal use. Everything beyond that can qualify as business use:

- Driving to client sites, job sites, or customer locations

- Making any form of deliveries products, food, packages including gig economy delivery work

- Transporting tools, equipment, inventory, or business-related cargo

- Driving between multiple work locations or offices in the same day

- Any use where a non-household employee is the driver

- Using a rented or borrowed vehicle for any business purpose this is where hired and non-owned auto insurance (HNOA) becomes essential

The Gig Economy Trap:

Uber, Lyft, DoorDash, Amazon Flex, and similar platform workers are not covered by their personal auto policies while actively working a platform shift. Rideshare and delivery platforms provide some coverage but gap periods exist. Independent gig workers should consult an advisor about commercial or rideshare endorsement options.

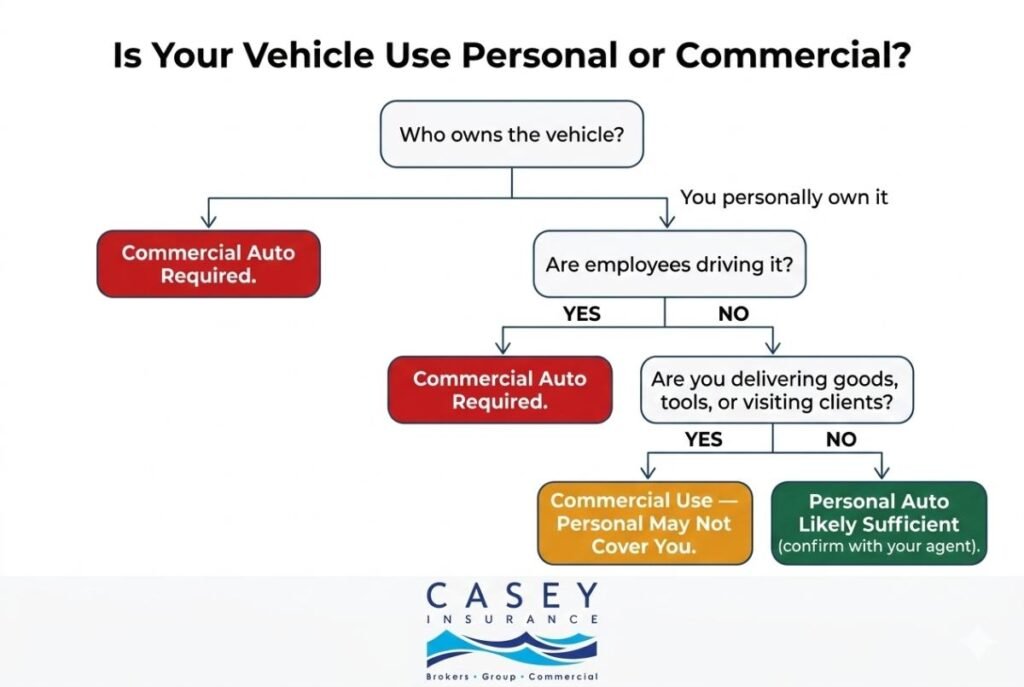

When Does Your Business Legally Require Commercial Auto Insurance?

The requirement for commercial auto insurance isn’t always a gray area. Here is a clear reference table of the scenarios where personal auto is legally or contractually insufficient:

Business Scenarios That Require Commercial Auto Insurance

| Situation | Why Commercial Auto Is Required |

|---|---|

| Vehicle is titled in the business name | Business-owned vehicles cannot be insured under a personal policy regardless of how they’re used |

| Vehicle transports goods, tools, or equipment for business | Tool/cargo transport = commercial use. Personal auto will deny claims. |

| Employees drive the vehicle (even occasionally) | Personal policies cover household members only employee use voids coverage |

| Vehicle is used for deliveries (any kind) | Amazon Flex, food delivery, parts delivery all require commercial or rideshare-specific coverage |

| Vehicle travels to client sites or job locations for work | Client visits and job site travel = business use. Commuting to one fixed office is typically personal use. |

| You’re using a rented or borrowed vehicle for business | Hired and non-owned auto (HNOA) endorsement or standalone policy required not personal auto |

| Your state requires commercial registration for the vehicle | Commercial registration + commercial auto insurance go hand-in-hand in most states |

| A contract or client requires commercial auto proof | COI (Certificate of Insurance) showing commercial auto is required by many GC, government, and large-client contracts |

Key Coverage Differences: What Commercial Auto Offers That Personal Can’t

Beyond the business use exclusion, commercial auto policies are structurally different from personal policies in ways that matter enormously once a claim is filed:

1. Higher Liability Limits

Personal auto policies typically top out at $300,000–$500,000 in combined single limit liability. Commercial auto policies routinely start at $500,000 and extend to $1M, $2M, or more. For businesses operating commercial vehicles in dense areas or transporting valuable cargo, the difference between a $300K personal limit and a $1M commercial limit can be the difference between a covered claim and a personal financial crisis.

2. Any Authorized Driver Coverage

Personal auto policies cover named insured and household family members only. Commercial policies cover any driver authorized to operate the vehicle for business purposes employees, contractors, temporary workers. If an employee borrows the company truck and has an accident, your commercial policy responds. Under a personal policy, that same accident would almost certainly be denied.

3. Hired and Non-Owned Auto (HNOA)

One of the most overlooked coverages in commercial auto hired and non-owned auto insurance covers your business’s liability exposure when employees use their personal vehicles for business tasks or when you rent vehicles for business use. A standard personal policy provides absolutely zero business liability coverage in these situations. HNOA fills that gap without requiring a full fleet policy.

4. Collision and Comprehensive for Commercial Vehicles

Commercial collision and comprehensive coverage works similarly to its personal counterpart but is underwritten for business vehicle use, commercial routes, and the cargo or equipment those vehicles typically carry.

How Much Is Commercial Auto Insurance Per Month in 2026?

This is one of the most searched questions in commercial auto insurance and the answer is: it depends significantly on your industry, vehicle type, number of drivers, and location. But 2026 data gives us solid reference points.

National Averages — 2026

- Insureon average: $147/month ($1,762/year) across all business types and coverage levels

- MoneyGeek / Progressive baseline: $137–$293/month for state minimum coverage, depending on industry profile

- Full coverage (liability + collision + comprehensive): Approximately $354/month ($4,252/year) via Progressive Commercial (MoneyGeek 2026)

- 37% of businesses pay under $100/month: Low-mileage, low-risk operations like financial services ($58/mo via Progressive) represent the lower end of the range

- Commercial auto rate trend: Commercial auto premiums increased an average of 10.4% in 2025 driven by social inflation and rising repair costs.

Florida-Specific Commercial Auto Costs — 2026

Florida consistently ranks among the most expensive states for both personal and commercial auto insurance. In 2026:

- Florida commercial auto range: $250–$1,370/month depending on vehicle type and industry

- Florida average (minimum coverage): $177/month ($2,120/year) via ERGO NEXT, the state’s lowest-cost provider.

- Florida personal auto (full coverage): $311/month average making Florida the third most expensive state nationally.

- Florida weather and litigation factors: Florida’s hurricane exposure, dense traffic, high uninsured driver rate, and active litigation environment all contribute to above-average commercial and personal auto premiums

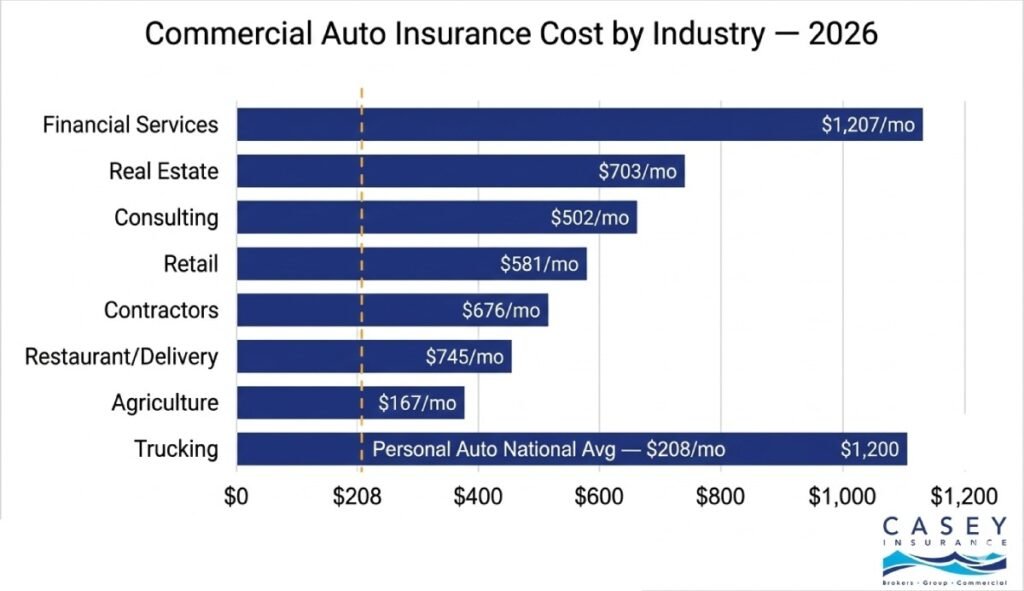

Commercial Auto Insurance Cost by Industry — 2026

| Business / Industry Type | Est. Monthly Premium | Annual Estimate | Primary Cost Driver |

|---|---|---|---|

| Financial Services / Consulting | $58/mo — $696/yr | Varies | Low mileage, client meetings, low cargo risk |

| Retail / Light Delivery | $95–$130/mo | Varies | Regular delivery runs, higher mileage exposure |

| IT / Tech Services | $198/mo avg | Varies | Field service calls, equipment transport |

| Landscaping / Lawn Care | $215/mo avg | Varies | Tool/equipment hauling, job site driving |

| General Contractors | $215–$260/mo | Varies | Job site risk, heavy tool transport, multiple drivers |

| Food Trucks / Catering | $250/mo avg | Varies | Constant road use, vandalism exposure, urban routes |

| Delivery Services | $253/mo avg | Varies | Highest mileage, theft risk, time-pressure driving |

| Trucking / Heavy Commercial | $1,125+/mo | Varies | Weight, cargo value, long haul, federal regulations |

What Factors Determine Your Commercial Auto Insurance Premium?

Understanding what drives your rate gives you actionable levers to manage it. Here are the primary rating factors for commercial auto in 2026:

- Vehicle type: Sedans and compact SUVs carry significantly lower premiums than box trucks, delivery vans, or heavy commercial vehicles. Vehicle value also directly affects collision and comprehensive premiums.

- Business use and mileage: High-mileage operations (delivery, trucking, food service) generate higher premiums. Low-mileage business use (client meetings, occasional site visits) generally costs less than average.

- Number of vehicles: Fleet policies for 5+ vehicles typically unlock 15–25% per-vehicle discounts. More vehicles also spread risk across a larger pool.

- Driver records: Commercial insurers scrutinize every driver’s motor vehicle record (MVR). A single at-fault accident or DUI on a driver’s record can add $500+ annually to that vehicle’s premium.

- Coverage limits and deductibles: Higher liability limits increase premiums proportionally. Higher deductibles reduce premiums but must be balanced against your ability to self-fund a claim.

- Location: State, city, and zip code affect rates based on local traffic density, weather risk, theft rates, and claims environment. Florida, Louisiana, and Nevada are consistently the most expensive states for auto insurance in 2026.

- Telematics and dashcams: GPS tracking and dashcam installation can reduce premiums by 10–25% through demonstrated safe driving. Progressive’s Snapshot ProView, for example, saves fleet operators 5% just for enrollment, with additional discounts for safe driving data.

- Claims history: Commercial auto claims have a direct impact on your renewal rate. Even a single at-fault commercial claim will typically increase your premium for 3–5 years.

Premium Reduction Strategy:

Bundling commercial auto with your general liability or BOP through the same carrier typically yields 10–15% multi-policy discounts. Paying annually instead of monthly also saves 5–13% depending on the carrier. These two moves alone can meaningfully offset premium increases.

Commercial Auto Insurance in Florida: What Business Owners Need to Know

Florida has some of the most complex auto insurance requirements in the country and business owners navigating commercial vehicle coverage need to understand both what the state requires and what the market actually looks like in 2026.

Florida Commercial Auto Minimum Requirements

Florida’s commercial auto requirements vary significantly based on vehicle type and use:

- Standard commercial vehicles: $10,000 in Personal Injury Protection (PIP) and $10,000 in Property Damage Liability (PDL) minimum though these minimums are widely regarded as inadequate for actual business risk exposure

- For-hire passenger vehicles (taxis, rideshare, transportation services): $125,000 per person / $250,000 per incident bodily injury + $50,000 PDL minimum

- Motor carriers operating in interstate commerce: Federal FMCSA requirements apply, with combined single limits starting at $750,000 for many commercial freight categories

- Construction industry vehicles: Additional Florida contractor licensing requirements may mandate specific commercial auto coverage levels

The gap between Florida’s minimum legal requirement and adequate business protection is enormous. The state’s above-average litigation environment, hurricane exposure, and high rate of uninsured drivers make carrying significantly higher commercial auto limits or adding a commercial umbrella a sound financial decision for any Florida business with vehicles on the road.

Our existing blog on commercial vs. personal auto insurance provides additional perspective on why Florida business owners face unique considerations in this space.

Quick Decision Guide: Do You Need Commercial Auto Insurance?

You almost certainly need commercial auto if:

- Your business owns any vehicles cars, trucks, vans, or specialized equipment

- Any employees or contractors drive on behalf of your business

- You or employees make deliveries or pickups of any kind

- You transport tools, equipment, products, or business materials

- You drive to client sites, job sites, or multiple business locations

- You rent vehicles for business purposes

- Your vehicle is titled in your business’s name

You maybe able to use personal auto if:

- You are a solo operator who only drives between your home and one fixed office (standard commute)

- You never transport business goods, equipment, or passengers for compensation

- No employees ever use your vehicle

- Your vehicle is titled personally and exclusively for personal use

Even in the borderline scenarios, an endorsement to your personal policy such as a business use endorsement from some carriers may be available at lower cost than a full commercial policy. An independent insurance advisor can evaluate your specific use case and recommend the right solution.

See our full overview of commercial auto insurance to explore the complete range of coverage options available for your business vehicles.

FAQs About Commercial Auto vs. Personal Auto Insurance

In most cases, no not without significant risk. Personal auto policies contain a business use exclusion that allows the insurer to deny claims when the vehicle was being used for business purposes at the time of an accident. Using your personal vehicle for client visits, deliveries, employee transport, or hauling business equipment creates a gap that your personal policy will not fill.

Nationally, the average commercial auto insurance premium is approximately $147/month ($1,762/year) for all policy types combined. State minimum coverage only starts as low as $137/month. Full coverage (liability + collision + comprehensive) averages around $354/month ($4,252/year).

Not always and the comparison is less straightforward than most people assume. The national average personal auto full coverage premium in 2026 is $208/month ($2,496/year). Low-risk commercial operations like a consultant using a company sedan for client meetings may pay as little as $58–$147/month for commercial auto. High-risk commercial operations like trucking can run $1,125+/month.

Yes commercial auto insurance is widely available for single vehicles. There is no fleet size requirement. A solo contractor with one work truck, a consultant with one company car, or a food truck operator with one vehicle can all purchase a single-vehicle commercial auto policy.

Get the Right Auto Coverage for How Your Business Actually Operates

The distinction between commercial and personal auto insurance isn’t a technicality it’s a financial firewall. In 2026, with commercial auto rates still trending upward and claims costs rising, the worst moment to discover your personal policy doesn’t cover your business driving is after an accident has already happened.

Our commercial insurance advisors help businesses across Florida and nationwide evaluate their auto coverage exposure, structure the right policy for their specific operations, and find the best available rates across multiple carriers. Explore our full commercial auto insurance coverage options including commercial auto liability, collision coverage, comprehensive fleet coverage, and hired and non-owned auto or contact us today for a customized commercial vehicle coverage assessment.

Already researched the personal side of auto coverage? Our blog on collision vs. comprehensive auto insurance and our overview of auto liability insurance how much coverage you need provide useful context for understanding how commercial coverage builds on personal insurance fundamentals.