The moments after a car accident are stressful and confusing. Your heart races, adrenaline surges, and dozens of questions flood your mind. What do I do first? Should I call police? How do I file a claim? What if I say the wrong thing?

Making mistakes during these critical first minutes can result in denied claims, reduced settlements, or personal liability for damages you shouldn’t have to pay. Yet most drivers have never filed an auto insurance claim and don’t know the proper procedures until they desperately need them.

This comprehensive guide walks you through exactly what to do immediately after accidents, how to file claims correctly, what to expect during the process, and how to avoid common mistakes that jeopardize your coverage.

Immediate Actions at the Accident Scene

What you do in the first minutes after an accident significantly impacts your claim outcome.

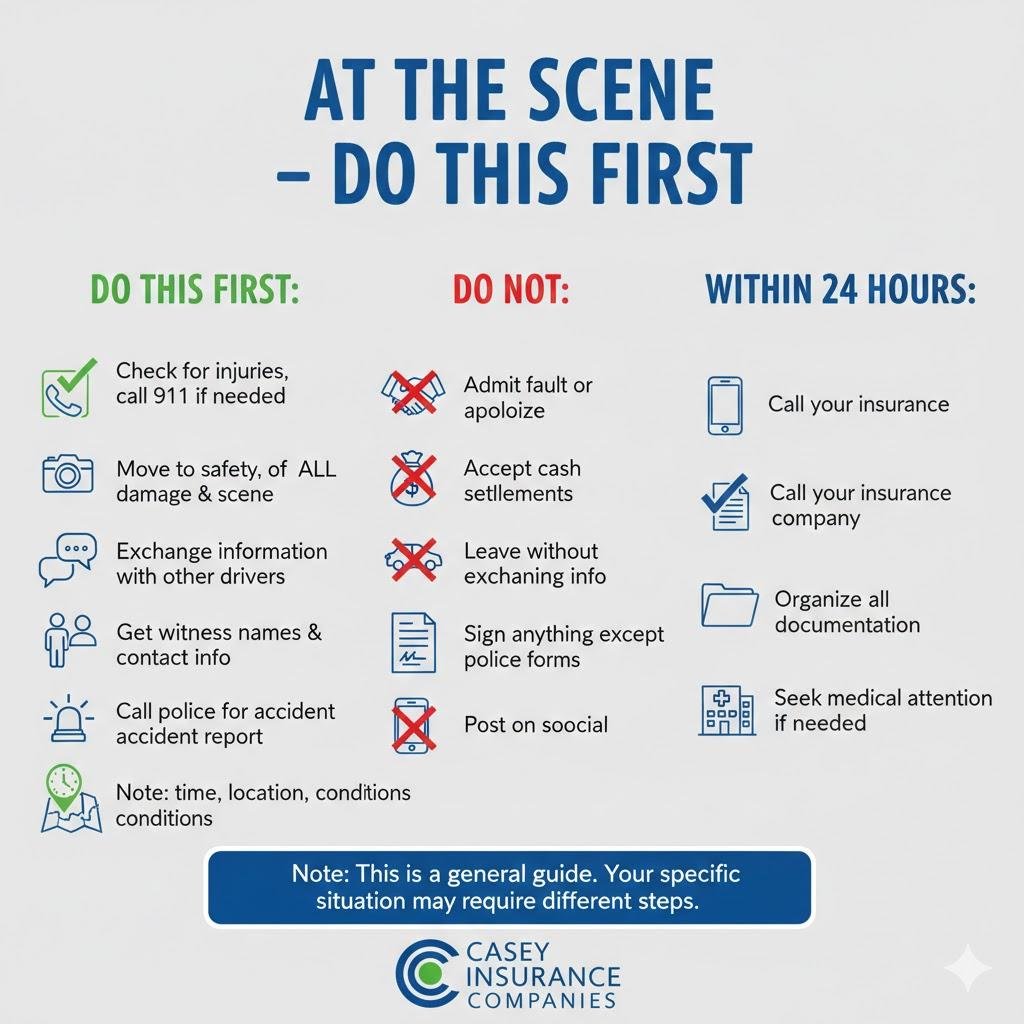

1. Ensure Safety First

Check for Injuries: Assess yourself, passengers, and others involved for injuries requiring immediate medical attention.

Move to Safety: If vehicles are drivable and blocking traffic, move them to the roadside or parking area. Turn on hazard lights.

Call 911: Report accidents involving injuries, significant property damage, disabled vehicles blocking traffic, or hit-and-run situations. Police reports provide crucial documentation for claims.

Don’t Admit Fault: Provide facts to police and other drivers, but avoid saying “I’m sorry” or “it was my fault” even if you believe you caused the accident. Fault determination happens later through investigation.

2. Document Everything Thoroughly

Comprehensive documentation strengthens your claim and prevents disputes.

Take Photos and Videos:

- All vehicle damage from multiple angles

- Overall accident scene showing vehicle positions

- Street signs, traffic signals, road conditions

- Skid marks, debris, or other evidence

- Weather conditions

- Visible injuries (if appropriate)

- License plates of all vehicles involved

Gather Information from Other Drivers:

- Full names and contact information

- Insurance company names and policy numbers

- Driver’s license numbers

- Vehicle make, model, year, and license plate

- Current addresses

Collect Witness Information:

- Names and phone numbers of anyone who saw the accident

- Brief statements about what they witnessed

- Their location when observing the accident

Note Accident Details:

- Date, time, and exact location

- Weather and road conditions

- Traffic signals and signs

- Your recollection of events leading to impact

- Approximate speeds

3. Don’t Discuss Fault or Settlement

Avoid These Mistakes:

- Discussing fault with other drivers

- Accepting cash settlements on the spot

- Signing anything except police reports

- Posting about the accident on social media

- Making recorded statements without your insurer’s guidance

What you say and do at the scene can be used against you later. Stick to facts, exchange information, and save detailed discussions for your insurance company.

When to Contact Your Insurance Company

Timing matters when reporting accidents to your insurer.

Report Immediately If:

You’re At Fault: Always report accidents you caused, regardless of damage severity

There Are Injuries: Any injuries to anyone require immediate reporting

Significant Damage Occurred: Substantial vehicle or property damage needs prompt reporting

The Other Driver Is Uninsured: You’ll need your uninsured motorist coverage

You’re Uncertain About Fault: Let your insurer investigate rather than assuming responsibility

Hit-and-Run Situations: Report immediately delays complicate claims

Police Were Involved: Accidents requiring police reports should be reported to insurers

Can You Wait to Report?

Minor Accidents Where:

- You weren’t at fault

- No injuries occurred

- Damage is minimal

- The other driver has insurance and accepts responsibility

- You’re confident their insurance will cover everything

Even in these situations, report within 24-72 hours. Most policies require “prompt” notification delays can jeopardize coverage.

How to File an Auto Insurance Claim?

Follow this process to file claims correctly.

1: Contact Your Insurance Company

Call Your Agent or Insurer’s Claims Hotline: Most insurers offer 24/7 claims reporting.

Provide Basic Information:

- Your policy number

- Accident date, time, and location

- Brief description of what happened

- Contact information for other drivers

- Police report number (if applicable)

- Extent of injuries and damage

Ask About Next Steps: Understand what your insurer needs from you and their claims timeline.

2: Submit Required Documentation

Your insurer will request:

Written Statement: Detailed account of the accident from your perspective

Photos and Videos: All documentation you collected at the scene

Police Report: Obtain a copy and provide it to your insurer

Repair Estimates: Get estimates from approved or recommended repair shops

Medical Records: If claiming injuries, provide medical documentation and bills

Witness Statements: Formal statements from witnesses supporting your account

Lost Wage Documentation: If claiming income loss, provide employment verification and pay stubs

3: Vehicle Inspection and Damage Assessment

Adjuster Inspection: Your insurer sends an adjuster to assess damage and estimate repair costs.

Approved Repair Facilities: Many insurers have networks of approved shops. Using them often streamlines the process and may include guarantees.

Supplement Estimates: If additional damage is discovered during repairs, shops submit supplemental estimates for approval.

4: Claim Decision and Settlement

Claim Approval: If your claim is approved, your insurer authorizes repairs or issues settlement payment.

Deductible Payment: You pay your collision or comprehensive deductible directly to the repair shop.

Total Loss Determination: If repair costs exceed 75-80% of vehicle value, insurers declare total loss and pay actual cash value minus your deductible.

Settlement Check: For total loss claims, you receive payment within days after settling agreed value and signing title transfer.

How Long Does an Insurance Claim Take?

Claim timelines vary based on complexity and cooperation.

Simple Claims (No Injuries)

Minor Damage, Clear Fault:

- Initial contact to adjuster assignment: 1-3 days

- Vehicle inspection: 2-5 days

- Repair authorization: 1-3 days

- Repair completion: 3-10 days

- Total: 1-3 weeks

Complex Claims (Injuries, Disputed Fault)

Serious Damage or Injury Claims:

- Investigation period: 2-6 weeks

- Medical treatment completion: Months to years

- Negotiation period: 2-12 weeks

- Total: Several months to 2+ years for serious injury claims

Factors Affecting Timeline

Delays Occur When:

- Fault is disputed

- Injuries require ongoing treatment

- Multiple parties are involved

- You’re slow providing documentation

- Repair parts aren’t readily available

- Total loss negotiations drag out

Speed Up Claims By:

- Responding promptly to all requests

- Providing complete documentation immediately

- Cooperating fully with adjusters

- Using approved repair facilities

- Maintaining regular communication

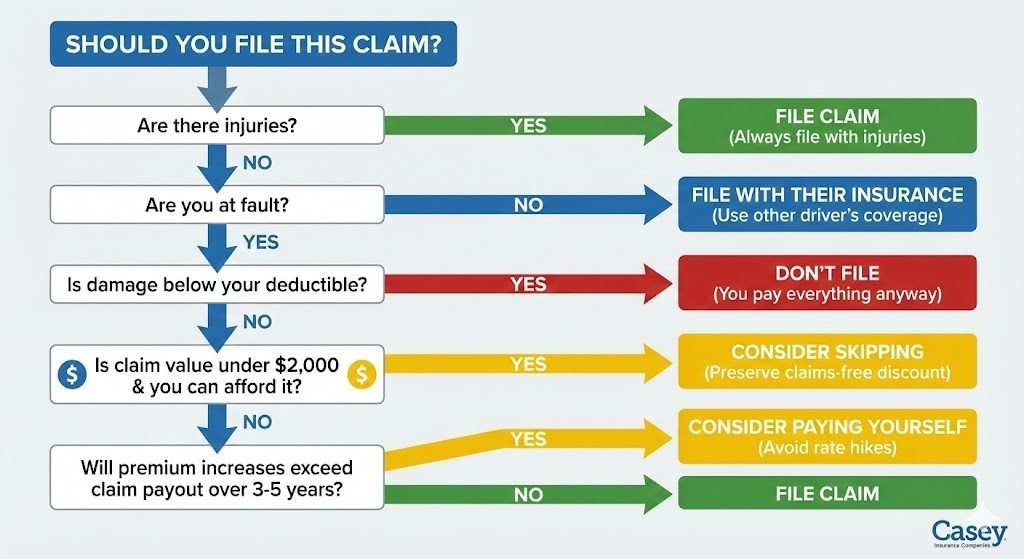

When NOT to File an Auto Insurance Claim

Not every accident warrants filing claims. Consider these factors.

Skip Filing Claims If:

Damage Is Below Your Deductible: If repairs cost $800 but your deductible is $1,000, filing gains nothing and creates a claim record.

Damage Barely Exceeds Deductible: Repairs costing $1,200 with $1,000 deductible nets $200 but may increase future premiums more than $200 over several years.

You Can Afford Repairs Out-of-Pocket: For minor damage under $2,000-$3,000 that you can pay yourself, avoiding claims preserves claims-free discounts.

You Weren’t At Fault and Other Driver Has Insurance: Let the at-fault driver’s liability coverage handle everything no need to involve your insurance.

The Rate Increase Consideration

Filing claims especially at-fault claims typically increases premiums at renewal:

- At-fault collision claims: 20-40% increase for 3-5 years

- Comprehensive claims: 5-15% increase (less impact since not your fault)

- Multiple claims: 30-50%+ increases

Calculate whether claim payouts exceed premium increases over time. Sometimes paying yourself saves money long-term.

What to Do When Insurance Denies Your Claim?

Claim denials are frustrating but not always final.

Common Denial Reasons

Policy Exclusions: Damage from excluded perils or situations

Coverage Lapse: Policy wasn’t active when accident occurred

Late Reporting: Failure to report accidents within required timeframes

Fraud Suspicion: Insurers suspect false or exaggerated claims

Material Misrepresentation: You provided false information on your application

Not Covered Activity: Commercial use on personal policy, racing, intentional acts

Steps to Challenge Denials

1. Request Written Explanation: Insurers must provide specific denial reasons in writing.

2. Review Your Policy: Confirm the denial reason is legitimate based on your policy language.

3. Gather Supporting Evidence: Collect additional documentation supporting your position.

4. File a Formal Appeal: Submit written appeals with new evidence to your insurer’s appeals department.

5. Contact Your State Insurance Department: File complaints with state regulators if you believe denials are unjustified.

6. Consult an Attorney: For significant claims, attorneys specializing in insurance disputes may help.

7. Consider Mediation or Arbitration: Some policies include dispute resolution clauses offering alternatives to lawsuits.

How Long Does an Insurance Claim Stay Open?

Claim status and duration depend on claim type and complexity.

Claim Remains “Open” Until:

Property Damage Claims: Repairs are completed and paid, or total loss is settled—typically 2-8 weeks.

Injury Claims: All medical treatment is finished and settlements are reached—can take months to years.

Ongoing Negotiations: Claims remain open during settlement discussions.

Litigation: Lawsuits keep claims open until court resolution—potentially years.

Claims on Your Record

Even after closing, claims remain on your insurance record:

- Claims History: 3-5 years typically

- CLUE Reports: Comprehensive Loss Underwriting Exchange tracks claims for 7 years

- Rate Impact: At-fault claims affect rates for 3-5 years

This is why avoiding unnecessary claims is wise they follow you for years.

Tips for Smooth Claims Processing

Be Honest and Accurate: Never exaggerate damage or injuries fraud has serious consequences.

Keep Detailed Records: Maintain files with all correspondence, estimates, receipts, and documentation.

Follow Up Regularly: Don’t wait for insurers to contact you check claim status weekly.

Understand Your Coverage: Know your deductibles, limits, and what’s covered before accidents happen.

Don’t Rush Settlements: Especially with injury claims, ensure all treatment is complete before settling.

Review Repair Work: Inspect vehicles thoroughly before accepting completed repairs.

Get Everything in Writing: Don’t rely on verbal promises request written confirmation of all agreements.

Understanding Claims Impact on Future Rates

Filing claims affects your insurance costs beyond the immediate accident.

Rate Increase Duration

At-Fault Claims: Impact rates for 3-5 years, with the largest increases in years 1-3.

Not-At-Fault Claims: May still slightly increase rates with some insurers, though impact is minimal.

Comprehensive Claims: Less impact than collision since they’re not driving-related.

Claims-Free Discounts

Many insurers reward claims-free history:

- 5-10% discount after 3 claim-free years

- 10-15% discount after 5+ claim-free years

- Diminishing deductibles reducing $100-$250 per claim-free year

Filing claims for minor damage sacrifices these valuable long-term discounts.

Your Path to Successful Claims

Understanding the auto insurance claims process removes uncertainty and stress when accidents occur. Knowing what to do immediately, how to document properly, when to file claims versus paying yourself, and what to expect during processing empowers you to handle accidents confidently.

The key is preparation. Review your coverage now, understand your deductibles and limits, know your insurer’s claims process, and keep important information accessible. When accidents happen, you’ll be ready to respond correctly rather than learning through costly mistakes.

Our auto insurance specialists help clients understand their coverage and guide them through claims processes when accidents occur. We provide comprehensive Auto Insurance including Collision Coverage, Comprehensive Coverage, Liability Coverage, and Uninsured Motorist Protection.

Frequently Asked Questions

If you’re not at fault, file with the other driver’s insurance to avoid impacting your rates and using your deductible. If they’re uninsured or disputes arise, then file with your own insurance using collision or uninsured motorist coverage. However, you’re at fault, you must file through your own collision coverage.

You can choose any licensed repair facility insurers cannot force you to use specific shops. However, using their approved network shops often provides guarantees, streamlines the process, and may include better warranties. Get multiple estimates regardless of which shop you choose.

If you believe the settlement is inadequate, don’t accept it immediately. Gather independent estimates, documentation of all damages, and comparable vehicle values. Submit this evidence requesting reconsideration. For serious disputes, consult an attorney or file complaints with your state insurance department.