Water is one of the most common and expensive causes of home damage, yet it’s also one of the most confusing coverage areas in homeowners insurance. The type of water, where it comes from, and how it entered your home determine whether you’re covered or facing thousands in out-of-pocket costs.

Many homeowners discover coverage gaps only after water disasters strike. Flooded basements, burst pipes, roof leaks, and appliance failures cause billions in damage annually, but not all water damage receives equal treatment from insurance companies.

Understanding exactly what standard homeowners insurance covers regarding water damage and critically, what requires separate flood insurance protects you from devastating financial surprises when water invades your home.

Does Homeowners Insurance Cover Water Damage?

The answer is: sometimes, it depends entirely on the water source and how damage occurred.

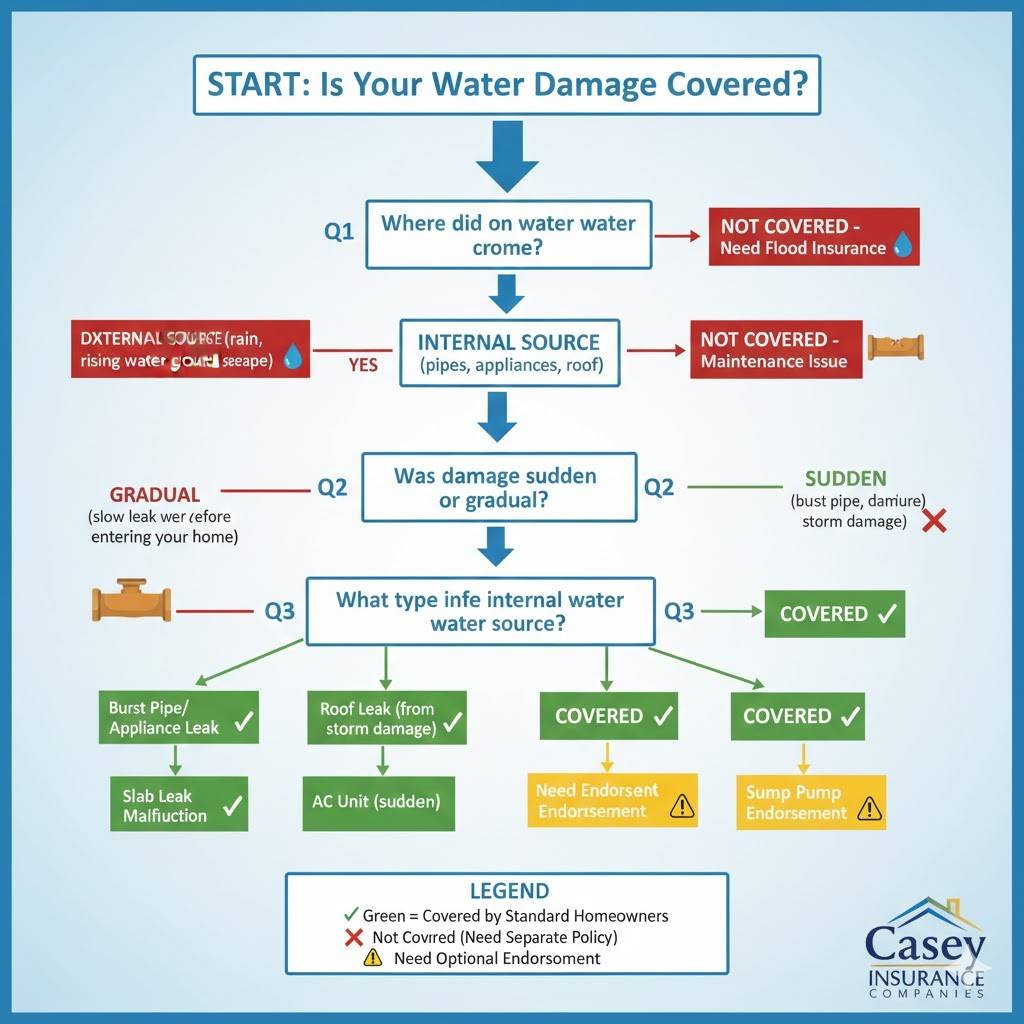

Standard homeowners insurance covers sudden, accidental water damage from internal sources but excludes flooding from external water sources and gradual damage from leaks or seepage.

Water Damage Homeowners Insurance DOES Cover

- Burst Pipes: When pipes suddenly break or burst from freezing, age, or pressure, resulting water damage is covered.

- Appliance Leaks: Washing machines, dishwashers, water heaters, or refrigerators that suddenly malfunction and leak are typically covered.

- Roof Leaks During Storms: Water entering through storm-damaged roofs is covered if the roof was properly maintained.

- Plumbing System Failures: Sudden failures of internal plumbing causing water damage.

- HVAC System Issues: Does homeowners insurance cover water damage from air conditioner? Yes, if AC units malfunction suddenly causing unexpected water damage (like drain pan overflow or sudden failures).

- Slab Leaks: Is a slab leak covered by insurance? Generally yes, if the leak is sudden and accidental. Damage from water escaping under your foundation’s concrete slab is typically covered, though accessing and repairing the pipe itself may have limitations.

- Accidental Overflow: Bathtubs, sinks, or toilets accidentally left running causing overflow damage.

Water Damage Homeowners Insurance DOESN’T Cover

- Flooding from External Sources: Water entering from outside rising rivers, storm surge, heavy rain runoff, or groundwater seepage.

- Basement Flooding from Rain: Does insurance cover basement flooding from rain? No rainwater entering through foundations, windows, or doors is considered flood damage requiring separate coverage.

- Does Homeowners Insurance Cover Water Damage from Rain?: Only if rain enters through storm-damaged roofs or walls. Rain entering through windows, doors, or foundations is excluded.

- Gradual Leaks: Slow leaks developing over time from poor maintenance, deteriorating pipes, or aging systems.

- Sewer Backup: Water backing up through drains and toilets (requires separate sewer backup endorsement).

- Sump Pump Failure: Basement flooding from failed sump pumps (requires separate coverage).

- Ground Water Seepage: Water entering through foundation cracks, basement walls, or below-grade areas.

- Neglect and Maintenance Issues: Water damage resulting from failure to maintain your home properly.

Understanding the Flood Insurance Gap

The distinction between covered “water damage” and excluded “flood damage” confuses many homeowners but it’s critical to understand.

What Qualifies as Flood Damage?

Flooding means water on the ground outside your home that enters your property. This includes:

- Rivers, streams, or lakes overflowing

- Storm surge from hurricanes

- Heavy rain creating surface water runoff

- Melting snow creating standing water

- Groundwater rising and entering basements

- Water accumulating on the ground and entering homes

Key Distinction: If water touched the ground before entering your home, it’s flood damage requiring separate flood insurance.

Why Standard Policies Exclude Floods

Flood risk is:

- Geographically concentrated (coastal areas, floodplains)

- Catastrophic in scope (affecting many homes simultaneously)

- Difficult to price accurately in standard policies

This is why flood coverage requires separate policies through the National Flood Insurance Program (NFIP) or private flood insurers.

Who Needs Flood Insurance?

Required for:

- Homes in high-risk flood zones with mortgages from federally backed lenders

- Properties in Special Flood Hazard Areas (SFHAs)

Strongly Recommended for:

- Properties in moderate-risk flood zones

- Homes near water bodies

- Properties in areas with heavy rainfall or poor drainage

- Basements prone to flooding

Worth Considering for:

- Anyone 25% of flood claims come from low-to-moderate risk areas

- Climate change is increasing flood risk nationwide

Our Flood and Water Coverage specialists help homeowners understand their flood risk and secure appropriate protection.

Water Backup and Sump Pump Coverage

Two common water damage sources require optional endorsements.

Sewer and Drain Backup Coverage

What It Covers: Water backing up through drains, toilets, or sewer lines into your home.

Why It’s Needed: Standard policies exclude this yet it’s increasingly common due to aging infrastructure and heavy storms overwhelming sewer systems.

Coverage Limits: Typically $5,000-$25,000

Cost: $50-$250 annually

Who Needs It: Anyone with basement drains, older sewer connections, or areas prone to sewer system backups.

Sump Pump Failure Coverage

What It Covers: Water damage when sump pumps fail, allowing basement flooding.

Why It’s Needed: Standard policies exclude mechanical failures and their consequences.

Coverage Includes: Damage from pump mechanical failure, power outages affecting pumps, and overflow from pump capacity issues.

Cost: Often included with sewer backup endorsements

Who Needs It: Homes with basements and sump pumps—especially in areas with high water tables or heavy rainfall.

How to Make a Successful Water Leak Insurance Claim

Proper documentation and quick action determine claim success.

Immediate Steps After Water Damage

1. Stop the Water Source: Shut off water mains if pipes burst, turn off appliances, or address the immediate cause if possible.

2. Prevent Further Damage: Make temporary repairs preventing additional damage cover roof holes with tarps, remove standing water with wet vacuums, move belongings to dry areas. Save all receipts.

3. Document Everything Thoroughly:

- Photograph and video all damage from multiple angles

- Document water source and entry points

- Show extent of damage to structures and belongings

- Capture timestamps proving sudden occurrence

4. Contact Your Insurer Immediately: Report claims within 24-72 hours. Don’t wait days or weeks prompt reporting is required.

5. Mitigate Damage: Begin drying and cleanup to prevent mold. Use fans, dehumidifiers, and professional water extraction if needed. Save receipts mitigation costs are typically reimbursed.

6. Don’t Throw Away Damaged Items: Adjusters need to inspect damage before disposal. Keep everything until told otherwise.

Common Claim Mistakes to Avoid

- Delaying Reporting: Late reporting can jeopardize coverage.

- Inadequate Documentation: Poor photos or missing evidence weakens claims.

- Making Permanent Repairs Before Inspection: Wait for adjuster approval except for emergency mitigation.

- Exaggerating Damage: Honesty is crucial fraud has serious consequences.

- Accepting Initial Settlement Without Review: If settlements seem low, get independent estimates and negotiate.

Working with Adjusters

Be Present During Inspection: Point out all damage and ensure nothing is missed.

Provide Complete Documentation: Submit all photos, receipts, and evidence promptly.

Get Multiple Estimates: Independent contractor estimates support your damage claims.

Ask Questions: Understand what’s covered, what’s excluded, and how settlement is calculated.

Follow Up Regularly: Don’t assume silence means progress—check claim status weekly.

Gradual Damage vs. Sudden Damage

This distinction determines coverage for many water claims.

Sudden and Accidental Damage (Covered)

Covered Examples:

- Pipes bursting during freezing weather

- Water heater suddenly failing and flooding basement

- Washing machine hose breaking unexpectedly

- Roof damage from storm allowing immediate water entry

Key: Damage occurs quickly, unexpectedly, and from identifiable single events.

Gradual Damage (Not Covered)

Excluded Examples:

- Slow pipe leaks over weeks/months causing rot

- Persistent roof leaks from deferred maintenance

- Chronic basement seepage from poor drainage

- Ongoing condensation damage from inadequate ventilation

Key: Damage develops over time from neglect, poor maintenance, or ongoing issues you should have addressed.

The Gray Area

Some situations fall between sudden and gradual:

Questionable Scenarios:

- Slow leaks that suddenly worsen

- Pipes deteriorating gradually then bursting

- Chronic minor leaks causing sudden secondary damage

Documentation Matters: Proving sudden occurrence requires evidence. If you discovered damage but can’t prove when it started, insurers may deny claims as gradual damage.

Special Coverage Considerations

Certain water damage situations require specific understanding.

Mold Coverage

Limited Coverage: Most policies cover mold remediation resulting from covered water damage (burst pipes) up to sublimits of $5,000-$25,000.

Excluded: Mold from flooding, gradual leaks, or maintenance neglect isn’t covered.

Mold Endorsements: Available for higher limits if you live in humid climates or have mold concerns.

Frozen Pipe Coverage

Covered If: You maintained heat or drained/shut off water systems when leaving homes vacant.

Excluded If: Homes were vacant without proper winterization or heat maintenance.

Prevention: Keep heat at 55°F minimum, insulate exposed pipes, and drain systems if leaving homes vacant during freezing weather.

Hidden Water Damage

Coverage Depends On: When damage occurred and was discovered.

Scenario: You discover water damage behind walls from old leaks. If gradual, it’s not covered. If from sudden recent events you couldn’t reasonably discover, it may be covered.

Document Discovery: When you find hidden damage, document discovery date immediately to prove it’s recent.

Understanding Your Coverage Limits

Water damage coverage has limits beyond your dwelling coverage amount.

- Dwelling Coverage: Pays to repair water-damaged structures up to your policy limit.

- Personal Property Coverage: Covers water-damaged belongings up to personal property limits.

- Sewer Backup Sublimits: Separate $5,000-$25,000 limits for sewer backup damage.

- Mold Remediation Sublimits: Often $5,000-$25,000 caps on mold removal.

- Service Line Coverage: Optional coverage for repairing underground water/sewer lines (often $10,000 limit).

Review these limits and increase if necessary for adequate protection.

Your Complete Water Damage Protection Strategy

Water damage represents one of homeowners’ biggest financial risks. Complete protection requires understanding both what standard homeowners insurance covers and securing additional coverage for excluded perils.

Essential Coverage Checklist:

- Standard homeowners insurance for sudden internal water damage

- Separate flood insurance if you face any flood risk

- Sewer backup and sump pump failure endorsements

- Adequate dwelling and personal property limits

- Consider service line coverage for underground pipes

Don’t wait until water invades your home to discover coverage gaps. Review your policies now, add necessary endorsements, and ensure you have comprehensive protection against water damage in all its forms.

Our specialists help homeowners build complete water damage protection including Flood Coverage, proper Dwelling Protection, and comprehensive Home Insurance.

Frequently Asked Questions

No basement flooding from rain is considered external flood damage, which standard homeowners policies exclude. You need separate flood insurance through NFIP or private insurers to cover rain-caused basement flooding. However, if you have sewer backup coverage and the flooding results from overwhelmed sewer systems backing up into your basement, that endorsement would provide coverage.

Likely no, gradual leaks over extended periods are excluded as maintenance issues. However, if the slow leak suddenly caused a pipe to burst or resulted in sudden secondary damage (like ceiling collapse), that sudden component might be covered. This is why immediate leak repairs are crucial catching and fixing leaks early prevents both damage and coverage disputes.

Yes, your standard homeowners deductible (typically $500-$5,000) applies to covered water damage claims. However, some policies have separate deductibles for specific endorsements sewer backup coverage might have its own $500-$1,000 deductible. Flood insurance has separate deductibles (typically $1,000-$10,000) independent of your homeowners policy. Always verify which deductible applies when filing water damage claims.