Your home’s physical structure represents your largest investment often worth hundreds of thousands of dollars. Yet many homeowners critically underinsure their dwelling coverage, discovering this costly mistake only after disasters strike when it’s too late to fix.

Understanding dwelling protection coverage and calculating how much you actually need protects you from devastating financial gaps that could leave you unable to fully rebuild after fires, storms, or other covered disasters.

This guide explains exactly what dwelling coverage in home insurance protects, how dwelling amounts are determined, and how to ensure you have adequate dwelling insurance coverage for complete protection.

What Is Dwelling Coverage in Home Insurance?

Dwelling coverage (also called Coverage A or dwelling protection coverage for homeowners insurance) is the foundation of your home insurance policy. It pays to repair or rebuild your home’s physical structure when covered disasters damage or destroy it.

Think of dwelling home insurance as protection for everything that makes up your house itself from foundation to roof and everything structurally in between.

What Dwelling Coverage Protects

Your dwelling amount on home insurance covers:

Main House Structure:

- Walls, floors, and ceilings

- Roof and foundation

- Windows and doors

- Attached structures (attached garage, deck, porch)

Built-In Systems:

- Plumbing and pipes

- Electrical wiring and panels

- Heating and cooling systems (HVAC)

- Built-in appliances

Permanently Attached Features:

- Kitchen cabinets and countertops

- Bathroom fixtures

- Flooring and carpeting

- Built-in shelving

Structural Components:

- Drywall and framing

- Insulation

- Attached light fixtures

- Stairs and railings

Essentially, if it’s permanently attached to your house and would remain if you moved out, dwelling coverage protects it.

What Dwelling Coverage Doesn’t Protect

Understanding exclusions prevents coverage assumptions:

Not Covered by Dwelling Insurance:

- Detached structures (garage, shed)—covered under “Other Structures” coverage

- Personal belongings and furniture—covered under Personal Property Coverage

- Land and landscaping—not insurable

- Liability claims—covered under Liability Coverage

- Flood damage—requires separate flood insurance

- Earthquake damage—requires earthquake endorsements

- Normal wear and tear—maintenance is your responsibility

How Much Dwelling Coverage Do I Need?

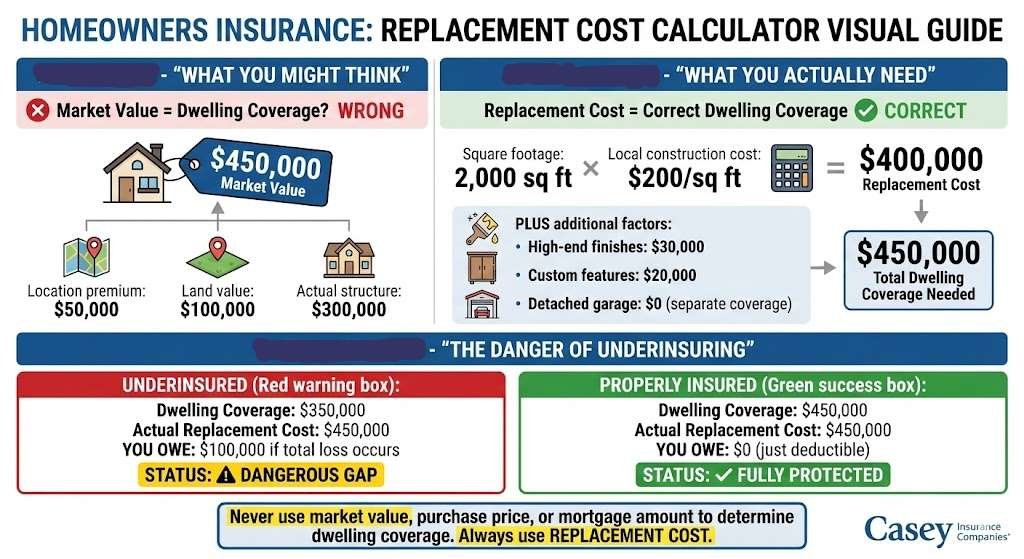

The most critical dwelling coverage question homeowners ask is: “How much do I actually need?” The answer isn’t your home’s market value, purchase price, or mortgage amount it’s your home’s replacement cost.

Replacement Cost vs Market Value

Replacement Cost: Amount needed to rebuild your home from the ground up at current construction prices using similar materials and quality.

Market Value: What buyers would pay for your home, including land value, location desirability, and market conditions.

These numbers differ significantly sometimes by $100,000-$200,000 or more.

Example:

- Your home’s market value: $450,000 (includes $100,000 land value)

- Your home’s replacement cost: $380,000 (actual rebuilding cost)

- Correct dwelling coverage: $380,000

Common Mistake: Insuring for $450,000 (overpaying) or $350,000 (dangerously underinsured).

Factors Affecting Replacement Cost

What you need for dwelling protection coverage depends on:

Construction Quality:

- Custom homes cost more to rebuild than tract homes

- High-end materials (hardwood, granite, custom tile) increase costs

- Architectural details and custom features add expense

Home Size:

- Square footage directly impacts rebuilding costs

- Multi-story homes cost more per square foot than single-story

Local Construction Costs:

- Labor rates vary by region

- Material availability affects pricing

- Permit and building code compliance costs

Special Features:

- Swimming pools and spas

- Finished basements

- High-end kitchens and bathrooms

- Custom woodwork or built-ins

How to Calculate Your Dwelling Amount

1: Professional Replacement Cost Estimator

Most insurance companies use sophisticated calculators considering:

- Your home’s square footage

- Number of stories and rooms

- Construction type and quality

- Age and condition

- Local building costs

This is typically included free when getting quotes.

2: Builder’s Estimate

Contact local builders for estimates to rebuild your home. Get 2-3 estimates and average them. Cost: $300-$500 for formal estimates, but provides accurate replacement cost data.

3: Appraisal

Professional appraisers can provide replacement cost valuations separate from market value assessments. Cost: $300-$600.

4: Rule of Thumb (Less Accurate): Multiply your home’s square footage by local construction costs per square foot ($100-$400+ depending on quality and location). A 2,000 sq ft home in an area with $200/sq ft building costs = $400,000 replacement cost estimate.

The Danger of Underinsuring Your Dwelling

Insufficient dwelling home insurance creates catastrophic financial exposure.

What Happens When You’re Underinsured

Partial Loss Scenario:

- Your home’s replacement cost: $400,000

- Your dwelling coverage: $320,000 (80% of replacement cost)

- Kitchen fire causes $80,000 damage

- Most policies won’t pay full $80,000 they may reduce payment proportionally

Total Loss Scenario:

- Your home’s replacement cost: $400,000

- Your dwelling coverage: $320,000

- House burns down completely

- Insurance pays: $320,000

- Your out-of-pocket: $80,000 to fully rebuild

You can’t rebuild your $400,000 home with $320,000 you face devastating shortfalls when you need coverage most.

The 80% Rule (Coinsurance Penalty)

Many policies include coinsurance clauses requiring you to insure for at least 80% of replacement cost. Falling below this threshold triggers penalties reducing claim payments even for partial losses.

Always insure for 100% of replacement cost the small premium difference isn’t worth the massive exposure.

Replacement Cost vs Actual Cash Value Dwelling Coverage

How your dwelling coverage pays claims makes enormous differences.

Replacement Cost Coverage (Recommended)

Pays: Full cost to rebuild using new materials at current prices no depreciation deduction.

Example: 15-year-old roof damaged by hail. Replacement cost coverage pays for brand-new roof ($18,000). You pay only your deductible.

Benefit: True replacement without paying depreciation gaps.

Cost: Standard in most policies, 10-15% more than actual cash value.

Actual Cash Value Coverage

Pays: Replacement cost minus depreciation based on age and wear.

Example: Same 15-year-old roof. Actual cash value coverage pays depreciated value (~$9,000). You pay deductible plus $9,000 gap.

Drawback: Insufficient for actual rebuilding you cover depreciation personally.

When It’s Used: Only for very old homes or cost-saving measures (not recommended).

Always choose replacement cost dwelling coverage. The small premium difference is worthwhile for complete protection.

Extended and Guaranteed Replacement Cost

For maximum protection, consider enhanced dwelling coverage options.

Extended Replacement Cost

Pays 120-150% of your dwelling coverage limit if rebuilding costs exceed your insured amount.

Example:

- Your dwelling coverage: $400,000

- Extended replacement cost: 125%

- Total available: $500,000

Benefit: Buffer against unexpected cost increases during rebuilding.

Cost: 5-15% premium increase.

Who Needs It: Homeowners in areas with volatile construction costs or unique homes.

Guaranteed Replacement Cost

Pays full rebuilding costs regardless of dwelling coverage limits—no cap.

Benefit: Complete protection even if costs skyrocket.

Requirements:

- Home must be insured at current replacement cost estimate

- Regular policy reviews and updates

- Home under 15-20 years old (varies by insurer)

Availability: Increasingly rare after major disasters demonstrated unpredictable cost spikes.

Cost: 10-20% premium increase when available.

Updating Your Dwelling Coverage

Home values and construction costs change your dwelling amount should too.

When to Review Dwelling Coverage

Annually at Renewal: Construction costs rise 3-8% yearly. Review annually to maintain adequate coverage.

After Renovations: Kitchen remodels, additions, finished basements increase replacement costs. Update dwelling coverage immediately after improvements.

Market Changes: Major construction cost spikes (lumber shortages, labor shortages) may require mid-term increases.

Every 3-5 Years: Get fresh replacement cost estimates ensuring accuracy.

Inflation Guard Endorsements

Many policies include automatic inflation adjustments increasing dwelling coverage 2-4% annually matching construction cost inflation. This helps maintain adequate coverage without manual updates but verify increases match actual local cost trends.

Common Dwelling Coverage Mistakes to Avoid

Mistake 1: Insuring for market value instead of replacement cost

Mistake 2: Forgetting to update coverage after renovations

Mistake 3: Choosing actual cash value to save money

Mistake 4: Assuming your mortgage amount equals proper coverage

Mistake 5: Not understanding coinsurance penalties

Mistake 6: Neglecting to account for special features and high-end finishes

Your Dwelling Protection Foundation

Dwelling coverage is the cornerstone of your home insurance policy. Getting this amount right insuring for full replacement cost with replacement cost coverage ensures you can actually rebuild your home after disasters without devastating out-of-pocket expenses.

Take time now to verify your dwelling amount on home insurance accurately reflects your home’s true replacement cost. The few minutes spent reviewing coverage could save you hundreds of thousands in underinsurance gaps.

Our home insurance specialists help homeowners calculate accurate dwelling protection coverage and ensure their home structures receive proper protection. We provide comprehensive guidance on Dwelling Protection and complete Home Insurance coverage.

Frequently Asked Questions

No dwelling insurance coverage only protects the structure itself, not the land. Land can’t be destroyed by fire, storms, or other covered perils, so it’s not insurable. Your home’s lot retains value even if the structure is destroyed, which is why replacement cost differs from market value (which includes land value).

Not necessarily. Lenders require dwelling home insurance at least equal to your mortgage balance, but this often underinsures your home. If your mortgage is $250,000 but replacement cost is $400,000, the lender’s requirement leaves you $150,000 underinsured. Always insure for full replacement cost, not just the mortgage amount.

Many policies include inflation guard endorsements automatically increasing dwelling amounts 2-4% annually. However, verify this with your insurer and ensure increases match actual local construction cost trends. After major renovations or if construction costs spike dramatically, request additional increases beyond automatic adjustments to maintain adequate protection.