A contractor’s work van is rear-ended by a distracted driver at a job site entrance. A landscaping company’s truck is flooded in a storm surge during hurricane season. A delivery vehicle’s windshield is shattered by hail on I-95. A food truck is stolen from its overnight parking lot. A company car rolls over while avoiding road debris on the Florida Turnpike.

Five scenarios. Five different causes of loss. All of them damaging or destroying a business vehicle. And all of them covered but by two distinct physical damage coverages that most business owners treat as one.

Collision and comprehensive coverage are the components of a commercial auto policy that protect your own business vehicles from damage and loss. They’re what turns a totaled work truck or a stolen delivery van from a catastrophic unplanned capital expense into a manageable insurance claim. In 2026, with motor vehicle repair costs elevated by tariff-driven parts price increases and total loss frequency climbing to 22.6% of all commercial auto claims, understanding exactly what each coverage does and when to carry it, how to deductible it, and what it doesn’t pay for is essential fleet financial management.

This guide explains both coverages in full, compares them head-to-head, addresses the specific considerations Florida fleet operators face, and provides a practical deductible decision framework for businesses with one vehicle or fifty.

2026 Physical Damage Context

Total loss frequency: 22.6% of all commercial auto claims in Q4 2025. Repairable claims volume down 10.4% through August 2025 as owners self-pay smaller repairs. Average repair complexity rising due to ADAS calibration requirements now present in 1-in-3 repairs. Motor vehicle repair costs up 9.7% from tariffs on imported parts. Electric/hybrid vehicle repairs running $1,000+ higher severity than ICE equivalents. Florida: hurricanes and floods are primary comprehensive claim drivers for commercial fleets statewide.

What Is Collision Coverage for Commercial Vehicles?

Commercial auto collision coverage pays to repair or replace your business vehicle when it is damaged in a crash regardless of who caused the accident. It is a first-party coverage, meaning you file a claim with your own insurer rather than against another party’s policy.

Collision coverage applies when your vehicle is damaged by:

- A crash with another vehicle whether you are at fault or the other driver is uninsured

- Impact with a stationary object a telephone pole, guardrail, building, fence, or parking barrier

- A single-vehicle rollover one of the most common commercial vehicle loss scenarios

- Road hazard impact a pothole or road debris that causes vehicle damage

- Crash with an uninsured or underinsured motorist when UM/UIM coverage is insufficient to cover physical damage

What collision does not cover: damage to the other party’s vehicle (that’s your liability property damage coverage), injuries to your driver (that’s medical payments or workers’ comp), cargo or equipment inside your vehicle (inland marine or cargo coverage), or non-collision damage like theft, weather, or fire those require comprehensive.

Your insurer pays up to the actual cash value (ACV) of your vehicle at the time of the loss, minus your chosen deductible. ACV is market value not what you paid for the vehicle or what it would cost to replace it new. For a $65,000 cargo van that has depreciated to $41,000 ACV after three years, a total-loss collision claim pays $41,000 minus your deductible not $65,000.

ACV vs. Replacement Cost — Know the Gap:

Collision and comprehensive both pay actual cash value — not replacement cost. A three-year-old $65,000 work truck that has depreciated to $41,000 will generate a $41,000 claim settlement (minus deductible) if totaled. If you have a loan balance of $52,000 on that truck, you are $11,000 short without gap insurance. For financed or leased commercial vehicles, gap coverage or loan/lease payoff endorsement is essential.

What Is Comprehensive Coverage for Commercial Vehicles?

Comprehensive coverage sometimes called ‘other than collision’ (OTC) — pays to repair or replace your business vehicle when it is damaged by a non-collision event. Like collision, it is a first-party coverage that protects your own asset. Unlike collision, the trigger is an event outside your control: weather, theft, fire, wildlife, or acts of nature.

The most common comprehensive claims for commercial vehicles include:

- Hurricane and tropical storm damage: Wind-driven debris, structural damage from gusts, and water intrusion are major commercial fleet loss events in Florida’s hurricane belt

- Flood damage: Storm surge, flash flooding, and road flooding particularly relevant in Florida’s low-lying coastal and urban areas. Water damage totals vehicles quickly due to electrical system and engine compromise

- Hail damage: Dents, cracked windshields, and ADAS sensor damage from hail events. Hail claims historically approach collision-level repair costs when severe, and ADAS calibration requirements now routinely add $400–$1,500 to hail repair bills

- Vehicle theft: Comprehensive covers the full vehicle theft and non-recovery. A vehicle stolen and not recovered within 30 days is typically treated as a total loss at ACV minus deductible

- Vandalism: Spray paint, broken windows, slashed tires, or deliberate vehicle damage

- Fire: Including arson and electrical fires

- Animal collision: Hitting a deer, hog, or other wildlife a collision with an animal is comprehensive, not collision coverage

- Falling objects: Tree limbs, construction materials, overpass debris

Commercial Vehicle Comprehensive Coverage — What It Covers vs. What It Doesn’t

| ✅ Comprehensive COVERS | ❌ Comprehensive Does NOT Cover |

|---|---|

| Hurricane / tropical storm damage (wind + water) | Collision with another vehicle or stationary object (use collision) |

| Flood damage — storm surge, flash flooding, road flooding | Mechanical breakdown or engine failure |

| Hail damage — dents, broken glass, ADAS sensor damage | Wear and tear, gradual deterioration |

| Vehicle theft — full theft + theft of parts/accessories | Personal belongings inside the vehicle at time of theft |

| Vandalism — keying, broken windows, spray paint | Damage caused by a collision disguised as non-collision |

| Fire damage — including arson and electrical fire | Intentional damage by the vehicle owner |

| Hitting an animal (deer strike, wildlife impact) | Damage to the animal you hit (use liability PD) |

| Falling objects — tree limb, construction debris, overpass damage | Cargo or equipment inside/on the vehicle (use cargo/inland marine) |

| Lightning strike — electrical and structural damage | Coverage above actual cash value — no new replacement value unless you add endorsement |

| Tornado, earthquake, civil disturbance damage | Rental vehicle costs during repair (add rental reimbursement endorsement) |

Collision vs. Comprehensive: Complete Side-by-Side Comparison

Here is the full head-to-head breakdown of how these two physical damage coverages work for commercial vehicles:

Collision vs. Comprehensive Coverage for Commercial Vehicles — 2026 Master Comparison

| Feature | 🔵 Collision Coverage | 🟢 Comprehensive Coverage |

|---|---|---|

| What it covers | Damage to YOUR vehicle caused by a collision — with another vehicle, a stationary object, a guardrail, or a rollover | Damage to YOUR vehicle from non-collision events — weather, theft, fire, vandalism, animals, floods, falling objects |

| Triggered by | At-fault accident, multi-vehicle crash, single-vehicle rollover, hitting a pothole or road hazard | Hurricane / tropical storm, hail, flood, fire, lightning, vehicle theft, vandalism, hitting a deer or animal |

| Who files the claim | You file against your own collision coverage if at-fault or if other driver is uninsured | You file against your own comprehensive policy regardless of fault — it is always a first-party claim |

| Coverage limit | Actual cash value (ACV) of your vehicle at time of loss, minus your deductible | Actual cash value (ACV) of your vehicle at time of loss, minus your deductible |

| Florida total loss threshold | If repair cost ≥ 80% of ACV, insurer may declare vehicle a total loss | Same 80% ACV rule applies. Hail and glass exclusions for salvage title branding only. |

| Premium rate impact | At-fault collision claim: +40–50% premium increase typical for 3–5 years | Comprehensive claim: +3–10% increase, or often no surcharge for first claim |

| Required by lenders? | Yes — any financed or leased commercial vehicle requires collision | Yes — any financed or leased commercial vehicle requires comprehensive |

| Required by state law? | No — optional first-party coverage | No — optional first-party coverage |

| Florida-specific notes | Florida’s high traffic density and uninsured motorist rate (14%+) elevates collision risk for fleet vehicles | Florida’s hurricane/tropical storm exposure and flooding make comprehensive a high-frequency coverage trigger for commercial fleets |

| Deductible options | $500, $1,000, $2,500, $5,000 — higher deductible = lower premium, higher out-of-pocket at claim | Same deductible structure; many insurers offer separate comp and collision deductibles for fleet policies |

Collision and Comprehensive Coverage for Florida Fleet Operations

Florida’s geography, weather patterns, and claims environment create a commercial auto physical damage exposure that is meaningfully different from most other states. Florida fleet operators need to understand these specific dynamics when making collision and comprehensive coverage decisions.

1. Hurricane and Flood Exposure

Florida’s Atlantic and Gulf Coast geography puts virtually every commercial fleet in the direct path of hurricane and tropical storm activity. Comprehensive coverage responds to all storm-related vehicle damage: wind damage, wind-driven debris, storm surge flooding, and rainwater intrusion. In a major hurricane event, fleet damage can be total-loss-level across dozens of vehicles simultaneously a scenario that makes comprehensive not just advisable but operationally essential for any Florida business that relies on its vehicle fleet to generate revenue.

Florida has an 80% total loss threshold if repair costs equal or exceed 80% of a vehicle’s ACV, the insurer may declare it a total loss and pay ACV minus deductible rather than fund repairs. For flood-damaged vehicles in particular, this threshold is often exceeded quickly: water intrusion into electrical systems, engine compartments, and interiors typically generates repair estimates that approach or exceed vehicle value even on relatively new commercial units.

2. Hail and ADAS Calibration Complexity

Florida experiences significant hail events, particularly in central and northern regions during spring storm season. Hail damage that would have generated a straightforward PDR (paintless dent repair) claim five years ago now frequently triggers additional ADAS calibration requirements — because sensors in bumpers, windshields, and rooflines are displaced or damaged by hail impact and require recalibration after every repair in which they are involved.

According to CCC Intelligent Solutions, ADAS calibration is now required on more than one-third of all commercial vehicle repairs in 2025-2026. A hail repair that costs $3,200 in body work may require an additional $800–$1,500 in calibration procedures, increasing the effective claim cost significantly. Comprehensive deductible selection for Florida fleet vehicles should account for this elevated baseline repair cost.

3. Vehicle Theft in Florida’s Commercial Vehicle Market

Florida consistently ranks among the top states nationally for vehicle theft, and commercial vehicles particularly cargo vans, pickup trucks with tools, and trailers are disproportionately targeted due to their cargo and resale value. Comprehensive theft coverage responds when a vehicle is stolen and not recovered: the insurer pays ACV minus deductible, typically processing the total loss within 30 days of the theft report if the vehicle remains unrecovered.

Businesses can reduce comprehensive premiums and theft exposure simultaneously by investing in GPS tracking (which aids recovery and earns underwriting credits), anti-theft ignition immobilizers, and secured overnight parking. These measures are particularly important in high-theft metro areas including Miami-Dade, Broward, Hillsborough, and Orange counties.

Florida Pre-Season Action

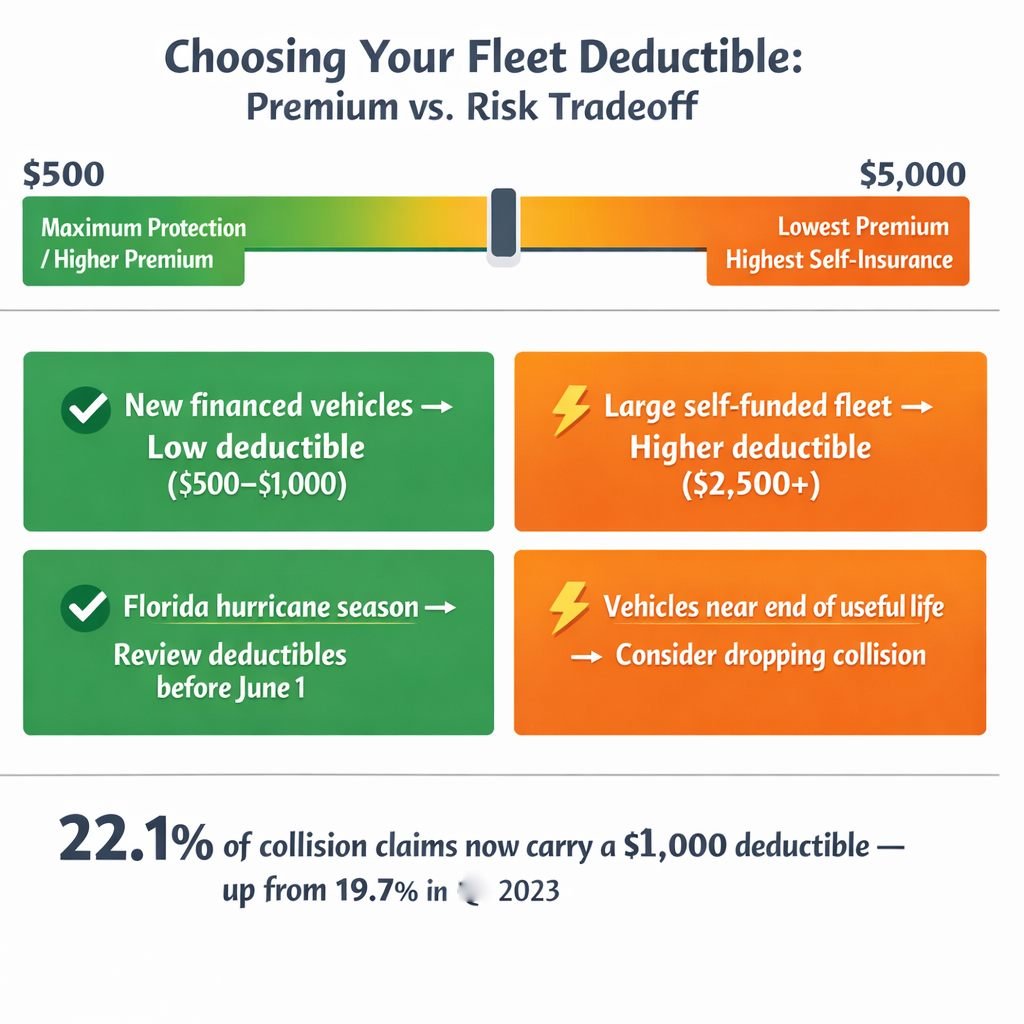

Review comprehensive deductibles before June 1 (official start of hurricane season). If your current deductible is $2,500 or $5,000 and your fleet consists of vehicles with ACV of $30,000–$60,000, confirm you have adequate reserves to fund multiple simultaneous deductibles in a major storm event. Consider reducing deductibles 90 days before hurricane season if reserves are tight.

Choosing the Right Deductible for Your Commercial Vehicle Fleet

Deductible selection is one of the most consequential decisions in commercial auto physical damage coverage and one that most business owners make once at policy inception and never revisit. In 2026, 22.1% of collision claims carry a $1,000 deductible, up from 19.7% in 2023, reflecting a broader trend of fleet operators moving toward higher deductibles to manage premium costs in a rising-rate environment.

The right deductible is not simply the lowest one available. It is the deductible level at which your premium savings justify the additional out-of-pocket cost you would absorb at claim time — balanced against your fleet’s claim frequency, vehicle values, and available cash reserves.

Commercial Fleet Deductible Decision Framework — 2026

| Deductible | Out-of-Pocket at Claim | Premium Level | Best Fit |

|---|---|---|---|

| $500 | Lower | Highest | Best for newer, high-value fleet vehicles where a claim is likely to exceed deductible; also best if cash reserves are limited |

| $1,000 | Moderate | Moderate — most common fleet choice in 2026 (22.1% of claims carry $1K deductible, CCC 2024) | Balance of affordability and protection; good for mid-value work trucks and vans with moderate claim history |

| $2,500 | Significant | Lower | Best for high-volume fleets where small claims are self-insured; reduces premium but requires reserves to fund claims |

| $5,000 | High | Lowest | For large fleets with dedicated risk management, a formal self-insurance program, or vehicles with lower market value |

The 10% Rule for Older Vehicles

A widely used guideline for commercial fleet physical damage coverage: if the annual combined premium for collision and comprehensive exceeds 10% of the vehicle’s current ACV, the coverage may no longer be cost-effective. For a work truck with an ACV of $12,000, if collision + comprehensive costs more than $1,200/year, you are paying insurance premiums close to a meaningful fraction of the vehicle’s value. At that ratio, dropping physical damage coverage and self-insuring the vehicle may make more financial sense provided the vehicle is fully owned (not financed) and you have the reserve to fund replacement.

Important exception

The 10% rule never applies to financed or leased commercial vehicles. Lenders require collision and comprehensive coverage for the life of the loan or lease, regardless of the cost-to-value ratio. Dropping coverage on a financed vehicle violates your loan agreement and can trigger force-placed insurance at rates significantly higher than voluntary market coverage.

When Is Collision and Comprehensive Coverage Required?

Unlike liability coverage, collision and comprehensive are not legally mandated by state law. But they are required in several common business situations:

- Financed commercial vehicles: Any vehicle with an outstanding loan or lease requires both collision and comprehensive coverage as a condition of the financing agreement. The lender is a loss payee on your policy and must be paid before you in a total loss claim.

- Leased fleet vehicles: Leasing contracts universally require full physical damage coverage. The lessor owns the vehicle and will require both collision and comprehensive at specific minimum levels.

- Client or contract requirements: Some commercial clients, government contracts, or project agreements require that vehicles used on their sites carry full physical damage coverage as part of their contractor insurance requirements.

- SBA loans and equipment financing: Small Business Administration loans and equipment financing arrangements typically include a requirement for physical damage coverage on the financed assets.

- High-value fleet vehicles: Operationally, any vehicle whose loss would create a significant unplanned capital expenditure for your business warrants physical damage coverage regardless of financing status.

For businesses with older, fully owned vehicles of low ACV, the decision to carry or drop physical damage coverage can be evaluated using the 10% rule above. For newer vehicles, high-value trucks, or financed equipment, collision and comprehensive are essential components of the full commercial auto package.

Total Loss Claims: How Commercial Vehicle ACV Is Determined

In 2026, 22.6% of commercial auto physical damage claims are declared total losses — a rate that has been climbing as vehicle complexity increases repair costs faster than vehicle values appreciate. Understanding how total loss is determined — and how ACV is calculated — prevents surprises at claim time.

Florida’s 80% Total Loss Threshold

Florida uses a fixed 80% total loss threshold: if the estimated repair cost equals or exceeds 80% of the vehicle’s ACV at the time of loss, the insurer may declare it a total loss and pay ACV minus deductible rather than fund repairs. Unlike states that use a total loss formula (TLF) that factors in salvage value, Florida’s rule is based purely on the repair-cost-to-ACV ratio making it one of the stricter thresholds in the country.

Florida also includes applicable replacement sales tax in total loss ACV settlements a meaningful addition for commercial vehicle replacements that can add $3,000–$6,000 to a settlement on a $50,000–$100,000 commercial vehicle.

Actual Cash Value (ACV) — What It Means for Your Fleet

Your insurer determines ACV by researching comparable vehicles in your area same make, model, year, mileage, and condition. ACV reflects depreciated market value, which means:

- A three-year-old $65,000 work truck may have an ACV of $38,000–$43,000 depending on mileage and condition

- A cargo van with 120,000 miles has significantly lower ACV than the same van at 45,000 miles, regardless of what you paid

- Commercial upfits (specialized equipment installed on a vehicle) may or may not be included in ACV depending on whether they were declared on your policy always list commercial upfits explicitly

- If you disagree with your insurer’s ACV calculation, you have the right to negotiate. Providing documentation of comparable vehicles at higher prices is the most effective negotiation tool. Florida law permits you to dispute ACV through the appraisal process outlined in your policy

Gap Insurance for Commercial Vehicles

When the ACV of your commercial vehicle is less than your outstanding loan balance, gap insurance or a loan/lease payoff endorsement pays the difference between the insurance settlement and what you owe. Without it, a total loss on a financed $75,000 cargo van with an ACV of $55,000 and an outstanding loan of $65,000 leaves you personally responsible for the $10,000 gap.

Gap endorsements are inexpensive relative to the exposure they address typically $50–$200 per vehicle per year and are strongly recommended for any recently financed commercial vehicle in the first three years of a loan term, when loan balance most commonly exceeds depreciated ACV.

Upfit Declaration Reminder

Commercial vehicles with specialized upfits ladder racks, refrigeration units, tool storage systems, mounted equipment — must have those upfits explicitly declared on your commercial auto policy to ensure they are included in ACV calculations at claim time. An undeclared $18,000 refrigeration unit on a cargo van will not appear in an adjuster’s ACV calculation unless it is listed on your policy schedule.

FAQs About Collision and Comprehensive Commercial Vehicle Coverage

Collision coverage pays to repair or replace your business vehicle when it is damaged in a crash — with another vehicle, a stationary object, or in a rollover. Comprehensive coverage pays for non-collision damage: hurricane, flood, hail, vehicle theft, vandalism, fire, animal strikes, and falling objects. Both are first-party coverages that pay based on your vehicle’s actual cash value minus your deductible. The key distinction: collision responds to crashes; comprehensive responds to everything else.

If your commercial vehicles are financed or leased, yes — both are required by your financing agreement. For vehicles you own outright, the decision depends on the vehicle’s current ACV and your financial ability to absorb a loss without insurance. A useful guideline: if the combined annual premium for collision and comprehensive exceeds 10% of the vehicle’s ACV, self-insurance may be worth considering for lower-value units. However, for high-value trucks, specialized vehicles, or fleet units that are operationally critical, carrying both coverages is almost always the right decision — one uninsured total loss can cost more than a decade of premiums.

Florida uses an 80% total loss threshold: if the estimated repair cost equals or exceeds 80% of your vehicle’s actual cash value (ACV) at the time of loss, your insurer may declare it a total loss and pay ACV minus your deductible rather than funding repairs. Florida also includes applicable replacement sales tax in ACV settlements. If you owe more on a loan than the ACV settlement, gap insurance or a loan/lease payoff endorsement covers the difference. You have the right to dispute your insurer’s ACV valuation — provide documentation of comparable vehicles at higher market prices to support your negotiation. Most total loss claims settle within 2–4 weeks of damage assessment.

Yes — hail damage is a covered peril under comprehensive coverage for commercial vehicles. This includes dents to body panels, cracked or shattered windshields and glass, and damage to ADAS sensors mounted in bumpers, mirrors, and windshield areas. In 2026, ADAS calibration requirements are now triggered in more than one-third of commercial vehicle repairs — including many hail repairs — adding $400–$1,500 in calibration costs to otherwise straightforward body work. Florida businesses should note that while hail damage is covered, the hail damage cause is excluded from Florida’s salvage title branding requirements — meaning a hail-totaled vehicle may receive a clean title rather than a salvage designation, preserving resale value.

Protect Every Vehicle in Your Fleet — Before the Next Storm, Accident, or Theft

Collision and comprehensive coverage are the financial backstop between a damaged or stolen business vehicle and a major unplanned capital expenditure. In 2026, with repair costs elevated by tariffs and ADAS complexity, and total loss frequency at its highest level in years, physical damage coverage decisions deserve the same analytical attention as your liability limits

Our commercial insurance advisors help Florida and nationwide fleet operators structure collision and comprehensive programs that are properly deductible for your cash position, accurately schedule your vehicle upfits, and price competitively across multiple commercial carriers. Explore our collision coverage for commercial vehicles and comprehensive coverage for business fleets pages, review our complete commercial auto insurance program, and contact us for a fleet physical damage coverage assessment today.

Also see our guides to commercial auto liability coverage and commercial auto insurance vs. personal auto for the full commercial vehicle insurance picture.