Your home contains thousands of dollars in belongings furniture, electronics, clothing, appliances, jewelry, and countless other possessions accumulated over years. Yet most homeowners significantly underestimate the total value of everything they own until disaster strikes and they must replace it all.

Personal property insurance (Coverage C on homeowners policies) protects your belongings when they’re damaged, destroyed, or stolen. But standard coverage includes sublimits on valuable items that leave many possessions underinsured or completely unprotected.

Understanding what personal property coverage actually protects, how much coverage you need, and when to schedule high-value items prevents devastating financial gaps when you need to replace your belongings.

What Is Personal Property Coverage?

Personal property coverage (Coverage C) protects your belongings inside and outside your home. This insurance for personal property covers items you own not the structure itself (that’s dwelling coverage).

What Does Personal Property Insurance Cover?

Coverage C personal property protects a wide range of belongings:

Furniture and Household Items:

- Sofas, chairs, and tables

- Beds and mattresses

- Lamps and decorative items

- Kitchen appliances and cookware

- Dishes and utensils

Electronics and Technology:

- Televisions and computers

- Tablets and smartphones

- Gaming systems and equipment

- Cameras and photography gear

- Home theater systems

Clothing and Accessories:

- All clothing and shoes

- Handbags and luggage

- Watches and everyday jewelry

- Sunglasses and accessories

Hobby and Recreation Equipment:

- Sports equipment

- Musical instruments

- Exercise equipment

- Tools and workshop items

- Lawn and garden equipment

Items Away from Home:

- Belongings in your car

- Luggage during travel

- College dorm room items

- Storage unit contents

Personal belongings insurance typically covers your possessions anywhere in the world, not just inside your home this worldwide coverage is a valuable benefit many people don’t realize they have.

What Personal Property Coverage Doesn’t Cover (or Limits)

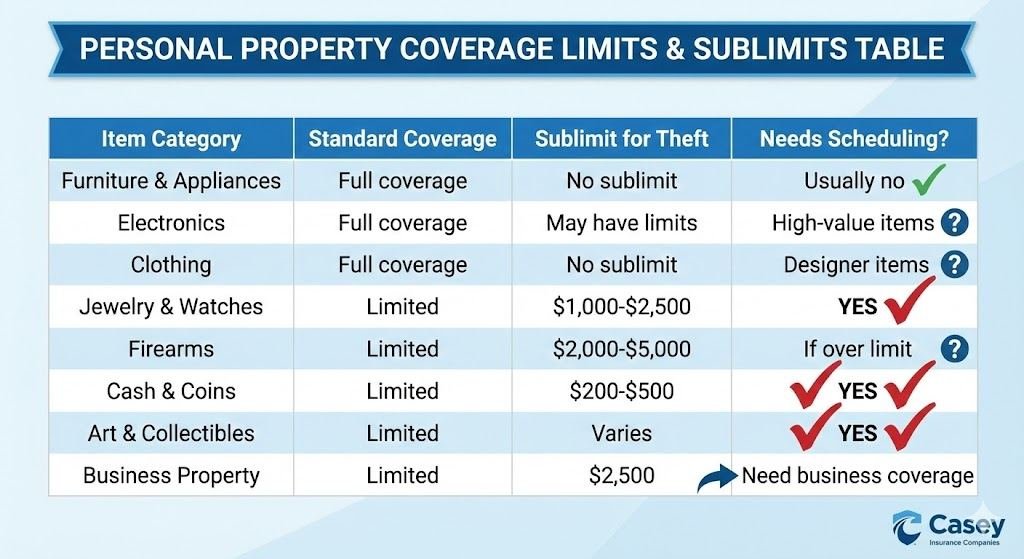

Standard coverage includes significant limitations on certain valuables:

- Jewelry, Watches, and Furs: Typically limited to $1,000-$2,500 total for theft

- Cash and Currency: Usually $200-$500 maximum

- Firearms: Often $2,000-$5,000 limit

- Silverware and Goldware: Limited coverage

- Fine Art and Collectibles: May have sublimits

- Business Property: Typically $2,500 limit or excluded entirely

- Electronics for Business: Limited or excluded

These sublimits mean if you have $15,000 in jewelry and it’s stolen, your standard policy might pay only $1,500 leaving you with $13,500 in uncovered loss.

How Much Personal Property Coverage Do I Need?

Determining adequate coverage requires honest assessment of what you own.

Standard Coverage Amounts

Personal property coverage limits homeowners insurance typically equal 50-70% of your dwelling coverage.

Example Calculations:

- $300,000 dwelling coverage = $150,000-$210,000 personal property coverage

- $500,000 dwelling coverage = $250,000-$350,000 personal property coverage

This standard percentage works for many homeowners, but not all.

When Standard Limits Aren’t Enough

Increase personal property coverage beyond standard percentages if you:

- Own expensive furniture or designer pieces

- Have extensive wardrobes or shoe collections

- Possess significant electronics (home theater, computer equipment)

- Collect art, antiques, or other valuables

- Have substantial hobby equipment (photography, music, sports)

- Work from home with expensive equipment

Creating a Home Inventory

The best way to determine how much personal property coverage you need is creating a detailed inventory:

Inventory Best Practices:

- Room-by-Room Documentation: Walk through every room photographing and listing everything

- Video Walkthrough: Record video showing all belongings, opening closets and drawers

- Keep Receipts: Save purchase receipts for expensive items

- Update Regularly: Add new purchases and remove disposed items

- Store Securely: Keep copies in cloud storage or off-site

Digital Tools: Apps like Sortly, MyStuff2, or Encircle help create organized inventories with photos, values, and receipts.

Most people discover they own far more than expected when completing inventories often $100,000-$300,000+ in possessions.

Replacement Cost vs Actual Cash Value

How your personal belongings insurance pays claims dramatically affects what you receive.

Replacement Cost Coverage (Recommended)

Pays: Full cost to replace items with new equivalents at current prices no depreciation.

Example: Your 5-year-old $1,500 laptop is stolen. Replacement cost coverage pays for a comparable new laptop (~$1,500). You pay only your deductible.

Benefits:

- True replacement without out-of-pocket depreciation costs

- Ability to actually replace possessions

- Peace of mind knowing full value protection

Cost: Typically 10-20% higher premiums than actual cash value

Actual Cash Value Coverage

Pays: Replacement cost minus depreciation based on age and condition.

Example: Same stolen 5-year-old laptop. Actual cash value coverage pays depreciated value (~$500-$700). You pay deductible plus $800-$1,000 to replace it.

Drawbacks:

- Insufficient for actual replacement

- Out-of-pocket costs for depreciation

- Can’t truly replace many items

Recommendation: Always choose replacement cost coverage for personal property. The modest premium increase is worthwhile for complete protection.

What Causes Coverage C to Pay Claims?

Personal property coverage protects against the same perils as your dwelling:

Covered Perils:

- Fire and smoke damage

- Theft and burglary

- Vandalism and malicious mischief

- Windstorm and hail

- Lightning strikes

- Water damage from burst pipes

- Falling objects

- Weight of ice, snow, or sleet

Not Covered:

- Floods (requires flood insurance)

- Earthquakes (requires earthquake coverage)

- Normal wear and tear

- Pest damage (termites, rodents)

- Intentional damage

Special Limits and Considerations

Understanding sublimits prevents claim surprises.

Common Personal Property Sublimits

Standard Policy Sublimits:

- Jewelry, watches, furs: $1,000-$2,500

- Firearms: $2,000-$5,000

- Silverware, goldware: $2,500

- Cash, coins, precious metals: $200-$500

- Securities, stamps, collectibles: $1,000-$5,000

- Watercraft and trailers: $1,000-$1,500

- Business property: $2,500

Example Problem: You have $8,000 in firearms. Without scheduling, theft coverage maxes at $2,500 you lose $5,500 in uncovered value.

Items Typically Excluded or Limited

Business Equipment: Computers, supplies, and inventory for home businesses require business insurance or endorsements.

Motor Vehicles: Cars, motorcycles, ATVs require separate auto/vehicle insurance.

Credit Cards: Most policies cover $500-$1,000 in unauthorized charges.

Electronic Data: Stored data and software often have limited coverage back up important files.

Off-Premises Coverage

Coverage C personal property protects your belongings worldwide, not just at home.

What Off-Premises Coverage Includes

Protected Situations:

- Hotel room theft during vacation

- Belongings stolen from your car

- Items in storage units

- College student dorm rooms

- Luggage lost during travel

- Equipment stolen at gym or office

Typical Limit: 10% of your total personal property coverage applies off-premises.

Example: If you have $200,000 personal property coverage, $20,000 applies to off-premises locations.

College Student Coverage

Students living away at college remain covered under parents’ homeowners policies, but verify:

- Coverage applies to dorm rooms and off-campus apartments

- Limits are adequate for electronics, clothing, and furnishings students have

- High-value items (laptops, bikes, instruments) are scheduled if needed

Some insurers require separate renters policies for off-campus housing.

Filing Personal Property Claims

Proper documentation and procedures ensure successful claims.

Essential Claim Documentation

What You Need:

- Home inventory with photos/videos showing items

- Purchase receipts or proof of value

- Police reports for theft claims

- Photos of damage for covered perils

- List of all damaged or stolen items with values

Why Inventory Matters: Without proof of ownership and value, insurers pay minimal settlements. Detailed inventories dramatically improve claim outcomes.

The Claims Process

- Report Promptly: Notify your insurer within 24-72 hours

- File Police Reports: Required for theft claims

- Document Damage: Photograph everything before cleanup

- Create Detailed Loss List: List every damaged/stolen item with descriptions and values

- Provide Supporting Documentation: Submit receipts, photos, appraisals

- Work with Adjusters: Cooperate fully during investigation

- Don’t Dispose of Damaged Items: Until adjuster inspects them

When to Hire Public Adjusters

For large claims ($50,000+), consider public adjusters who:

- Work for you, not the insurance company

- Maximize claim settlements

- Handle documentation and negotiations

- Charge 5-15% of settlement but often increase payouts substantially

Protecting Your Personal Property

Prevention and documentation protect your belongings and coverage.

Security Measures

Reduce Theft Risk:

- Install security systems and cameras

- Use quality locks on doors and windows

- Store valuables in safes

- Don’t advertise expensive purchases (empty boxes at curb)

- Maintain inventory proving ownership

Earn Discounts: Security systems often qualify for 5-15% insurance discounts while genuinely protecting your property.

Maintenance and Care

Prevent Damage:

- Maintain plumbing to prevent water damage

- Store items properly protecting from damage

- Use climate control preventing deterioration

- Regular cleaning and maintenance

Insurance Optimization

Review Coverage Annually:

- Update limits as you acquire possessions

- Schedule new valuable items

- Verify coverage still matches inventory totals

- Increase limits if standard percentages are inadequate

Your Complete Personal Property Protection

Personal belongings insurance protects thousands in possessions you’ve accumulated furniture, electronics, clothing, jewelry, and countless items essential to your daily life. Adequate Coverage C personal property coverage with proper scheduling of valuables ensures you can actually replace everything after disasters.

Don’t assume standard coverage adequately protects you. Create detailed inventories, schedule high-value items, choose replacement cost coverage, and verify your insurance personal property limits match what you actually own.

The modest cost of proper personal property coverage is insignificant compared to the financial devastation of discovering inadequate limits after total loss events.

Our specialists help homeowners build comprehensive Personal Property Coverage with appropriate limits and valuable item scheduling through complete Home Insurance protection.

Frequently Asked Questions

Yes you don’t need original purchase receipts for all items. For inherited or gifted valuables, obtain professional appraisals documenting current value. For everyday items without receipts, insurers accept reasonable proof of ownership through photos, credit card statements, or detailed descriptions. However, claims settle faster and for higher amounts when you have strong documentation, so photograph inheritances and gifts when you receive them.

Your homeowners personal property coverage protects belongings stolen from your car not auto insurance (which only covers the vehicle itself). However, your auto insurance deductible might be lower than your homeowners deductible. File with homeowners insurance for stolen belongings and auto insurance only if the vehicle was damaged during the break-in.

Standard homeowners policies typically exclude coverage for property damage or theft related to short-term rental activities. Guest belongings aren’t covered, and damage guests cause to your personal property may not be covered either. You need short-term rental insurance endorsements or separate policies covering this exposure. Airbnb’s Host Guarantee provides some protection but has gaps and limitations.