On a Tuesday morning in March 2025, an employee making a routine delivery in a company cargo van ran a red light and struck a sedan carrying a family of four. The mother sustained a spinal fracture. The father missed three months of work. Their two children were treated for serious injuries. Total liability exposure for the business: over $1.4 million.

The business had commercial auto insurance. But its liability limit was the state minimum. The policy covered a fraction of the claim. The owner was left personally responsible for the remainder.

This is not an extreme scenario it is increasingly the median outcome in commercial auto liability claims in 2026. The National Association of Insurance Commissioners reports that the average bodily injury claim for a commercial vehicle now exceeds $44,000, and jury awards of $10 million or more called nuclear verdicts are a routine feature of commercial auto litigation. Auto liability surged 14.9% in Q4 2025, the 36th consecutive quarter of rate increases, driven by social inflation, rising medical costs, and vehicle repair expenses that climbed 9.7% following 2025 tariffs on imported auto parts.

Carrying commercial auto liability coverage is legally required. Carrying the right amount is a business survival decision. This guide explains what commercial auto liability covers, how limits work, what Florida and federal law actually.

2026 Claims Reality

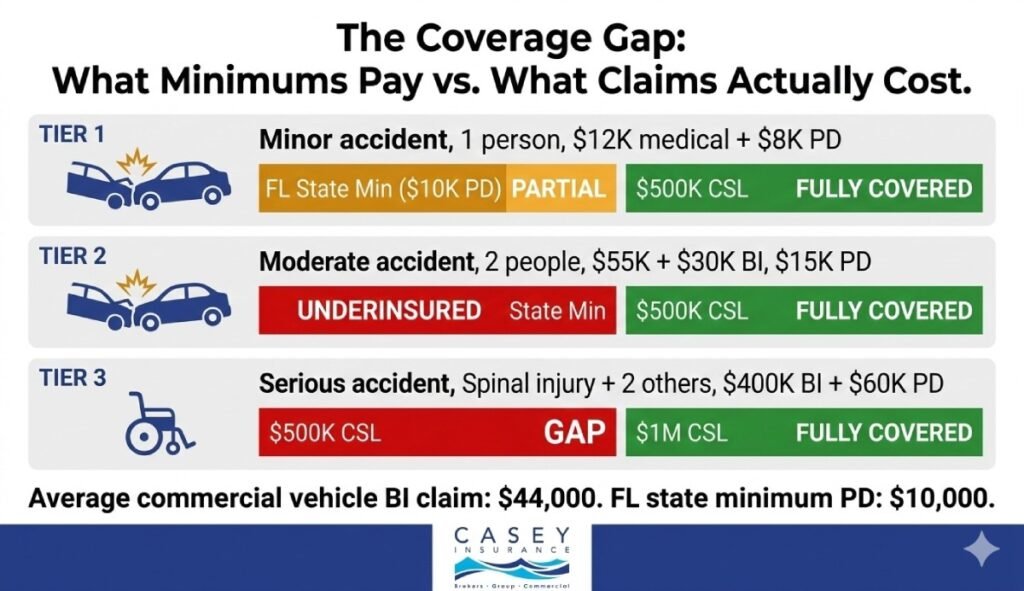

Average commercial vehicle bodily injury claim: $44,000. Average overall commercial auto liability claim: $24,000. Commercial auto liability rate increases: 14.9% in Q4 2025 the 36th consecutive quarter of increases. Motor vehicle repair costs rose 9.7% in 2025 from imported auto part tariffs. Nuclear verdicts ($10M+ jury awards) are rising in frequency across transportation-related lawsuits.

What Is Commercial Auto Liability Coverage?

Commercial auto liability coverage is the component of your commercial auto policy that pays for injuries and property damage you cause to others when one of your business vehicles is involved in an at-fault accident. It does not cover damage to your own vehicles or injuries to your own drivers those require separate collision, comprehensive, and medical payments coverage.

Commercial auto liability includes two components that always appear together:

- Bodily injury (BI) liability: Pays for the other party’s medical expenses, lost wages, rehabilitation, pain and suffering damages, and legal fees if they sue your business. In serious multi-occupant accidents, BI claims routinely reach six and seven figures.

- Property damage (PD) liability: Pays to repair or replace the other party’s vehicle or property your vehicle damaged. In Florida, where vehicle values are high and commercial damage claims often involve specialty or branded vehicles, the state minimum PD limit of $10,000 is routinely exceeded by a single-vehicle accident.

Together, these components form the financial backbone of your commercial auto liability insurance coverage. They also define your exposure in litigation your liability limit is the ceiling on what your insurer will pay. Everything above that limit is your personal or corporate responsibility.

What Liability Does NOT Cover

Commercial auto liability covers the other party’s losses not yours. Damage to your own vehicles requires collision coverage. Your driver’s injuries require medical payments or workers’ comp. Always pair liability with physical damage coverage for a complete commercial auto program. See our pages on collision coverage for commercial vehicles and comprehensive fleet coverage.

How Commercial Auto Liability Limits Work: Split Limits vs. Combined Single Limit

Commercial auto liability limits are structured in one of two ways and the difference between them can mean the gap between a fully covered claim and a six-figure shortfall.

Split Limits

A split limit policy expresses coverage as three separate numbers for example, 100/300/100. This means: $100,000 maximum per injured person (BI), $300,000 maximum total per accident (BI aggregate), and $100,000 for property damage. The sub-limits are fixed you cannot apply unused PD capacity to a large BI claim.

Combined Single Limit (CSL)

A combined single limit (CSL) policy expresses coverage as a single pool for example, $1,000,000 CSL. That one limit applies in any combination to BI per person, BI per accident, and property damage, based on the actual composition of the claim. A $1M CSL on a severe two-person accident can direct the full million toward the highest-cost items without per-person sub-limit constraints.

For most commercial operations, CSL policies offer significantly better real-world protection at a modest premium premium above split-limit policies. The table below illustrates the structural difference:

Split Limit vs. Combined Single Limit (CSL) — Coverage Structure Comparison

| Factor | Split Limit | Combined Single Limit (CSL) |

|---|---|---|

| Structure | Split Limit (e.g., 100/300/100) | Combined Single Limit — e.g., $1M CSL |

| What it means | $100K/person BI + $300K/accident BI + $100K property damage — three separate caps | One flexible pool covers BI per person, BI per accident, AND property damage in any combination |

| Flexibility | Fixed sub-limits — cannot shift unused PD to cover a large BI claim | Single pool flexes to cover the largest need in any given claim |

| Scenario: 1-person accident, $400K injury + $60K PD | Pays $100K BI + $60K PD = $160K. You owe $300K personally. | $1M CSL pays $400K + $60K = $460K. You owe $0. |

| Scenario: 4-person accident, $60K each + $25K PD | 100/300/100 pays $240K BI + $25K PD = $265K. Covered. | $500K CSL pays $265K from single pool. Fully covered. |

| Best for | Very low-risk, limited-driving operations with minimal per-person exposure | Most commercial operations — especially fleet, multi-driver, or high-liability industries |

| Typical premium difference | Lower base premium for nominally equivalent limits | 5–15% more than split limit — but substantially better real-world protection |

How Much Commercial Auto Liability Do You Actually Need?

The gap between what the law requires and what protects your business is wide and widening every year as claim costs and jury verdicts escalate.

1. State Minimums: The Legal Floor, Not the Business Protection Floor

Florida’s current commercial vehicle minimum for standard vehicles under 26,000 lbs is $10,000/$20,000 BI + $10,000 PD, with $10,000 PIP. At those limits, a single hospitalization from one at-fault accident can exhaust your entire policy in a single billing cycle. State minimums establish legal financial responsibility they were never designed to protect a business from modern accident litigation.

2. The $1 Million CSL Standard: Why It Has Become the Industry Baseline

Commercial insurance advisors consistently recommend $1,000,000 CSL as the practical baseline for any business with regular road exposure. This reflects both the current claims environment and the contractual reality: general contractors, government clients, and major commercial accounts increasingly require certificates of insurance showing $1M commercial auto liability before awarding work.

A $1M CSL covers the vast majority of commercial auto claims the $44,000 average BI claim is well within that ceiling. What $1M may not cover: a severe multi-occupant accident, a wrongful death claim, or a case driven into nuclear verdict territory by plaintiff counsel.

3. When $1M Is Not Enough: The Nuclear Verdict Environment

In 2026, nuclear verdicts jury awards of $10 million or more are an established feature of commercial auto litigation. The drivers: aggressive plaintiff litigation funding, social inflation in jury attitudes, expanding theories of corporate liability, and the increasing severity of accidents involving heavier commercial vehicles.

For businesses in higher-risk industries contractors with multi-driver fleets, delivery operations in dense metro areas, passenger transport $1M CSL plus a commercial umbrella policy has become the effective minimum for real financial protection. Umbrella policies typically start at $1M increments and can extend total coverage to $5M, $10M, or beyond.

Commercial Auto Liability Limits by Business Type — 2026 Reference

| Business / Use Type | State Minimum | Recommended Limit | Key Exposure Notes |

|---|---|---|---|

| Consultants / Professional Services | $500K CSL | $1M CSL | Low mileage, client visits; low cargo exposure |

| Retail / Light Service Vehicles | $500K–$1M CSL | $1M CSL | Regular road use; moderate public interaction risk |

| Landscaping / Trades (1–4 vehicles) | $1M CSL | $1M–$2M CSL | Tool/equipment hauling, daily job-site driving |

| General Contractors (fleet) | $1M CSL | $2M+ CSL + umbrella | Multi-driver fleet; client contracts often require $1M+ |

| Delivery / Courier Services | $1M CSL | $1M–$2M CSL | High mileage, time pressure, dense route exposure |

| Food Trucks / Mobile Operations | $1M CSL | $1M CSL | Urban routes, frequent pedestrian-adjacent stops |

| Passenger Transport / For-Hire | $1.5M–$5M CSL* | Maximum available + umbrella | State-mandated higher limits; multi-injury catastrophic risk |

| Trucking / Motor Carriers (interstate) | $750K–$5M CSL* | Maximum available + excess | FMCSA federal minimums; nuclear verdict environment |

Florida Commercial Auto Liability Requirements in 2026

Florida’s commercial auto liability landscape is among the most complex in the country shaped by a no-fault framework, weight-based vehicle minimums, federal FMCSA requirements for interstate carriers, and pending legislation that could materially change minimum requirements for all Florida drivers mid-2026.

Florida Commercial Auto Liability Requirements — 2026 Reference Table

| Vehicle / Operation Type | Minimum Required Limit | Notes for Florida Business Owners |

|---|---|---|

| Standard business vehicles (under 26,000 lbs, intrastate) | 10/20/10 BI/PD + $10K PIP | Most small business vehicles: vans, trucks, sedans. PIP required on all FL-registered vehicles. |

| PENDING: HB 1181 (effective July 1, 2026 if enacted) | 25/50/10 BI/PD — PIP repealed | Increases BI minimums; removes PIP. Verify status before mid-2026 renewal. |

| Heavy vehicles (26,000+ lbs GVWR, intrastate) | $50,000–$300,000 per §627.7415 | Weight-based FL minimums under state statute. Confirm GVWR on driver-side door label. |

| For-hire passenger vehicles (taxis, limos, rideshare) | $125K per person / $250K per incident + $50K PD | County and platform contracts often require limits above the state floor. |

| Interstate commerce vehicles (10,001+ lbs, FMCSA) | $750K CSL (non-hazmat general freight) | Federal FMCSA minimums supersede state for interstate operations. MC number required. |

| Hazardous materials carriers (FMCSA) | $5,000,000 CSL | Applies regardless of whether operations cross state lines. |

| Passenger buses / large vans (16+ passengers, interstate) | $5,000,000 CSL | Federal DOT requirement. Cannot be satisfied by umbrella — must be primary limit. |

Fleet Liability Insurance: Coverage and Pricing at Scale

Businesses operating five or more vehicles enter the realm of commercial truck fleet insurance a policy structure that manages vehicle liability as a portfolio. Fleet policies offer both coverage advantages and cost efficiencies unavailable on individual policies.

Fleet Coverage Advantages

- Blanket fleet coverage: One policy covers all listed vehicles. Adding or removing vehicles mid-term is handled by endorsement. Newly acquired vehicles are typically covered automatically for 30 days while the fleet schedule is updated.

- Consistent limits across all units: Fleet policies ensure every vehicle carries identical liability limits eliminating coverage gaps that emerge from managing multiple individual policies with different structures or renewal dates.

- Dedicated commercial claims handling: Fleet-level accounts receive dedicated commercial claims representatives familiar with business vehicle operations, cargo considerations, and employer liability issues.

Fleet Pricing and Discount Levers

- Fleet discount threshold: Most commercial insurers apply fleet pricing — typically 5–25% per-vehicle savings — at 5+ vehicles. A 10-vehicle contractor fleet saving 20% per vehicle at $3,500/vehicle/year saves $7,000 annually.

- Telematics programs: GPS tracking and dashcam programs reduce premiums by 10–25%. Progressive’s Snapshot ProView saves fleet operators 5% at enrollment alone, with additional discounts for demonstrated safe driving data.

- Driver safety programs: Documented driver training, formal MVR (motor vehicle record) review policies, and vehicle maintenance schedules earn premium credits at renewal. Carriers are increasingly aggressive about rewarding documented fleet safety investment.

- Multi-policy bundling: Bundling commercial auto with GL, commercial property, and workers’ comp through the same carrier typically yields an additional 10–15% multi-policy discount across all bundled lines.

Fleet Safety ROI

A single at-fault commercial auto claim for a moderate injury can increase your fleet renewal premium by 15–25% for 3–5 years. A dashcam program costs $200–$800 per vehicle to install and directly prevents the inflated demand letters and attorney involvement that turns a $15,000 fender bender into a $90,000 settlement. The math strongly favors proactive fleet safety investment.

How to Get the Best Price on Commercial Auto Liability Coverage

The businesses that consistently get the best pricing on commercial auto liability share four characteristics:

- They work with an independent advisor: Independent commercial insurance advisors access multiple carriers simultaneously Progressive, The Hartford, Travelers, Nationwide, Zurich, and dozens of specialty markets placing your account with the carrier that prices your specific risk most competitively. Direct carrier relationships limit you to one pricing structure.

- They invest in documented fleet safety: Telematics data, dashcam programs, formal MVR reviews, and written driver safety policies are underwriting signals that directly influence tier placement and rate. Carriers reward documented risk management with lower base rates and better renewal terms.

- They bundle coverages: Commercial auto, GL, commercial property, and workers’ comp with one carrier yields multi-policy discounts of 10–15% across all bundled lines and often produces better claims service than fragmented multi-carrier arrangements.

- They pay annually and review limits every year: Annual premium payment saves 5–13% over monthly installments. Annual limit reviews with your advisor ensure coverage keeps pace with claims inflation a $500K limit from five years ago may now represent a 50% underinsurance gap relative to current claim severities.

For context on the broader commercial auto landscape, see our guides on commercial auto insurance vs. personal auto and common commercial auto insurance mistakes.

FAQs About Commercial Auto Liability Coverage

For most small businesses with regular road exposure, $1,000,000 CSL is the practical baseline recommended by commercial insurance advisors and required by most commercial contracts. The average commercial vehicle bodily injury claim exceeds $44,000, and serious multi-person accidents routinely produce six-to-seven-figure claims.

A split limit policy separates coverage into three fixed sub-limits: bodily injury per person / bodily injury per accident / property damage (e.g., 100/300/100). These sub-limits cannot be shifted unused PD capacity cannot cover a large BI claim. A CSL policy provides one flexible pool e.g., $1M CSL allocable in any combination to cover the full range of losses in a given claim. CSL is generally preferred for commercial operations because real-world accidents rarely present costs that fit neatly within rigid sub-limit structures. A $1M CSL typically costs 5–15% more than a nominally equivalent split-limit policy but provides substantially better protection in complex or severe claims.

A commercial fleet insurance policy covers all listed business vehicles under a single policy — providing consistent liability limits, physical damage coverage, and any-authorized-driver provisions across the entire fleet. Fleet policies typically include: commercial auto liability (BI and PD), collision, comprehensive, medical payments, uninsured/underinsured motorist coverage, and optional add-ons including hired and non-owned auto, rental reimbursement, and roadside assistance.

Yes — consistently. Independent commercial insurance advisors access multiple carriers simultaneously, placing your account with the insurer that prices your specific risk profile most competitively. Direct carrier relationships lock you into a single pricing structure. Beyond carrier access, advisors can identify bundling opportunities (10–15% multi-policy discount), telematics programs (10–25% savings), fleet discount qualification, and annual vs. monthly payment structures (5–13% savings).

Right-Size Your Commercial Auto Liability Before the Next Renewal — Not After the Next Claim

The 2026 commercial auto liability market is defined by rising claim severity, expanding litigation risk, and a Florida regulatory environment likely to shift materially before the year ends. The businesses that review their limits now matching coverage to the realities of today’s claims and legal environment emerge from serious accidents financially intact.

Our commercial insurance advisors help businesses across Florida and nationwide structure commercial auto liability programs that provide genuine protection at the best available market pricing. Explore our full commercial auto liability coverage options and contact us for a multi-carrier commercial auto liability quote tailored to your specific vehicles, drivers, and operations.