A fire breaks out in your restaurant kitchen on a Saturday night. The building is heavily damaged. Your property insurance will eventually cover the repairs but that process takes four months. During those four months, your business generates zero revenue. Your rent is still due. Your key employees need to be paid if you want to keep them, your loan payments don’t stop and our utility accounts stay open. The bills don’t care that your doors are closed.

This is the financial gap that business income insurance also called business interruption insurance, is specifically designed to fill. And it is a gap that proves catastrophic for businesses that don’t have it: according to the U.S. Small Business Administration, 60% of small businesses hit by a disaster never reopen. The Institute for Business and Home Safety reports that 75% of businesses in serious disruption situations close permanently within 18 months of the event.

Business income coverage doesn’t prevent the disaster. It prevents the disaster from becoming the end of your business.

The Stakes:

60% of businesses hit by a disaster never reopen (SBA). 75% of businesses in serious disruption situations close permanently within 18 months (IBHS). 67% of Florida small businesses are underinsured for business interruption. SBA approved $1.4 billion in disaster loans to Florida businesses after Hurricanes Helene and Milton alone — reflecting the scale of income disruption a major storm creates. Business income coverage is the primary defense before those loans become necessary.

What Is Business Income Insurance?

Business income insurance (also called business interruption insurance or BI coverage) pays for the net income your business loses when a covered property event forces you to close or operate at reduced capacity. It replaces the revenue stream your business would have generated, covers your ongoing operating expenses that continue during the shutdown, and does so for a defined period while your property is restored to operational condition.

Business income coverage typically pays for:

- Lost net profits: The income your business would have earned during the closure period, based on pre-loss financial performance

- Continuing payroll: Wages for key employees retained during shutdown — essential to keep your team intact for reopening

- Rent and mortgage payments: Your fixed location costs continue regardless of whether you’re generating revenue

- Loan and debt service: Business loan payments due during the closure period

- Utilities: Ongoing utility accounts that remain active during repairs

- Taxes: Tax obligations that come due during the restoration period

Business income coverage is triggered by direct physical loss or damage to your insured property from a covered peril — fire, theft, vandalism, wind damage, and other events covered under your commercial property policy. This trigger requirement is critical and non-negotiable: without a covered property damage claim, there is no business income claim. A Florida court reaffirmed this in Fontainebleau Florida Hotel LLC v. Westchester Surplus Lines Insurance Co. (Fla. 3d DCA, March 2025), ruling that BI coverage requires actual direct physical loss — not merely disruption or inconvenience.

The Trigger Rule — Critical for Florida Businesses:

Business income coverage requires a covered physical property loss as the trigger. Revenue loss from reduced customer traffic after a hurricane (even if your property is undamaged), supply chain disruption, or power outages at the utility provider level do NOT trigger standard BI coverage without the underlying property damage claim. Each of these scenarios requires specific endorsements to be covered.

What Is Extra Expense Coverage?

Extra expense coverage pays for necessary costs your business incurs to continue operating or to speed up reopening that would not have been incurred if the covered loss hadn’t happened. Where business income coverage replaces revenue you lost because you couldn’t operate, extra expense coverage pays for the cost of operating around the damage maintaining business continuity while repairs are underway.

Common extra expense claim items include:

- Temporary location lease: Renting a temporary retail space, office, or production facility while your primary location is repaired

- Equipment rental: Leasing replacement equipment or machinery during the restoration period

- Moving and relocation costs: The physical cost of setting up and then dismantling a temporary operating location

- Overtime wages: Paying employees overtime to accelerate restoration, rebuild inventory, or maintain customer service during the disruption

- Emergency vendor costs: Expedited shipping, emergency contractors, or premium-rate service providers engaged to speed reopening

- Increased advertising: Marketing costs to inform customers of your temporary location or communicate your reopening

In most BOP policies, business income and extra expense coverage are bundled into a single BI/EE component one combined coverage with a single limit that covers both lost income and the extra costs incurred to minimize that income loss. The extra expense component serves the insurer’s interest as well as yours: a business that reopens in month two from a temporary location generates fewer total claims than one that stays closed for month six.

Business Income vs. Extra Expense: What Each Covers

| Business Income Coverage | Extra Expense Coverage | |

|---|---|---|

| What it pays for | Lost net income — revenue your business would have earned but didn’t because of the shutdown | Necessary extra costs incurred to continue or resume operations that would not exist without the covered loss |

| Who it’s for | Any business that loses revenue during closure — retailers, restaurants, service firms, medical offices | Businesses that choose to keep operating from a temporary location or need to accelerate recovery |

| Typical expenses covered | Lost profits; ongoing payroll; rent/mortgage; loan repayments; utilities; taxes due during closure period | Temporary office or retail lease; equipment rental; relocation moving costs; overtime wages to speed reopening; emergency vendor costs |

| Trigger requirement | Direct physical loss or damage to your insured property from a covered peril (fire, theft, vandalism, storm) | Same trigger: direct physical property damage. Extra expense pays the additional costs of working around the damage |

| Coverage period | From end of waiting period (48–72 hrs) through restoration period — up to 12 months standard | Concurrent with restoration period — expires when property is repaired and normal operations resume |

| Waiting period | Usually 48–72 hours after the covered event — coverage is not retroactive to minute zero of closure | Same waiting period applies — extra expense coverage begins when BI coverage begins |

| How limits are set | Based on projected net income for the coverage period — use 12-month income history as baseline; Florida worst-case: 6-month recovery minimum | Usually a sub-limit within the BI/EE coverage; should reflect realistic relocation and continuity costs for your operation type |

| In a BOP | Standard inclusion in most BOP policies from major carriers — confirm it is included (not all BOP carriers include it automatically) | Typically bundled with BI in a combined Business Income and Extra Expense (BI/EE) component in a BOP |

What Business Income Coverage Covers and What It Doesn’t

One of the most important exercises before a loss occurs is understanding exactly what your BI coverage does and does not respond to. The exclusions below represent the most common sources of disputes, underinsurance surprises, and coverage gaps:

| What BI/EE COVERS | What BI/EE Does NOT Cover |

|---|---|

| ✅ Lost net income during covered property closure | ❌ Pandemic / communicable disease closures (explicitly excluded in most policies post-2020) |

| ✅ Ongoing payroll for retained employees during shutdown | ❌ Closures with no direct physical property damage trigger |

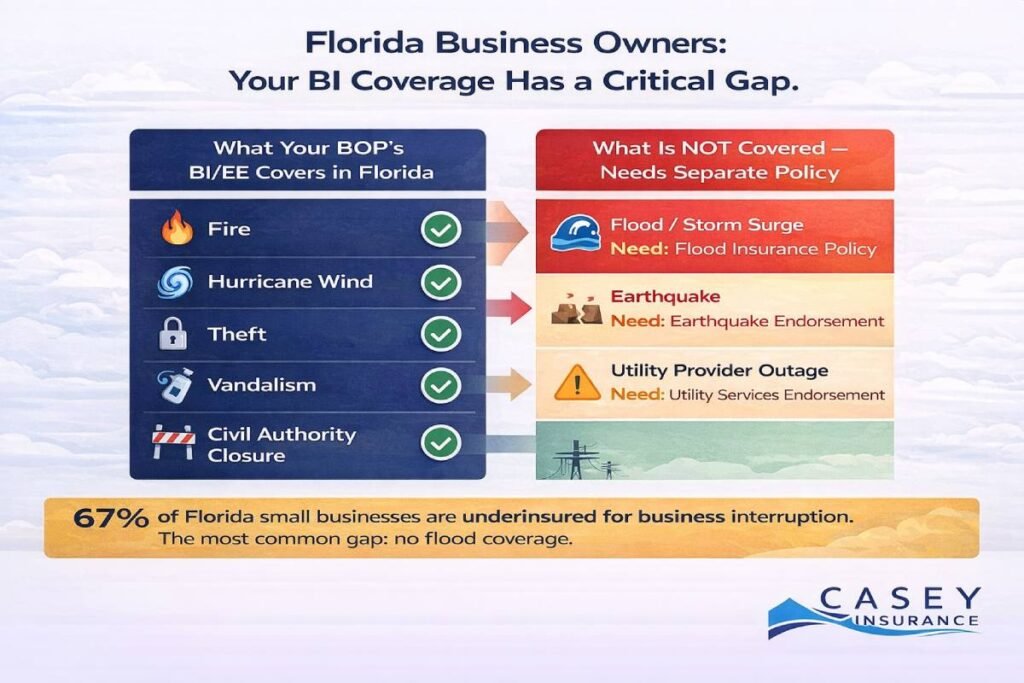

| ✅ Rent / mortgage payments while closed | ❌ Flood damage — requires separate flood policy (critical for Florida businesses) |

| ✅ Loan and debt service payments due during closure | ❌ Earthquake damage — requires separate earthquake endorsement |

| ✅ Utility costs that continue while closed | ❌ Revenue losses from reduced customer traffic after reopening (post-loss market conditions) |

| ✅ Taxes due during the closure period | ❌ Slow business or seasonal revenue decline unrelated to covered property damage |

| ✅ Temporary relocation costs (extra expense) | ❌ Revenue lost beyond the policy’s restoration period / coverage limit |

| ✅ Civil authority closures — government-ordered closure due to damage to nearby property | ❌ Loss of income from cyber incidents without physical damage (need cyber BI endorsement) |

| ✅ Equipment rental to accelerate reopening (extra expense) | ❌ Supply chain disruption losses unless contingent BI endorsement is added |

| ✅ Overtime wages to speed recovery (extra expense) | ❌ Utility service interruption at the utility provider level (need utility services endorsement) |

Civil Authority Coverage:

Most BI policies include a civil authority provision coverage for lost income when a government order prevents access to your business due to damage to nearby property, not your own. After Hurricanes Ian, Helene, and Milton, this provision was critical for Florida businesses on barrier islands and in evacuation zones whose buildings were intact but inaccessible due to government-ordered closures. Confirm your policy includes civil authority coverage with your advisor.

Understanding the Period of Restoration

The period of restoration is the defined window during which your business income coverage pays claims from the end of the waiting period (typically 48–72 hours after the covered event) until the earlier of: the date your property is repaired and you can resume normal operations, or the maximum coverage period stated in your policy.

Standard BOP policies cap the restoration period at 12 months. For many business types, this is adequate a restaurant fire with a 3-month rebuild timeline, a retail theft with a 2-week closure, a vandalism event requiring 30 days for repairs. But for businesses in high-risk environments, or for losses that involve major structural damage, equipment replacement, or permitting and code compliance issues, 12 months may not be sufficient.

Florida’s Extended Restoration Reality

For Florida businesses, the standard 12-month restoration cap is a risk. After a major hurricane event, the recovery timeline is driven by contractor availability, materials supply, permitting backlogs, and ongoing economic disruption — factors that routinely extend reconstruction beyond 12 months. Insurance experts note that post-catastrophe economies often see 2–3 year recovery timelines for businesses in heavily impacted areas, while the standard BOP BI cap stops at 12 months.

Florida business owners should discuss extended period of indemnity options typically endorsements that extend the restoration period to 18 or 24 months with their advisors. The additional premium for this extension is modest relative to the exposure it addresses.

The Waiting Period

Most BI/EE policies include a waiting period — typically 48–72 hours after the covered event before coverage activates. This functions like a time-based deductible: minor disruptions lasting less than 72 hours do not generate BI claims. For events that trigger the waiting period, coverage is not retroactive to the moment of loss — it begins after the waiting period has elapsed. Confirm the waiting period in your policy and factor it into your financial reserve planning.

How to Calculate the Right Business Income Coverage Limit

The single most important and most commonly mishandled aspect of business income insurance is limit setting. 67% of Florida small businesses are underinsured for business interruption and underinsurance at claim time typically results in proportional payout reductions, leaving the business to self-fund the shortfall during an already financially strained period.

Here is the step-by-step framework for calculating an adequate BI/EE limit:

| Action | What To Do / Key Notes | |

|---|---|---|

| Step 1 | Calculate your annual net income | Annual revenue minus ongoing business expenses (not including non-continuing costs like raw materials you won’t buy during closure). Use the last 12 months of actual financials as the baseline. |

| Step 2 | Estimate your restoration period | How long would it realistically take to repair or replace your physical space and equipment? For Florida businesses: a hurricane recovery of 6–12 months is a realistic worst-case scenario. Use the longer estimate, not the optimistic one. |

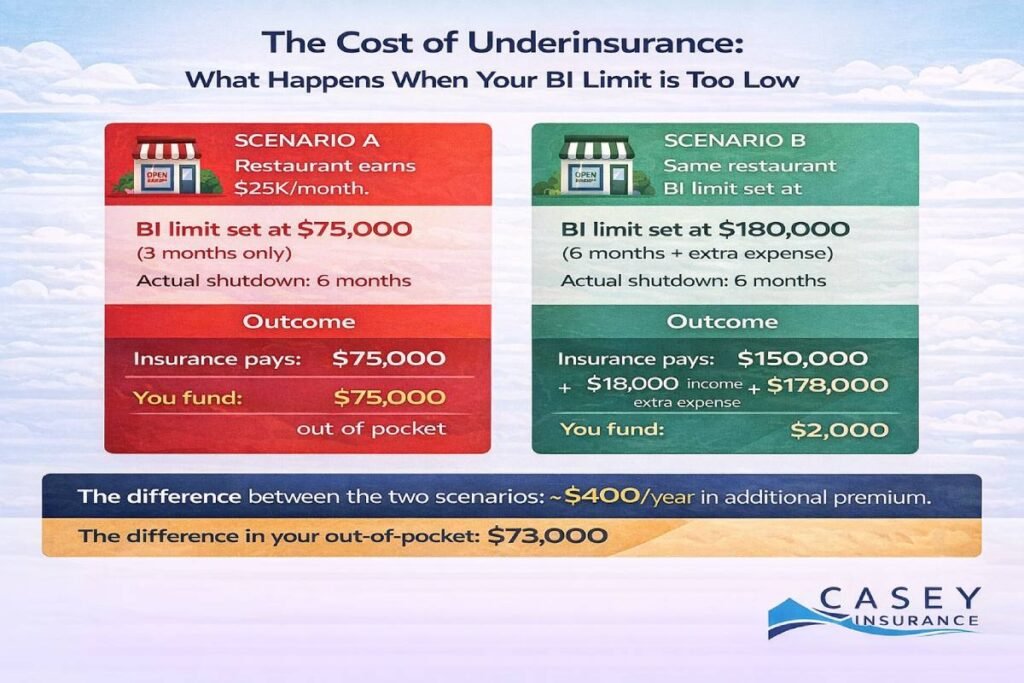

| Step 3 | Calculate your projected BI exposure | Monthly net income × estimated months of closure = your minimum BI coverage limit. Add 10–15% buffer for inflation, cost overruns, and delays. |

| Step 4 | Add extra expense estimate | What would it cost to operate from a temporary location? Lease costs, equipment rental, relocation, overtime wages. Include these in your limit calculation as a separate EE sub-limit. |

| Step 5 | Set your policy limit | Set your BI/EE limit at or above your projected exposure. Do NOT underinsure — 67% of Florida small businesses are underinsured for BI (insurance research data 2025). Underinsurance at claim time triggers proportional payout reductions. |

| Verification | Review annually before renewal | BI exposure changes as your revenue grows. A business earning $40K/month in 2024 but $55K/month in 2026 needs a materially higher limit. Review limits every renewal cycle — especially before Florida hurricane season. |

The Coinsurance Trap:

Some BI policies contain a coinsurance clause if you insure for less than a required percentage of your actual BI exposure, your claim payout is reduced proportionally. Example: if you should have $200,000 in BI coverage but only carry $100,000, a $120,000 claim may only pay $60,000. Work with your advisor to either eliminate coinsurance requirements or ensure your limit meets the requirement to avoid this penalty.

Business Income Coverage in Florida: What Business Owners Must Know

Florida’s combination of hurricane exposure, high litigation activity, and complex insurance regulations makes business income coverage more important and more nuanced than in most other states. Key Florida-specific considerations:

1. Flood Is Not Business Income

Florida’s most common catastrophic business disruption scenario — hurricane storm surge and flooding — is explicitly excluded from standard commercial property coverage and therefore from standard BI/EE coverage. A flood event requires a separate flood insurance policy (National Flood Insurance Program or private market). Without one, a four-week flood closure generates no BI claim. This is the most critical coverage gap for Florida businesses and the most common source of underinsurance after major storms.

2. Hurricane Deductibles and Waiting Periods

Many Florida commercial property policies contain separate hurricane deductibles often expressed as a percentage (1%–5%) of insured property value rather than a fixed dollar amount. A business with $2,000,000 in insured property value and a 2% hurricane deductible has a $40,000 deductible on hurricane claims. This deductible applies to both the property damage claim and the BI/EE claim that flows from it. Confirm your hurricane deductible structure before hurricane season and ensure your cash reserves can absorb it.

3. Post-Hurricane Claim Complexity

Following Hurricanes Helene and Milton, the SBA approved $1.4 billion in disaster loans for Florida businesses and residents a figure that underscores the scale of income disruption these storms create. Business interruption claims in post-hurricane environments are among the most complex insurance claims a small business will ever file: they require detailed financial documentation, pre-loss income substantiation, and careful period of restoration calculations. Engaging a public adjuster or your insurance advisor early in the claims process materially improves outcomes.

4. The Direct Physical Loss Requirement in Florida Courts

Florida courts have consistently affirmed that BI coverage requires actual, direct physical property damage from a covered peril. In Fontainebleau Florida Hotel LLC v. Westchester Surplus Lines Insurance Co. (March 2025), the Third District Court of Appeal reaffirmed this standard, rejecting BI claims without underlying property damage. For Florida businesses, this means your BI claim must be built on a solid documented property damage claim — documentation quality at the property damage stage directly affects your BI recovery.

Frequently Asked Questions: Business Income and Extra Expense Coverage

Business income insurance also called business interruption insurance pays for the net income your business loses when a covered property event (fire, theft, vandalism, wind damage) forces you to close temporarily. It covers lost profits, ongoing payroll, rent, loan payments, utilities, and taxes that continue during the shutdown. Coverage activates after a 48–72 hour waiting period and pays for the duration of the period of restoration — the time it takes to repair your property and resume operations — up to the policy’s maximum (usually 12 months). It is triggered by direct physical loss to your insured property from a covered peril, not by revenue losses alone.

Business income coverage replaces lost revenue. Extra expense coverage pays for additional costs you incur to keep operating or accelerate reopening during the restoration period. If you rent a temporary location, lease replacement equipment, pay overtime wages, or hire emergency contractors to speed repairs — those costs are extra expense, not business income. In most BOP policies, both are bundled into a single BI/EE component with a combined limit.

The formula: (Monthly net income) × (realistic months to restore) + extra expense budget = your minimum BI/EE limit. For a Florida business, use a 6-month minimum restoration estimate — not an optimistic 2-month estimate. Add a 10–15% buffer for cost inflation and delays. Review your limit at every annual renewal as your revenue grows. 67% of Florida small businesses are underinsured for BI — the most common error is calculating limits based on best-case recovery timelines rather than realistic worst-case scenarios.

Don’t Let a Covered Loss Become a Permanent Closure

Commercial property insurance rebuilds your building. Business income insurance keeps your business alive while that happens. They are not the same coverage and one without the other leaves a gap that has permanently closed thousands of Florida small businesses after hurricanes, fires, and other covered events. Our commercial insurance advisors help Florida and nationwide businesses structure BI/EE coverage that is properly sized for their actual revenue exposure, accounts for realistic restoration timelines, and includes the Florida-specific endorsements extended indemnity periods, civil authority provisions, and flood coverage referrals that standard BOP policies often miss. Explore our Business Income and Extra Expense Coverage, and contact us for a BI/EE coverage assessment before the next hurricane season.