A kitchen fire destroys your restaurant’s cooking equipment and damages the building. A smash-and-grab theft clears out half your retail inventory overnight. A burst pipe floods your office, destroying computers and ruining furniture. A hailstorm shatters your storefront windows and damages your exterior signage.

In each case, your business has suffered a direct financial loss not from a third-party lawsuit, not from a liability claim, but from physical damage to your own property. This is the exposure that commercial property insurance inside your Business Owners Policy (BOP) is designed to address.

Property coverage is one of the two structural pillars of a BOP the other being general liability. Together, they form the foundation of small business protection. But unlike liability, which is typically well understood, property coverage is where the most common and most costly coverage errors occur: wrong valuation methods, underinsurance against today’s reconstruction costs, missing asset categories, and critical exclusions that business owners don’t discover until claim time.

2026 Property Coverage Context:

Commercial reconstruction costs rose 4.4% YoY nationally in 2025 some states saw increases above 7%. 75% of commercial buildings are underinsured nationally. Coinsurance penalties average 15–25% of the claim amount when underinsurance is identified. Commercial property insurance market is stabilizing: U.S. P&C premium growth expected to slow from 5.5% (2025) to ~3% (2026). Standalone commercial property averages $800/year for small businesses.

What Is Property Coverage in a BOP?

The commercial property component of a BOP pays to repair, rebuild, or replace your business’s physical assets when they are damaged or destroyed by a covered event. It is first-party coverage it protects your own property, not third-party claims. Your BOP’s property coverage operates entirely separately from its general liability component, each with its own limit and responding to different types of losses.

BOP property coverage applies to three primary categories of business assets:

- Buildings: The physical structure of your business location walls, roof, floors, permanently installed fixtures, HVAC systems, wiring, plumbing, and built-in improvements whether you own the building outright or it is financed

- Business personal property (BPP): All moveable business assets inside or adjacent to your building equipment, computers, furniture, inventory, stock, supplies, and business-use tools. This is the most variable and often most underinsured category

- Leasehold improvements and betterments: Permanent modifications you made to a space you lease custom build-outs, installed countertops, specialty lighting, partition walls that revert to the landlord at lease end but are your property under the policy during the lease term

The property coverage limit in your BOP is the maximum your insurer will pay for a covered loss. If a fire destroys your restaurant and the total replacement cost is $340,000, but your property limit is $200,000, you fund the $140,000 gap. Setting the right limit and understanding what valuation method your policy uses is the most consequential property coverage decision you’ll make.

What BOP Property Coverage Covers — and What It Doesn’t

Standard BOP property coverage operates on a named perils or ‘special form’ basis, depending on your carrier and policy. Most BOP policies use Special Form (open perils) — meaning coverage applies to all causes of loss except those specifically excluded. Understanding the exclusions is as important as understanding the inclusions:

| BOP Property COVERS | BOP Property Does NOT Cover |

|---|---|

| ✅ The building you own or lease (including permanent fixtures, installed equipment, HVAC, and built-in improvements) | ❌ Flood damage — requires separate flood insurance policy (NFIP or private market) |

| ✅ Business personal property: equipment, computers, furniture, tools, inventory, and business-use supplies | ❌ Earthquake damage — requires separate earthquake endorsement or standalone policy |

| ✅ Improvements and betterments — leasehold improvements you made to a space you rent | ❌ Mechanical/electrical breakdown — covered by Equipment Breakdown endorsement, not standard property |

| ✅ Fire damage — including structure, contents, and smoke damage | ❌ Employee theft — requires Crime/Employee Dishonesty endorsement or standalone fidelity bond |

| ✅ Theft and burglary — stolen property and forced-entry damage | ❌ Vehicles — business vehicles are covered under commercial auto, not BOP property |

| ✅ Vandalism — deliberate damage to your building or contents | ❌ Land — the value of land under your building is not covered; only the structure itself |

| ✅ Wind damage — hurricane winds, hail, tornadoes (note: NOT storm surge / flood) | ❌ Professional tools at off-premises job sites — may require Inland Marine or Contractor’s Equipment endorsement |

| ✅ Lightning strikes — electrical and structural damage | ❌ Accounts receivable data loss — standard property does not cover electronic data; requires cyber or data endorsement |

| ✅ Water damage from internal sources — burst pipe, appliance failure (not flood) | ❌ Intentional damage by the owner or named insured |

| ✅ Debris removal after a covered property loss | ❌ Wear and tear, gradual deterioration, rust, or corrosion |

| ✅ Glass breakage — storefront, display windows, interior glass | ❌ Property at off-premises locations unless specifically scheduled or endorsed |

The Flood Exclusion — Florida’s Most Costly Property Gap:

Hurricane wind damage to your building is covered under standard BOP property. Hurricane-driven storm surge and flooding is NOT. After Hurricane Ian, hundreds of Florida businesses discovered this distinction at claim time. Without a separate flood insurance policy NFIP or private market flood damage to your building, equipment, and inventory generates zero property coverage payout. Verify your flood coverage before every hurricane season.

Replacement Cost vs. Actual Cash Value: Your Most Important Property Coverage Decision

How your policy values damaged or destroyed property and how much it pays when a loss occurs depends entirely on the valuation method specified in your policy. This is one of the most consequential and most commonly misunderstood aspects of commercial property insurance, and the source of many claim-time surprises.

Commercial Property Valuation Methods — Comparison

| Valuation Type | What It Pays | Example | Best Fit / Key Note |

|---|---|---|---|

| Replacement Cost Value (RCV) | Pays to repair or replace damaged property with a new item of similar kind and quality — no depreciation deduction | A 5-year-old laptop destroyed in a fire is replaced with a comparable new model at today’s prices | Highest premium; best protection; most common for BOP property coverage |

| Actual Cash Value (ACV) | Pays replacement cost minus depreciation — the older the asset, the lower the payout | That same 5-year-old laptop at 50% depreciation: payout = 50% of replacement cost. You fund the rest. | Lower premium; significant out-of-pocket gap for older assets; default in many policies if RCV not specified |

| Agreed Value | Policy specifies a pre-agreed value for your property; coinsurance clause is suspended as long as limit ≥ agreed value | Your property is insured at $800,000 agreed value — no coinsurance penalty applies if a loss occurs below that limit | Eliminates coinsurance risk; requires annual Statement of Values (SOV) renewal to maintain suspension |

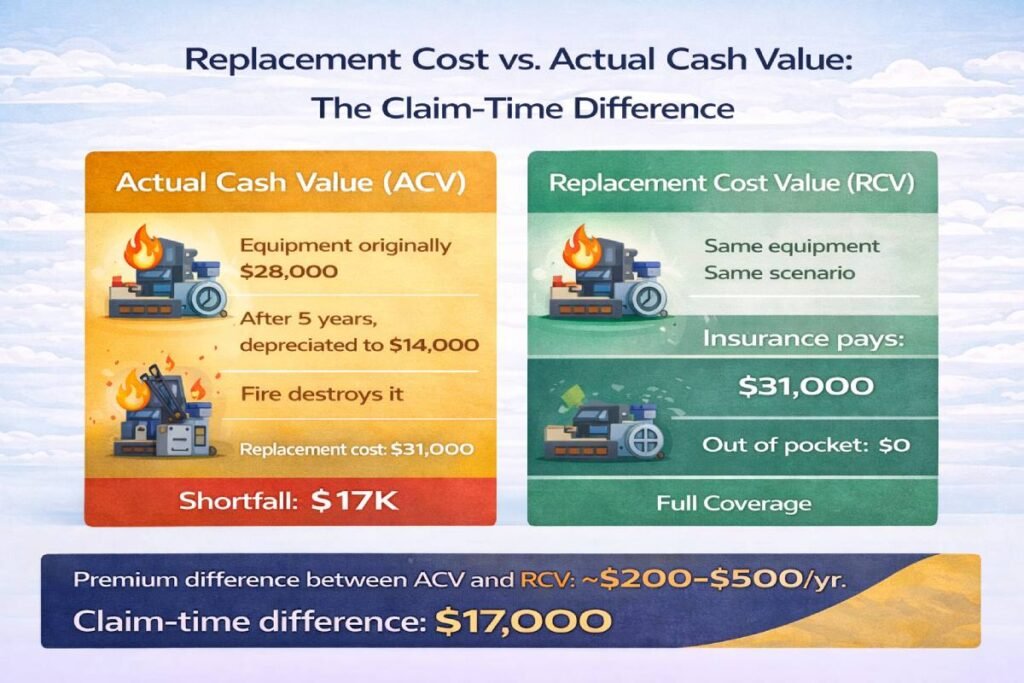

The RCV vs. ACV Example in Practice

A restaurant’s walk-in refrigeration unit — originally purchased for $28,000 — is destroyed in a kitchen fire after five years of use. Depreciation has reduced its ACV to approximately $14,000. Replacement cost for an equivalent unit today: $31,000 (reflecting inflation in equipment costs).

- ACV policy payout: $14,000 — you fund the remaining $17,000 out of pocket to reopen

- RCV policy payout: $31,000 — you replace the unit and reopen without a capital expenditure gap

The annual premium difference between ACV and RCV coverage on a policy at this value level is typically $200–$500. The out-of-pocket difference at claim time: $17,000. The math strongly favors RCV for any business asset your operation depends on to generate revenue.

The Coinsurance Clause: Why Underinsurance Costs More Than You Think

Most commercial property policies including the property component of a BOP contain a coinsurance clause that requires you to insure your property to at least a specified percentage of its full value (typically 80% or 90%). If you don’t meet that threshold, your insurer applies a coinsurance penalty that proportionally reduces your claim payout — even on a small, partial loss.

How the Coinsurance Penalty Works

The formula: (Insurance Carried ÷ Insurance Required) × Loss Amount = Claim Payment

Example: Your building has a true replacement cost of $500,000. Your policy has an 80% coinsurance requirement, meaning you’re required to carry at least $400,000 in coverage. You’ve insured it at $300,000 — thinking the lower premium was a smart savings. A fire causes $150,000 in damage.

- Coinsurance calculation: $300,000 ÷ $400,000 × $150,000 = $112,500 — your insurance pays $112,500, not $150,000

- You absorb the remaining $37,500 out of pocket, plus the full deductible — on a $150,000 partial loss where you expected 100% coverage

According to the Insurance Information Institute, coinsurance penalties average 15–25% of the claim amount when underinsurance is identified. Verisk research indicates that approximately 75% of commercial buildings nationwide are underinsured often because limits were set at property purchase or lease inception and never updated to reflect rising construction costs.

In 2025, commercial reconstruction costs increased 4.4% nationally and above 7% in some states. A building that cost $400,000 to rebuild three years ago may cost $450,000–$475,000 to rebuild today. If your property limit hasn’t kept pace, you are almost certainly carrying a coinsurance exposure without knowing it.

What to Include in Your BOP Property Schedule: Asset-by-Asset Guide

One of the most common property coverage gaps is not the valuation method it’s incomplete asset scheduling. Business owners often insure the headline items (building and major equipment) but miss categories of business property that would be expensive to replace. Here is the complete asset inventory to review with your advisor:

BOP Property Coverage — Asset Categories and Key Guidance

| Asset Category | What to Include | Key Notes / Common Mistakes |

|---|---|---|

| Building (if owned) | Full replacement cost — rebuild from ground up, including materials + labor at today’s construction prices. Florida: reconstruction costs up 4.4% YoY nationally (2025 data). | Undervaluing your building triggers coinsurance penalties. 75% of commercial buildings are underinsured nationally (Verisk). Get a professional replacement cost appraisal. |

| Leasehold Improvements | Include all permanent improvements YOU made to a leased space — custom fixtures, built-out offices, installed equipment | These are YOUR property under a BOP even in a leased space. Document all improvements made since moving in — photos + receipts. |

| Equipment & Machinery | New replacement cost of all owned or leased business equipment, computers, production machinery, specialized tools | Include serial numbers and purchase records. Update the schedule annually. Don’t insure at original purchase price — insure at current replacement cost. |

| Inventory / Stock | Peak seasonal value — the highest inventory level you typically carry during your busiest period | Insure at peak, not average. A retailer that carries $80K inventory at Christmas but only $30K in January should insure at $80K. |

| Furniture & Fixtures | All business furniture, display cases, countertops, built-in shelving, and interior fixtures | Include interior signage, branded display elements, and permanently installed items. Don’t forget back-office furniture. |

| Business Personal Property (BPP) | All loose business property not permanently attached to the building — supplies, stock, portable equipment, electronics | BPP limit is separate from the building limit. A restaurant with $25K in kitchen equipment + $15K supplies needs $40K+ in BPP coverage. |

| Tenant/Bailee Property | Property belonging to customers or clients temporarily in your care — if your business holds third-party property | BOP property typically does not cover third-party property in your care — requires Bailee Coverage endorsement. Common for salons, auto shops, cleaners. |

BOP Property Coverage in Florida: Key Considerations

Florida’s unique combination of hurricane risk, high litigation environment, and elevated construction costs creates a commercial property insurance landscape that requires attention beyond the standard BOP structure. Florida business owners need to address four specific considerations:

1. Hurricane Wind vs. Flood — The Critical Distinction

Hurricane wind damage to your building, equipment, and inventory is generally covered under BOP property. Hurricane-driven flood and storm surge is not. After Hurricanes Ian, Helene, and Milton, this distinction determined which Florida businesses recovered and which did not. The SBA approved over $1.4 billion in disaster loans to Florida businesses and residents after Helene and Milton alone but those loans reflect the scale of losses that were not covered by standard property insurance. Every Florida business with a physical location should carry a separate flood insurance policy.

2. Hurricane Deductibles

Many Florida commercial property policies including those bundled in BOPs — carry separate hurricane deductibles expressed as a percentage of insured property value (typically 2%–5%) rather than a fixed dollar amount. A business with $600,000 in insured property and a 2% hurricane deductible carries a $12,000 deductible on any hurricane-related property claim. Confirm your hurricane deductible structure before hurricane season and verify your cash reserves can absorb it without disrupting operations.

3. Reconstruction Cost Inflation

Florida’s construction market has experienced above-average cost inflation driven by material costs, labor shortages, and storm recovery demand. Commercial reconstruction costs rose 4.4% nationally in 2025, with coastal and hurricane-prone states often seeing higher increases. A building insured at its 2022 replacement cost may now be 15–20% underinsured relative to current rebuild costs — exposing the owner to a coinsurance penalty on top of already-elevated out-of-pocket exposure. Request a professional replacement cost update at every renewal.

4. Off-Premises Property

Standard BOP property coverage typically applies to property at your listed business location. Property temporarily removed — laptops taken to client sites, equipment transported to job locations, inventory in transit — may not be covered without specific endorsements. Inland Marine insurance (sometimes called a Floater) extends property coverage to business assets while they’re away from your primary location — essential for any business with mobile operations, field service employees, or contractors who regularly transport equipment.

See our full property coverage BOP and our overview of the complete Business Owners Policy. Also review our guides on business income and extra expense coverage and what is a BOP for the full picture.

Frequently Asked Questions: BOP Property Coverage

BOP property coverage protects three categories of business assets: buildings (the physical structure, fixtures, and permanently installed systems), business personal property (equipment, computers, furniture, inventory, tools, and supplies), and leasehold improvements (permanent modifications you made to a leased space).

A coinsurance clause requires you to insure your property to at least 80%–90% of its full replacement value. If your coverage falls below that threshold, your insurer applies a penalty that reduces your claim payout proportionally — even on partial losses. To avoid it: insure at 100% of current replacement cost (get a professional appraisal); elect an Agreed Value endorsement (suspends coinsurance); or add an Inflation Guard endorsement (auto-adjusts limits annually for construction cost inflation).

Don’t Wait for a Fire to Find Out Your Property Limit Was Set Three Years Ago

BOP property coverage is one of the most straightforward protections in commercial insurance — and one of the most commonly underbuilt. The difference between a properly structured property limit and one that was set at policy inception and never updated can be the difference between a full recovery and a six-figure funding gap at claim time.Our commercial insurance advisors help Florida and nationwide businesses perform property coverage audits inventorying assets, confirming replacement cost values, identifying valuation method gaps, and structuring limits that reflect what your business actually owns and what it would actually cost to rebuild. Explore our BOP property coverage, review our full Business Owners Policy program, and contact us for a property limit review before your next renewal.