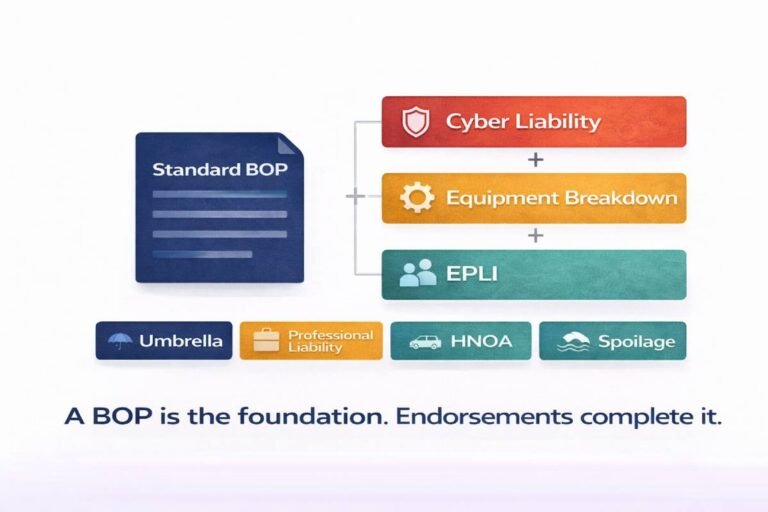

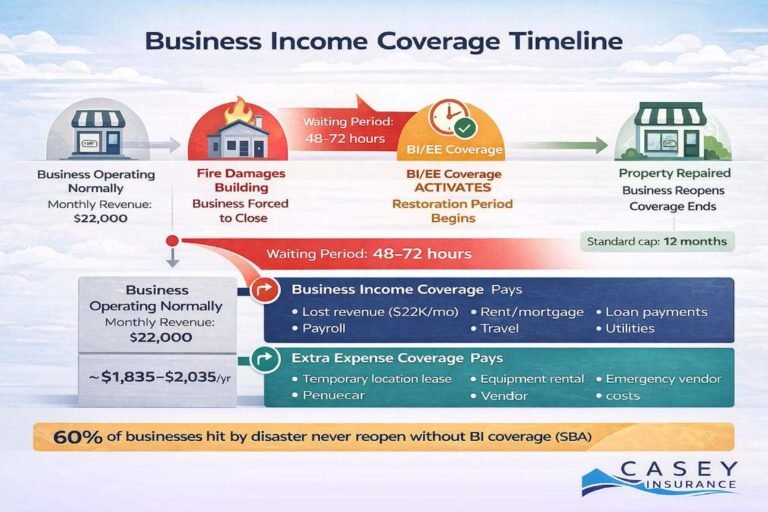

A Business Owners Policy gives you the foundation: general liability, commercial property, and business income coverage in one policy. But a standard BOP has real gaps and for many businesses, those gaps carry significant financial risk.

BOP endorsements also called riders or add-ons are targeted coverage extensions that plug those gaps. The right endorsements don’t add unnecessary cost; they address the specific exposures your standard policy was never designed to cover. The wrong ones are premium you don’t need.

Here’s a direct look at the endorsements worth adding what each covers, who actually needs it, and why it matters.

Standard BOP Gaps:

Cyber attacks / data breaches, mechanical equipment failure, employee lawsuits, professional errors, flood damage, employee theft, off-premises property, and employee vehicle use are all excluded from standard BOP coverage. Each requires a separate endorsement or policy.

BOP Endorsements: Quick Reference What’s Worth Adding and Why

| Endorsement | What It Covers | Who Needs It | Why It Matters |

|---|---|---|---|

| Cyber Liability | Covers data breach costs, ransomware, cyber BI, regulatory fines | All — especially any business storing customer data or using digital systems | Most important gap in a standard BOP for 2026 |

| Equipment Breakdown | Covers sudden mechanical/electrical failure of HVAC, refrigeration, boilers, production equipment | Restaurants, manufacturers, salons, medical offices, any business reliant on critical equipment | Standard BOP property excludes mechanical failure entirely |

| EPLI | Covers wrongful termination, discrimination, harassment, and wage claims by employees | Any business with employees — risk grows with headcount | Not covered anywhere in a standard BOP |

| Commercial Umbrella | Extends GL liability limits by $1M+ above primary BOP limits | Contractors, delivery, client-facing businesses — anyone with significant public liability | Cost-effective way to access higher limits without repricing the base policy |

| Professional Liability (E&O) | Covers financial harm to clients from errors or omissions in your professional services | Consultants, accountants, IT firms, designers, advisors, and any advice-driven business | GL does not cover professional errors — this fills the gap |

| Hired & Non-Owned Auto (HNOA) | Covers business liability when employees use personal vehicles or you rent vehicles for work | Any business where employees occasionally drive for work tasks | See our HNOA guide for full details |

| Flood (separate policy) | Covers building, equipment, and inventory damaged by flood and storm surge | All Florida businesses with a physical location — critical for hurricane exposure | Standard BOP property explicitly excludes flood — a standalone NFIP or private policy is required |

| Equipment Spoilage | Covers perishable inventory lost due to power outages or refrigeration failure | Restaurants, caterers, grocers, florists, pharmacies, food distributors | Losses from overnight fridge failure are not property damage — standard BOP won’t pay |

| Employee Dishonesty / Crime | Covers theft, forgery, or fraud committed by employees | Retail, cash-handling businesses, any business with employees who have access to funds or inventory | Standard theft coverage only applies to external theft — internal employee theft is excluded |

| Inland Marine | Covers business property in transit or at off-premises locations (job sites, client sites, vehicles) | Contractors, IT service firms, field service businesses, anyone who regularly moves equipment | BOP property only covers assets at your listed address |

The Three Endorsements Most Small Businesses Should Prioritize

Every business’s risk profile is different but three endorsements consistently fill the most costly gaps in a standard BOP for the broadest range of small businesses in 2026:

- Cyber liability: The single most important BOP gap in 2026. Standard property and GL do not respond to data breaches, ransomware, or cyber extortion. If your business stores customer information, processes payments online, or relies on digital systems that’s virtually every business today cyber liability is not optional. The average cyber claim for a small business is $79,000 (SmartFinancial 2026), and the cost of adding cyber to a BOP is typically $20–$80/month.

- Equipment breakdown: Standard BOP property covers damage from fire, theft, and vandalism not from mechanical failure. When your HVAC system fails, your commercial refrigerator dies, or your production equipment breaks down unexpectedly, standard property pays nothing. Equipment breakdown coverage is particularly critical for restaurants, medical offices, and any operation where a single equipment failure can halt revenue.

- EPLI (Employment Practices Liability): Once you have employees, you have exposure to claims of wrongful termination, discrimination, harassment, and wage disputes. None of these are covered by your BOP’s GL. EPLI protects against one of the fastest-growing categories of small business litigation and its absence is felt most acutely by businesses hiring for the first time.

Florida Priority:

For Florida businesses, add flood insurance (separate policy) to every BOP for any location with a physical premises. Hurricane storm surge and flooding are excluded from standard BOP property and this is Florida’s most commonly triggered property loss event. Review before June 1 each year.

Match Your Add-Ons to Your Business Type

Beyond the top three, the right endorsements depend on what your business does:

- You provide professional advice or services: Add Professional Liability (E&O) — GL does not cover financial harm caused by your professional work

- You sell or serve food: Add Equipment Spoilage — covers perishable inventory lost to power or refrigeration failure

- Employees drive for work tasks: Add Hired & Non-Owned Auto (HNOA) — personal auto policies exclude business use

- You handle cash or have access-level employees: Add Employee Dishonesty / Crime — internal theft is excluded from standard BOP theft coverage

- Your team works at client sites or transports equipment: Add Inland Marine — BOP property only covers assets at your listed address

- Your GL limit feels thin for your contract requirements: Add a Commercial Umbrella — extends total GL limits affordably without repricing the base policy

What Do BOP Endorsements Cost?

Endorsements are almost always the most cost-efficient way to access expanded coverage adding protection to an existing policy rather than building a separate one from scratch.

Typical ballpark ranges:

- Cyber liability: $20–$80/month added to BOP premium

- Equipment breakdown: $15–$50/month depending on equipment type and value

- EPLI: $30–$100/month depending on employee count and industry

- Professional liability (E&O): $25–$75/month for low-risk professional services

- Commercial umbrella ($1M): $20–$60/month — one of the highest return-on-premium coverages available

- HNOA: $10–$35/month added to existing GL or commercial auto

An independent advisor can access multiple carriers for each endorsement ensuring you get the most competitive pricing for your specific risk profile rather than a single-carrier default rate.

Frequently Asked Questions

For the majority of small businesses in 2026, the three most important BOP endorsements are cyber liability (covers data breaches, ransomware, and cyber events excluded from standard BOP), equipment breakdown (covers sudden mechanical failure of HVAC, refrigeration, and equipment not covered by standard property), and EPLI (covers employee claims of wrongful termination, discrimination, or harassment not covered by GL).

No — standard BOP property and liability components do not respond to data breaches, ransomware, or cyber extortion. You need a cyber liability endorsement or standalone cyber policy to cover breach response costs, regulatory fines, business interruption from a cyber event, and third-party liability from compromised customer data.

Build the BOP Your Business Actually Needs

The right endorsements turn a solid foundation into a complete protection program. The wrong ones add cost without coverage value. Our advisors help you identify the specific gaps in your current BOP, match the right endorsements to your business model, and price them competitively across multiple carriers. Explore our optional BOP endorsements insurance or contact us for a BOP coverage review today.